📈 Investing Notice: This content is for informational purposes only and not investment advice. Investments can go up and down in value. Always do your own research and seek advice from a regulated professional. See full disclaimer. Table of Contents

Hargreaves Lansdown fee changes are taking effect from 1 March 2026, and while they’ve described it as a “fee reduction”, the reality is more nuanced.

For some investors, these changes will reduce costs. For others, particularly those holding shares, ETFs, or multiple accounts, the new structure could result in higher annual fees.

Because platform charges play a significant role in long-term investment performance, it’s important to understand exactly what’s changing, how it affects different types of investors, and whether the new pricing still represents good value compared to other UK investment platforms.

In this guide, I’ll break down:

- what's changing with the Hargreaves Lansdown fee changes

- Who benefits most, and who may pay more

- How the new fee structure compares with other UK platforms

- What practical steps you can take before the changes take effect

If you already invest through Hargreaves Lansdown, or are considering opening an ISA, SIPP, or Junior ISA, this guide will help you make an informed decision based on your investing style, not marketing headlines.

If you’re a parent investing through a Hargreaves Lansdown Junior ISA, these changes will mostly benefit you, but there are still some details to understand.

What's Changing: Hargreaves Lansdown Fee Changes From March 1st 2026

Here’s a quick overview of the main Hargreaves Lansdown fee changes:

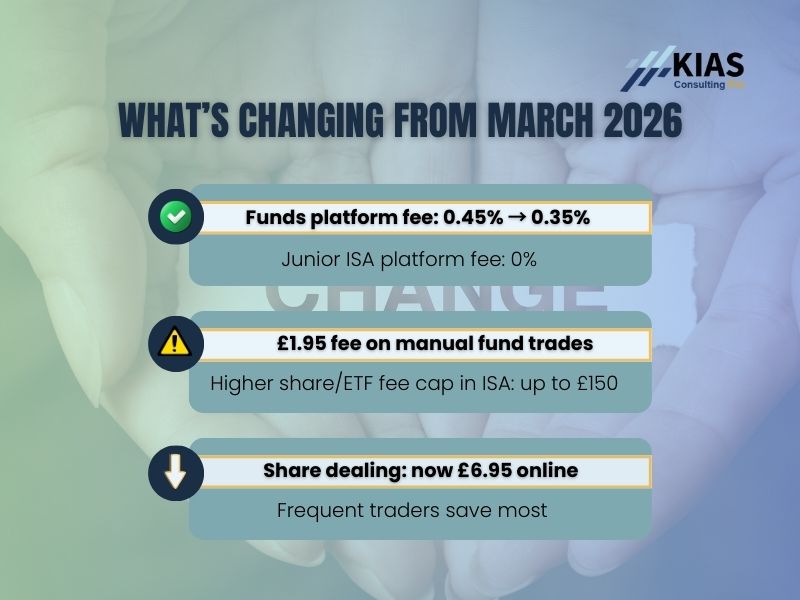

Platform Fee Changes

Account Type | Current Fee | New Fee | Change |

Stocks & Shares ISA (funds) | 0.45% | 0.35% | ✅ Reduced |

SIPP (funds) | 0.45% | 0.35% | ✅ Reduced |

Fund & Share Account (funds) | 0.45% | 0.35% | ✅ Reduced |

Fund & Share Account (shares) | £0 | 0.35% | ❌ New charge |

Junior ISA (funds) | 0.45% | 0% | ✅ Free! |

Fee Caps for Shares/ETFs/Investment Trusts

Account Type | Current Cap | New Cap | Change |

Stocks & Shares ISA | £45/year | £150/year | ❌ Increased |

SIPP | £200/year | £150/year | ✅ Reduced |

Fund & Share Account | £0 | £150/year | ❌ New charge |

Junior ISA | No charge | No charge | ✅ Still free |

Dealing Charges

Trade Type | Current Charge | New Charge | Change |

Online share dealing (0-9 trades) | £11.95 | £6.95 | ✅ Reduced |

Online share dealing (10-19 trades) | £8.95 | £6.95 | ✅ Reduced |

Online share dealing (20+ trades) | £5.95 | £3.95 | ✅ Reduced |

Online fund trading | Free | £1.95 | ❌ New charge |

Junior ISA share trading | £5.95 | £3.95 | ✅ Reduced |

The Good News: Lower HL Platform Fees

Let’s start with the positives. The Hargreaves Lansdown fee changes bring genuine savings for fund investors in ISAs and SIPPs:

