Table of Contents

ToggleEnsuring you receive your full State Pension is one of the most important steps you can take for financial security in retirement. While the extended April 2025 deadline to fill National Insurance (NI) gaps going back to 2006 has now closed, there is still plenty you can do to boost your pension. Here’s everything you need to know.

What Changed After 5 April 2025?

Until 5 April 2025, eligible individuals could fill gaps in their National Insurance record, going back to 2006, potentially covering up to 16 missing years. That special extended window is now permanently closed.

Under the current standard rules, you can now only fill gaps from the last six tax years. As of the 2025/26 tax year, this means you can go back to the 2019/20 tax year. Each year that passes, the oldest eligible year drops off, so acting sooner rather than later remains important.

Important note for those affected by the HMRC website outage:

HMRC’s online service went offline unexpectedly on the final day of the deadline (5 April 2025), preventing around 21,000 people from completing their payments. HMRC has confirmed that those affected by this error will be contacted and given extra time to complete their top-up. If you tried to pay on the deadline day and were unable to, contact HMRC directly to confirm your situation.

Why Topping Up Your National Insurance Still Matters

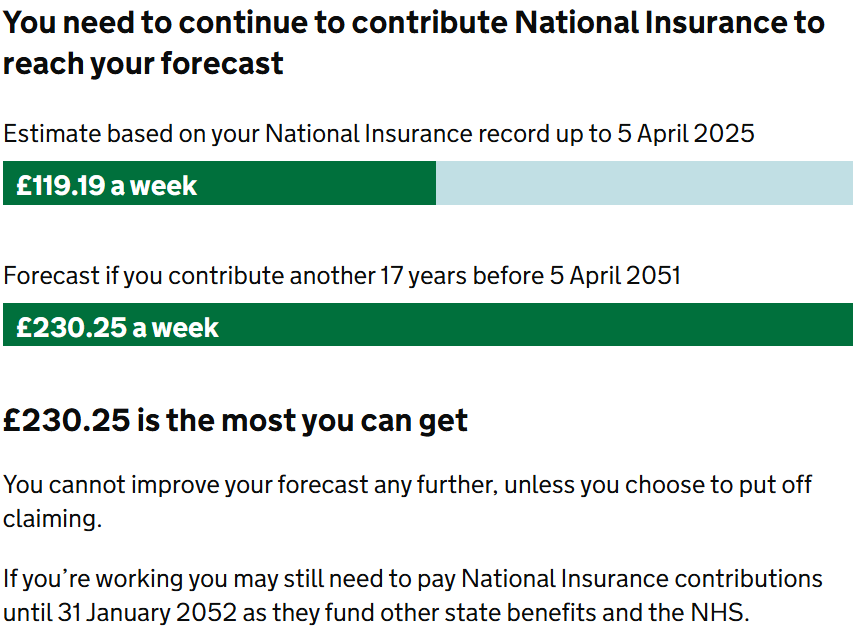

Even with the extended window now closed, topping up your NI record within the standard six-year window can still make a significant difference to your retirement income. Each full qualifying year you add is worth approximately 1/35th of the full State Pension.

