Disclaimer: This content is for educational purposes only and does not constitute tax, financial, or legal advice. Tax rules can change, and individual circumstances vary. Always check official HMRC guidance and consider professional support (e.g., a qualified accountant or Chartered Tax Adviser) for your situation.

Table of Contents

Toggle

Capital Gains Tax (CGT) can feel like an unpleasant surprise, especially if you’ve just sold (or you’re about to sell) shares, crypto, an investment property, or another asset, and you’re now searching for ways to reduce capital gains tax in the UK.

If you’re looking to reduce capital gains tax UK rules allow several HMRC-recognised ways people often use to reduce CGT, and there are also ways to avoid CGT on future investments by using tax-efficient wrappers like ISAs and pensions.

In this guide, I’m going to walk you through 10 practical strategies people commonly explore for 2025/26, split into:

- Part 1: strategies that may help reduce CGT on gains you’re making now

- Part 2: strategies that can help you avoid CGT on future investing

And if you haven’t calculated your potential CGT yet, start here first:

👉 Use my free Capital Gains Tax calculator (UK 2025/26)

(Tip: keep this page open: I’ll refer back to it throughout the blog.)

Quick refresher: what actually triggers Capital Gains Tax?

Capital Gains Tax is charged on the profit (gain) you make when you dispose of an asset, typically by selling it, gifting it (to someone other than a spouse/civil partner), swapping it, or transferring it.

You’re taxed on the gain, not the sale price:

Gain = Sale proceeds-Purchase cost-Allowable costs

For 2025/26, key points to know:

- Annual CGT allowance (Annual Exempt Amount): £3,000 per individual

- Typical CGT rates for individuals (most situations): 18% / 24%

- UK residential property reporting rule: if CGT is due, you usually must report and pay within 60 days of completion

(CGT gets complex quickly once reliefs, losses, mixed-use assets, separation/divorce, trusts, or residency issues are involved; that’s why this article stays educational and encourages professional support when needed.)

Part 1: Ways people reduce CGT on current or upcoming disposals

If you’re selling an asset in 2025/26 (or you already sold one and you’re planning your reporting), these strategies are the ones people often explore first.

1) Use your £3,000 CGT allowance deliberately (and don’t waste it)

For 2025/26, the annual CGT allowance is £3,000 per person.

That means you can make up to £3,000 of gains in the tax year before CGT applies (for most individuals). It’s simple, but it’s also one of the most commonly missed planning opportunities.

Key points:

- It’s per person

- It’s use it or lose it (you can’t carry it forward)

- Couples may be able to use two allowances if assets are held in the right names (more on that below)

Where this works best:

This is especially useful when you can control the timing and size of disposals, for example, with shares, funds, or crypto, where you can sell portions rather than everything at once.

✅ Action prompt:

Before you sell, use the calculator to estimate your gain and see whether it falls within the £3,000 allowance.

2) Consider spouse or civil partner transfers (where appropriate)

UK tax rules generally allow transfers between spouses or civil partners on a “no gain/no loss” basis, meaning the transfer itself usually doesn’t trigger CGT.

Some couples explore this to:

- potentially use two separate £3,000 allowances (£6,000 total), and/or

- Align ownership so that more of the gain falls under a lower CGT rate band (where applicable)

Important notes (keep it safe and factual):

- This typically needs to happen before disposal

- There are rules and exceptions (e.g., separation, residency, beneficial ownership)

- For large gains or complex situations, this is an area where professional advice can be very valuable

Example

If one partner is likely to pay CGT at a higher rate and the other has more “headroom,” the combined household outcome may differ depending on the ownership structure, and you should carefully review this.

✅ Action prompt:

If you’re a couple and selling taxable assets, it can be worth asking:

“Who legally owns the asset, and are both allowances being used efficiently?”

3) Time disposals where you can (shares/funds/crypto), but understand the limits for property

This is an important distinction, as timing strategies work very differently depending on the type of asset involved.

Shares/funds/crypto: you can often sell in portions

With divisible assets, some people sell portions across different tax years to use multiple annual allowances, or to manage how much of the gain falls into higher CGT rates.

Example

Imagine Tom has investments with a total gain of £60,000.

- Option A: sell in one go this tax year

Taxable gain = £60,000 – £3,000 allowance = £57,000 taxable

CGT depends on his band position and rates. - Option B: sell portions across 3 tax years (where feasible)

Year 1 gain: £20,000 – £3,000 = £17,000 taxable

Year 2 gain: £20,000 – £3,000 = £17,000 taxable

Year 3 gain: £20,000 – £3,000 = £17,000 taxable

In total, he’s used three allowances instead of one, which can reduce his overall taxable gains.

✅ Action prompt:

If you’re selling shares/funds/crypto, you can use the calculator to test different sale amounts and see how the estimate changes.