Example 1: Fund-Only Investor (ISA)

Portfolio: £50,000 in Vanguard LifeStrategy fund only

Current annual cost:

- Platform fee: £225 (0.45% of £50,000)

- Fund dealing: £0

- Total: £225/year

New annual cost (with quarterly rebalancing):

- Platform fee: £175 (0.35% of £50,000)

- Fund dealing: £0 (using regular monthly investing, which stays free)

- Total: £175/year

Annual saving: £50

Important:

If you manually rebalance by buying and selling funds outside your regular investing, you’d pay £1.95 per trade. But by using HL’s regular monthly investing feature, you completely avoid this charge.

Share Dealing Costs Drop Significantly

The reduction in share dealing charges is substantial:

Trades/Month | Old Cost | New Cost | Saving |

5 trades | £59.75 | £34.75 | £25.00/month |

10 trades | £89.50 | £69.50 | £20.00/month |

20 trades | £119.00 | £79.00 | £40.00/month |

For active traders buying individual shares, this is excellent news.

The Not-So-Good: New Hargreaves Lansdown Charges to Watch

While some fees are falling, HL is either increasing or introducing new fees for the first time:

1. New Fund Trading Fee: £1.95 per Trade.

Previously, buying and selling funds on HL was completely free. From March 1st, each fund transaction will cost £1.95.

When this applies:

- Manual fund purchases (ad-hoc trades)

- Selling funds

- Manually rebalancing between funds

When this DOESN’T apply:

- Regular monthly investing via direct debit (this stays free)

- So if you set up £200/month to go into 3 different funds automatically, you pay £0

Impact example: If you manually rebalance quarterly across 3 funds (sell some of each, buy more of others), that’s 6 trades × £1.95 = £11.70 per quarter = £46.80/year

Smart tip from a reader: Make any large fund purchases before March 1st to avoid this new charge!

2. Fund & Share Account: New 0.35% Charge on Shares.

This is important to understand, so let me clarify what a “Fund & Share Account” actually is…

What’s a Fund & Share Account Anyway?

This caused some confusion, so let’s clarify the different account types at HL:

Tax-Advantaged Accounts (Tax-Free Growth)

These are the accounts most people use:

- Stocks & Shares ISA – Tax-free investing, £20,000/year limit

- SIPP (Self-Invested Personal Pension) – Tax relief on contributions, grows tax-free

- Junior ISA – Tax-free for children under 18, £9,000/year limit

- Lifetime ISA – For first home or retirement, government 25% bonus

For all these accounts:

- Funds: Pay 0.35% platform fee (down from 0.45%)

Shares/ETFs: Pay 0.35% platform fee, capped at £150/year

Fund & Share Account (Taxable)

This is HL’s General Investment Account (GIA) – a taxable account with no annual limits.

Most people DON’T have a Fund & Share Account because the ISA and SIPP give you better tax treatment. You’d only use an FSA if you’d maxed out your ISA allowance (£20,000/year) and wanted to invest more.

New charges for FSA from March 1st:

- Funds: 0.35% platform fee (same as ISA/SIPP)

- Shares/ETFs: 0.35% platform fee, capped at £150/year (WAS FREE)

Bottom line: If all your investing is in ISAs, SIPPs, or Junior ISAs (like most people), you’re not affected by the FSA charge increases.

Understanding the New HL Fund Trading Fee

Let me clear up some confusion around the £1.95 fund trading fee, because this trips up a lot of people:

FREE under the new system:

- Automatic monthly investments set up via direct debit

- Example: You set up £25/month into Vanguard LifeStrategy = £0 cost

- Example: You set up £100/month split across 3 funds = £0 cost

- These are called “regular monthly investments” and remain completely free

COSTS £1.95 under the new system:

- Any manual (ad-hoc) fund purchase you make

- Any fund sale

- Manually rebalancing (selling Fund A to buy more of Fund B)

- One-time lump sum investments outside your regular plan

Real-world scenario from your portfolio:

Looking at your screenshots:

- Lifetime ISA: Holds multiple funds

- SIPP: Holds Legal & General International Index Trust

- Junior ISA: Holds Vanguard LifeStrategy 100% Equity

If these are all on regular monthly investing: £0 new charges

If you manually rebalance quarterly (e.g., sell some of one fund to buy another): £7.80/year in new charges (4 rebalances × 2 trades × £1.95)

Smart strategy:

Set up regular monthly investing where possible, and only rebalance manually once or twice a year to minimise the £1.95 charges.