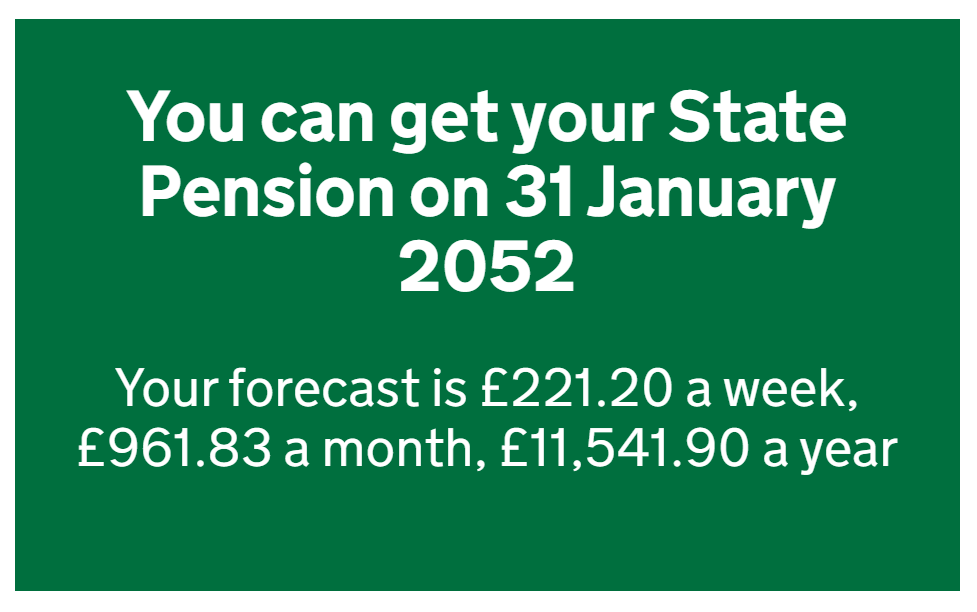

For the 2025/26 tax year, the full new State Pension is £230.25 per week (£11,973 per year). Adding one qualifying year could increase your annual pension by around £342, and that increase is paid for life, inflation-linked, and requires no investment risk.

With a typical top-up cost of around £923 for the 2025/26 tax year (or less for earlier years), most people recoup the cost within just two to three years of receiving their pension.

How to Check and Top Up Your National Insurance Record

Step 1: Check your National Insurance record. Visit the GOV.UK National Insurance records page and log in to your Personal Tax Account to see a full breakdown of your qualifying years and any gaps going back to 2019/20.

Step 2: Check your State Pension forecast. Use the government’s State Pension forecast tool to see how much you’re currently on track to receive, and how filling gaps could affect your entitlement.

Step 3: Determine if paying is worthwhile for you. Not everyone benefits from making voluntary contributions. Before paying, check whether you might be entitled to free NI credits instead (for example, if you were on Carer’s Allowance, Child Benefit, or Universal Credit). Also consider whether you already have 35 qualifying years; if so, further top-ups won’t increase your pension.

Step 4: Get a reference number and make a payment. Once you’ve confirmed it’s beneficial, contact HMRC for a payment reference number. You can then pay online, by bank transfer, or at a bank. Full instructions are available on Gov.UK

What Does It Cost to Top Up?

The cost to fill a gap depends on the tax year. Earlier years are generally cheaper to fill than the current year. For example, filling a gap for 2019/20 costs around £780, while filling the 2025/26 costs approximately £923. Each year must be assessed individually, and you do not have to fill all gaps, only the ones that will actually increase your State Pension entitlement.

Class 2 contributions (for those who were self-employed) are considerably cheaper and may apply if you have relevant gaps during self-employment. Always confirm the applicable class before paying.

Q: Who can still benefit from topping up?

Anyone with gaps in their NI record from 2019/20 onwards who is not on track for a full State Pension can potentially benefit. This includes those who had career breaks, worked abroad, were self-employed with low profits, or earned below the NI threshold in certain years.

Q: Can I still fill gaps if I’m already receiving my State Pension?

Yes, in some cases. If you are already receiving your State Pension and it is below the full amount, you may still be able to top up. Contact the Pension Service on 0800 731 0469 for guidance specific to your situation.

Q: I missed the April 2025 deadline, what are my options?

You can still fill gaps from the last six tax years (2019/20 onwards). While you can no longer access the extended window going back to 2006, filling recent gaps may still meaningfully increase your State Pension. If you were affected by the HMRC website outage on 5 April 2025, contact HMRC directly, as you may still be eligible to pay for pre-2019 years.

Q: Where can I get personal advice?

Contact the Future Pension Centre on 0800 731 0175 (if you have not yet reached State Pension age) or the Pension Service on 0800 731 0469 (if you are already receiving your State Pension). Both services are free and can confirm whether topping up will actually increase your entitlement before you pay anything.

Q: Act Now, the Six-Year Window Keeps Shrinking

Even though the 2006–2016 window has closed, the six-year rolling window means you still have a limited opportunity to fill gaps. Each year that passes, the oldest eligible gap year drops off permanently. If you have gaps in 2019/20, you must act before 5 April 2026 or that year will become inaccessible forever. Share this article with friends and family who may have gaps in their NI record, the sooner they act, the more options they’ll have. Secure your future, boost your pension today!

Additional Resources

Personalised Retirement Planning Guidance: Click here for personalised retirement planning advice.

- Free E-book Download: “5 Steps to Achieve Financial Independence”, actionable steps to save, reduce debt, and build lasting wealth.

- Check your NI record: gov.uk/check-national-insurance-record

- Make voluntary Class 3 NI contributions: gov.uk/pay-voluntary-class-3-national-insurance

Have questions about Lifetime ISA contribution limits or want to share your LISA savings strategy? Drop a comment below or contact us directly for personalised guidance tailored to your specific circumstances and goals.

Subscribe below to receive regular updates on LISA rules, savings strategies, and the latest government announcements affecting your finances.

Get the Budget Planner