4) Use capital losses to offset gains (and don’t forget to report them)

If you sell an asset for less than you paid for it, the difference is known as a capital loss. In some cases, capital losses can be used to reduce the amount of Capital Gains Tax you pay.

Capital Losses can be used to:

- Offset capital gains made in the same tax year, reducing your overall taxable gain, and/or

- Be carried forward to future tax years to offset gains later (as long as HMRC’s rules are followed)

This means a loss today may still be valuable for future tax planning.

For example:

- Gain on an asset: £50,000

- Loss on another asset: £8,000

- Net gain: £42,000

- Then apply the £3,000 allowance to the net figure (where applicable)

You usually need to claim capital losses with HMRC in order to use them, either in the same tax year or by carrying them forward to future years. HMRC explains how this works, including time limits and reporting requirements, in its guidance on capital losses.

✅ Action prompt:

If you’ve had a “bad investment year” in one place and a big gain in another, it’s worth understanding how losses can be used, and making sure you keep records.

5) Claim all allowable costs (this is where many people overpay)

Allowable costs reduce your gain, and a lower gain often means less CGT.

Common allowable costs can include things like:

- purchase and sale transaction fees (e.g., legal fees, broker fees, estate agent fees)

- certain valuation costs

- improvement costs (for property) that add value or extend the life of the asset (not routine repairs/maintenance)

What’s often not allowable (general examples):

- routine maintenance and repairs

- mortgage interest

- running costs and bills

Because allowable costs depend on the asset and the facts, it’s a good area to check HMRC guidance and keep documentation.

✅ Action prompt:

If you’ve already used the calculator, re-run it with your best estimate of allowable costs included.

6) Understand the 60-day property reporting rule (and use the time wisely)

If you sell UK residential property and CGT is due, you often must report and pay within 60 days of completion.

This rule is strict, and missing it can lead to penalties and interest.

Where this becomes “strategy” (in a practical sense) is not about avoiding the rule, it’s about using the 60-day window to get the calculation right:

- gather your documents early

- identify improvement costs and transaction fees

- confirm the correct acquisition values (especially with inherited property)

- seek professional support if anything is unclear

✅ Action prompt:

If your sale is property-related, don’t leave the calculation until the last minute.

Part 2: Ways people avoid CGT on future investing

If your main takeaway from your CGT calculation was: “I don’t want to deal with this again”, you’re not alone.

The most reliable long-term way to reduce capital gains tax UK investors face is using tax wrappers like ISAs and pensions

These next strategies aim to legally reduce the frequency with which CGT becomes an issue in the first place.

7) Use ISAs (CGT-free growth)

For most UK savers/investors, ISAs are one of the simplest and most accessible “CGT prevention” tools.

In an ISA:

- Investment growth is generally free from CGT

- Dividends and interest are typically tax-free too (subject to ISA rules)

✅ Action prompt:

If you’re investing outside tax wrappers, it may be worth reviewing how much is held in ISAs versus taxable accounts.

(I’ll be writing a dedicated blog on ISA vs General Investment Accounts soon, because this deserves its own deep dive.)

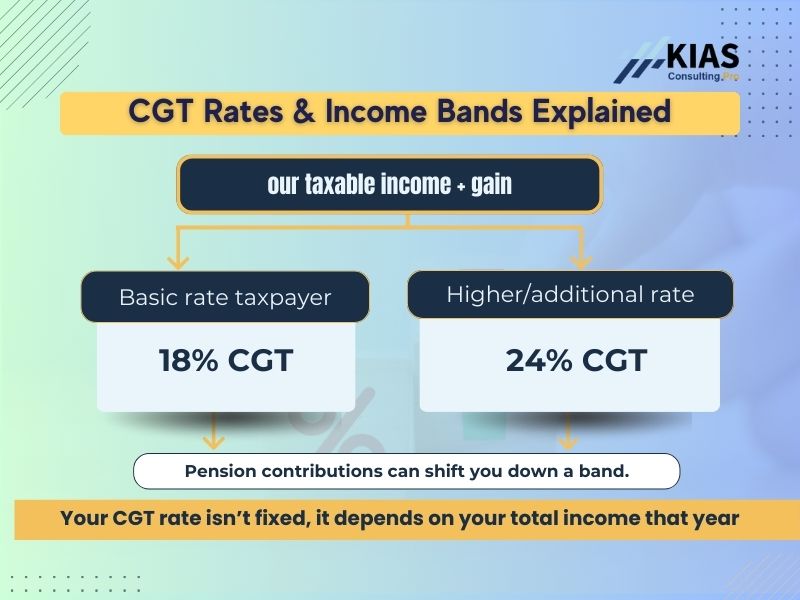

8) Pension contributions can affect your CGT rate (because they affect your income tax band)

Your CGT rate depends on your income tax band.

Pension contributions can reduce taxable income, which may affect how much of a capital gain falls into the 18% or 24% CGT rates (often resulting in a blended outcome).