Breaking Down the Hargreaves Lansdown Fee Changes: Will You Pay More or Less?

Let’s look at some realistic scenarios to see how the Hargreaves Lansdown fee changes will affect different investors:

Scenario 1: Fund Investor with Regular Investing (Winner)

Example Portfolio

- £1,867.70 in Lifetime ISA (funds)

- £651.51 in SIPP (investment trust)

- £1,505.72 in Junior ISA (fund)

- Uses regular monthly investing

Current costs:

- Platform fees: £18.11/year total

- Fund dealing: £0

- Total: £18.11/year

New costs:

- Platform fees: £14.09/year (0.35% on LISA + SIPP, 0% on Junior ISA)

- Fund dealing: £0 (using regular monthly investing)

- Total: £14.09/year

Result: Saves £4.02/year

Small saving now, but as your portfolio grows, the 0.10% difference (0.45% → 0.35%) will save you more!

Example Portfolio

- £1,867.70 in Lifetime ISA (funds)

- £651.51 in SIPP (investment trust)

- £1,505.72 in Junior ISA (fund)

- Uses regular monthly investing

Current costs:

- Platform fees: £18.11/year total

- Fund dealing: £0

- Total: £18.11/year

New costs:

- Platform fees: £14.09/year (0.35% on LISA + SIPP, 0% on Junior ISA)

- Fund dealing: £0 (using regular monthly investing)

- Total: £14.09/year

Result: Saves £4.02/year

Small saving now, but as your portfolio grows, the 0.10% difference (0.45% → 0.35%) will save you more!

Scenario 2: Larger Portfolio, Fund-Only, Using Regular Investing (Big Winner)

Portfolio:

- £100,000 in Stocks & Shares ISA (all funds)

- Uses regular monthly investing for additions

Current costs:

- Platform fee: £450 (0.45%)

- Fund dealing: £0

- Total: £450/year

New costs:

- Platform fee: £350 (0.35%)

- Fund dealing: £0 (regular monthly investing stays free)

- Total: £350/year

Result: Saves £100/year

Scenario 3: Active Trader with Shares Across Multiple Accounts (Mixed Results ⚖️)

Portfolio:

- £50,000 Stocks & Shares ISA (individual shares)

- £80,000 SIPP (individual shares and ETFs)

- Makes 3-4 trades per month

Current costs:

- ISA: £45 (capped)

- SIPP: £200 (capped)

- Share dealing: £47.80/month average (4 trades × £11.95)

- Total: £818.60/year

New costs:

- ISA: £150 (new cap)

- SIPP: £150 (new lower cap)

- Share dealing: £27.80/month (4 trades × £6.95)

- Total: £633.60/year

Result: Saves £185/year ✅

Even with higher fee caps, the reduced dealing charges win out for active traders!

Scenario 4: Multi-Account Holder with Fund & Share Account (Potential Loser)

This applies to sophisticated investors who’ve maxed out ISAs/SIPPs and use taxable accounts:

Portfolio:

- Stocks & Shares ISA: £50,000 (shares)

- SIPP: £80,000 (shares)

- Fund & Share Account: £50,000 (shares)

Current costs:

- ISA: £45 (capped)

- SIPP: £200 (capped)

- FSA: £0

- Total: £245/year

New costs:

- ISA: £150 (new cap)

- SIPP: £150 (new lower cap)

- FSA: £150 (new cap)

- Total: £450/year

Result: Extra £205/year (84% increase)

This is the scenario in which costs increase significantly. However, most retail investors don’t have Fund & Share Accounts, they stick with ISAs and SIPPs.

What This Means for Different Investors

Fund-Only Investors: Clear Winners

If you primarily invest in funds:

- Your platform fee drops from 0.45% to 0.35%

- Use regular monthly investing (free) to avoid the £1.95 trading fee

- Make large purchases before March 1st if possible

- Overall: You’ll save money

Action:

Set up or continue regular monthly investing to keep costs at zero.

Share/ETF Investors in ISAs/SIPPs: Winners

If you invest in individual shares or ETFs:

- Much cheaper dealing costs (£11.95 → £6.95)

- Platform fees stay at 0.35%, but caps increased for ISAs (£45 → £150)

- For most share investors under £43,000, you’ll pay more in platform fees

- But the dealing savings likely outweigh this if you trade regularly

- Overall, Active traders benefit; buy-and-hold investors need to calculate

Action:

Calculate your annual dealing costs vs platform fee changes.

Junior ISA Holders: Big Winners

Excellent news for parents investing for children:

- Platform fees drop to 0% (was 0.45% on funds!)

- Share trading costs fall to £3.95 per trade (was £5.95)

- No account charge for holding anything

- Overall: Significant cost reduction for long-term children’s investing

For more on Junior ISAs, see my guide: How to Choose the Best Junior ISA

Fund & Share Account (GIA) Holders: Losers

If you have a taxable Fund & Share Account:

- New 0.35% charge on shares (was free)

- Capped at £150/year

- This mainly affects high earners who’ve maxed out ISAs/SIPPs

- Overall: Definite cost increase

Action: Consider whether you still need the FSA or if there are more tax-efficient alternatives.

How Hargreaves Lansdown Fees Compare to Competitors After Changes

Understanding investment fees is crucial for long-term wealth building. Let’s see how the Hargreaves Lansdown fee changes position HL against major UK platforms:

Note:

All information verified from platform websites as of January 2026.

Platform Fee Comparison (£50,000 Portfolio, Funds Only)

Platform | Platform Fee | Annual Cost |

InvestEngine (DIY) | 0% | £0 |

Trading 212 | 0% | £0 |

HL (New) | 0.35% | £175 |

Vanguard | 0.15% (min £48/year) | £75 |

AJ Bell Dodl | 0.15% (min £12/year) | £75 |

Platform Fee Comparison (£50,000 Portfolio, Shares/ETFs Only)

Platform | Platform Fee | Annual Cost |

InvestEngine (DIY) | 0% | £0 |

Trading 212 | 0% | £0 |

HL (New) | 0.35% (capped £150) | £150 |

Vanguard | Not available | N/A |

AJ Bell Dodl | 0.15% (min £12/year) | £75 |

Dealing Costs (Per Trade)

Platform | Share Trading | Fund Trading |

InvestEngine (DIY) | Not available | £0 (ETFs only) |

Trading 212 | £0 | £0 (no mutual funds) |

HL (New) | £6.95 | £1.95 |

Vanguard | Not available | £0 |

AJ Bell Dodl | £0 | £0 |

Important clarifications:

- AJ Bell Dodl is different from AJ Bell (the full platform)

- Dodl charges 0% trading fees on both shares and funds

- Dodl has a simpler, app-only interface with limited investment choices

- AJ Bell (full platform) charges £5.00 per share trade and £1.50 per fund trade

FX Fees (Buying US Stocks)

Platform | FX Fee |

Trading 212 | 0.15% (best) |

InvestEngine | 0.45% (on non-GBP ETFs) |

AJ Bell Dodl | 0.75% (£0-£10k), 0.50% (£10-20k), 0.25% (£20k+) |

HL | Around 1% (tiered) |

Vanguard | 0% (Vanguard funds only) |

For investors heavily into US stocks, FX fees can dwarf platform fees. Trading 212’s 0.15% is an exceptional value.

The Verdict

HL remains competitive for:

- Fund-only investors who value HL’s research, service, and tools

- Active share traders benefiting from the new £6.95 trading cost

- Investors with very large portfolios where absolute percentage matters less

- Parents using Junior ISAs (now 0% platform fees!)

But it’s now clearly more expensive than:

- InvestEngine: Best for passive ETF investors (0% platform fee, ETF-only)

- Trading 212: Best for active share traders (0% trading, 0.15% FX)

- Vanguard: Best for Vanguard fund enthusiasts (low cost, limited selection)

- AJ Bell Dodl: Best for simple, low-cost fund/share investing via app

For detailed comparisons:

Should You Switch From Hargreaves Lansdown After Fee Changes?