For example:

Emma plans to sell shares in 2025/26:

- Salary: £55,000

- Taxable gain after allowance: £47,000 (example figure)

If Emma remains a higher-rate taxpayer, more of her gain may fall into the higher CGT rate.

If Emma makes a pension contribution from her income (within pension rules and limits), her taxable income may be reduced. This can increase the amount of her gain taxed at the lower CGT rate.

Important:

- Pension contributions do not cancel CGT

- The contribution doesn’t need to come from the gain

- The effect is about income bands, not the gain itself

- Timing and personal circumstances matter.

9) Specialist tax-advantaged investments (EIS/VCT), high risk and not for everyone

Some investment structures have tax features that can interact with CGT (e.g., deferral or exemption in certain cases). Examples people mention include:

- Enterprise Investment Scheme (EIS)

- Venture Capital Trusts (VCT)

However:

- These can be high-risk

- suitability varies widely

- This is an area where regulated advice and/or specialist tax advice is important

✅ Action prompt:

Treat these as “specialist territory.” If you ever go down this route, you may want to consider seeking professional support.

10) Property reliefs (e.g., Private Residence Relief), understand the rules early

Many people assume “property always triggers CGT”, but that’s not always true.

For example, your main home may qualify for Private Residence Relief (PRR), which can reduce or remove CGT, but the rules can be detailed, especially if:

- The property was let out

- You’ve lived abroad

- You own multiple properties

- It’s mixed-use

- There were periods when it wasn’t your main residence

✅ Action prompt:

If property is involved, don’t rely on assumptions; PRR rules can make a major difference, but they’re fact-specific.

10) Property reliefs (e.g., Private Residence Relief), understand the rules early

Disclaimer reminder: This article is educational and not tax advice.

It’s sensible to seek qualified help when:

- The gain is large (e.g., £50,000+ or £100,000+)

- You have multiple disposals, multiple properties, or mixed assets

- You’re dealing with inherited assets and valuations

- You’re a non-UK resident (or recently moved)

- trusts, divorce, or business assets are involved

A tax adviser/accountant can provide tax-specific advice and compliance support.

Where financial coaching can help

As a personal finance coach, my role is to help you:

- Understand the concepts in plain English

- Organise your figures before meeting a professional

- Identify what questions to ask your accountant/tax adviser

- Review your broader goals, so decisions align with your long-term plan

If you’d like support organising your numbers, clarifying your options, and preparing questions for your accountant/tax adviser, you can

Capital Gains Tax (CGT) Planning Checklist (2025/26)

- Before you sell

- Check whether the disposal is taxable (some reliefs may apply).

- Gather purchase and sale documents (contracts, completion statements, valuations).

- List potential allowable costs and keep proof (e.g., legal fees, agent fees, qualifying improvement costs).

- Estimate your gain using the CGT calculator to avoid surprises.

- Consider whether capital losses are available to offset gains (and ensure losses are recorded/reported correctly).

- If relevant, confirm legal ownership of the asset (especially for couples).

- If property is involved

- Check whether the 60-day CGT reporting and payment rule applies.

- Don’t leave reporting or calculations until the last minute.

- Looking ahead

- Review how much of your investing is held outside ISAs and pensions.

- Consider building tax-efficient investing habits before gains build up.

Q: What is the CGT allowance for 2025/26?

For 2025/26, the Annual Exempt Amount is £3,000 per individual (and typically £1,500 for most trustees). Always verify with HMRC in case rules change.

Q: What are the Capital Gains Tax rates in the UK for 2025/26?

In many common situations, individuals face CGT rates of 18% (lower) and 24% (higher), depending on theirincome tax band and circumstances. Some gains can be taxed at different rates in specific cases.

Q:Can I avoid Capital Gains Tax legally in the UK?

Some people legally reduce or avoid CGT by using tax-efficient wrappers (such as ISAs), making use of allowances, offsetting losses, and ensuring reliefs are applied correctly. What applies depends on personal circumstances.

Q: What is the 60-day CGT property reporting rule?

If you sell UK residential property and CGT is due, you often must report and pay within 60 days of completion. Missing the deadline can trigger penalties and interest.

Q: Can I carry forward unused CGT allowance?

Generally, no, the annual allowance is typically “use it or lose it.” Capital losses can often be carried forward (subject to HMRC rules).

Key Takeaways

- CGT planning is legal, and often comes down to knowing the rules early

- The biggest “quick wins” are usually: allowance, losses, allowable costs, and correct ownership

- The biggest long-term prevention tools are often: ISAs and pensions

- Property has extra complexity (including the 60-day reporting rule)

The key to reduce capital gains tax UK liabilities is planning early, ideally before you sell.”

If you haven’t run your numbers yet, use the calculator first, then come back to this list and see which strategies are worth exploring further.

Get the Budget Planner