Switching investment platforms isn’t a decision to take lightly, but the Hargreaves Lansdown fee changes might make it worthwhile for some investors. Here’s how to decide:

Consider Switching If:

1. You hold shares across multiple HL accounts and will hit multiple £150 caps

- Zero-fee platforms could save you £300-450+ annually

- That’s £3,000-4,500 over 10 years, plus lost growth

2. You actively trade shares and want the absolute lowest costs

- Trading 212 charges £0 per trade vs HL’s £6.95

- On 10 trades/month, that’s £834/year saved

3. You invest primarily in ETFs and want passive “set and forget” investing

- InvestEngine charges no platform fees on DIY ETF portfolios

- You’ll still pay the ETF’s OCF, but save the 0.35% HL platform fee

4. You invest heavily in US stocks

- Trading 212’s 0.15% FX fee vs HL’s ~1% FX fee

- On £10,000 of US stock purchases: £15 vs ~£100 in FX costs

Stick with HL If:

1. You value HL’s research, tools, and customer service

- HL’s research is genuinely comprehensive and beginner-friendly

- Customer service is consistently highly rated

- The platform is user-friendly with excellent educational resources

2. You invest mainly in funds using regular monthly investing

- The 0.35% platform fee is now competitive

- Regular monthly investing stays free (no £1.95 charge)

- Your costs have genuinely decreased

3. Your portfolio is under £50,000

- Fee differences are relatively small in £ terms at this level

- The hassle of transferring might not be worth it

- HL’s service and peace of mind may justify the cost

4. You have a Junior ISA at HL

- Now charges 0% platform fees, which are incredibly competitive.

- HL Junior ISAs are now one of the best value options

- No strong reason to switch

5. You use HL-specific products

- HL Ready-Made Portfolios (fees also reduced)

- Active funds not available elsewhere

- If these are core to your strategy, stay put

What About the Junior ISA?

The Junior ISA changes are particularly positive:

- HL now charges 0% platform fees on Junior ISAs

- Share trading costs have fallen to £3.95

- This makes HL one of the most competitive Junior ISA providers

Bottom line for Junior ISAs: Unless you’re paying very high fund OCFs, HL is now excellent value. No strong reason to switch unless you prefer a specific alternative for other features.

Action Steps: What To Do Before the Hargreaves Lansdown Fee Changes

Here's your practical action plan to navigate the Hargreaves Lansdown fee changes:

✓ Step 1: Calculate Your Personal Impact

⏱️ Time needed: 20 minutes

⚡ Step 2: Smart Moves Before March 1st

Do this before March 1st if it makes sense

🤔 Step 3: Decide Whether to Stay or Switch

Ask yourself:

- Will I save or pay more under the new structure?

- How much is the difference annually?

- Over 10 years, what's the total impact (including compound growth)?

- Do I value HL's service enough to justify any extra cost?

Rule of thumb:

- Saving money? Great, enjoy the reduction

- Paying £50-100 more/year? Probably worth staying for the service

- Paying £200+ more/year? Consider alternatives seriously

- That £200 difference = £2,000+ over 10 years, plus lost investment growth

🔍 Step 4: If Switching, Research Alternatives

⏱️ Time needed: 1-2 hours

For fund investors:

- Review Vanguard (excellent for Vanguard fans, limited to Vanguard funds only)

- Review InvestEngine (zero platform fees on DIY ETF portfolios)

- Read my guide: Investment Fees Explained UK

For share traders:

- Review Trading 212 (zero trading fees, 0.15% FX - lowest in UK)

- Review AJ Bell Dodl (zero trading, but limited selection)

- Check my: Trading 212 Guide

For international/US investors:

- FX fees matter hugely - can exceed platform fees

- Trading 212 has UK's lowest FX fees (0.15%)

- See: Investment Fees Explained

📅 Step 5: Review Annually

Whether you stay or switch

- Set a calendar reminder for January 2027

- Review how fee changes affected your actual costs

- Check if your platform still offers best value as portfolio grows

- Platforms change their fees - stay informed!

💡 Pro Tip: Make fund purchases before March 1st to avoid the new £1.95 trading fee!

Only do this if it aligns with your existing investment plan; never invest early purely to avoid a small fee.

Q: Will my Junior ISA be affected?

Great news, the Junior ISA is largely unaffected by these changes. HL’s Junior ISA already charges 0% on both platform fees and online dealing. That stays the same. The only new addition is a foreign exchange (FX) charge if you buy overseas shares in the Junior ISA, but if you stick to UK-listed funds or shares, nothing changes for you at all. This is why the Junior ISA remains one of the best-value options on HL. No platform fee, no dealing fee online, just the fund’s own charges

Q: Does regular monthly investing still avoid dealing charges?

Yes! Regular monthly investing in funds remains completely free. This is a key way to minimize costs under the new structure. However, the £1.95 charge applies to: Any manual (ad-hoc) fund purchases Selling funds Rebalancing between funds manually Smart tip: Use regular monthly investing wherever possible, and only make manual trades when necessary..

Q: What's the difference between a Fund & Share Account and my ISA?

Stocks & Shares ISA = Tax-free investment account, £20,000/year contribution limit Fund & Share Account = HL's General Investment Account (GIA), fully taxable, no limits Most people only use ISAs and SIPPs because they're tax-efficient. You'd only use an FSA if you'd maxed out your £20,000 ISA allowance and wanted to invest more. The big change is that FSA holders will now pay 0.35% (capped £150) on shares—this was previously free.

Q: Are there any hidden charges I should know about?

The main “hidden” costs that catch people out: FX fees when buying US/international stocks (~1% at HL) Fund OCFs (ongoing charges within the fund itself, typically 0.08%-1%+) Bid-ask spread on ETFs (small cost built into the price) Stamp duty on UK shares (0.5%, charged by the government) None of these are specific to HL; all platforms have them. But it’s worth being aware.

The Hargreaves Lansdown fee changes are genuinely mixed—not the simple “fee reduction” their marketing suggests, but not universally bad either.

The clear winners:

- Fund-only investors using regular monthly investing in ISAs/SIPPs

- Active share traders benefiting from lower dealing costs (£11.95 → £6.95)

- Junior ISA holders (0% platform fees!)

- Investors who value HL’s service and can afford slightly higher costs

Those who need to calculate carefully:

- Share investors in ISAs hitting the new £150 cap (up from £45)

- Anyone who manually rebalances funds frequently

- Fund & Share Account holders seeing new charges on shares

Those who might want to switch:

- Multi-account holders with significant share holdings (facing £450 annual caps)

- Very cost-conscious investors who could use zero-fee alternatives

- Heavy US stock investors paying high FX fees

My recommendation:

Take 20 minutes to calculate your personal impact using the steps above.

If you’ll save money or pay only marginally more, staying with HL makes sense. They offer excellent service, comprehensive research, and a user-friendly platform that’s particularly good for beginners.

But if you’re looking at £200+ extra annually, explore alternatives like *InvestEngine (ETF-only, zero fees), Trading 212 (zero trading, low FX), or Vanguard (low cost for Vanguard funds if your portfolio is above £32,000.00).

🔗 Affiliate Disclosure: This post contains affiliate links. This means we may earn a small commission at no extra cost to you. Read our full Affiliate Disclosure for more information.

Remember: Investment fees compound over time. A £200 annual difference isn’t just £2,000 over 10 years, it’s that £2,000 plus the growth you’d have earned on it. For younger investors building wealth, every 0.10% matters.

Whatever you decide, make it an informed choice based on YOUR situation and YOUR values, not just HL’s headlines or competitor marketing.

One final practical tip: If you were planning any fund purchases anyway, consider making them before March 1st to avoid the new £1.95 charge. It’s a small saving, but when investing long-term, small savings add up!

Only do this if it aligns with your existing investment plan; never invest early purely to avoid a small fee

Related Guides You’ll Find Helpful

Understand Your Fees:

Platform Comparisons:

- InvestEngine UK Review 2025: Is It Worth It?

- Trading 212 UK Review 2025

- Best Stocks & Shares ISA Platforms

Investing for Children:

Getting Started:

About This Guide:

This article provides educational information about Hargreaves Lansdown’s fee changes. All fee information has been verified from official platform websites as of January 30, 2026. I don’t receive commissions for recommending (or not recommending) any platform; I provide practical guidance based on verified facts.

Stay Updated:

Fee structures change regularly. While this guide is accurate as of January 2026, always check the latest information on provider websites. Review my Investment Fees Explained guide for current comparisons across UK platforms.

Get the Budget Planner

This is one of the clearest breakdowns of the HL fee changes I’ve seen. I like how you showed that it’s not a simple ‘fee cut’, it really depends on investing style and account mix.

Thanks so much. I am glad you found value in reading this. Have you done your calculations to determine what steps you need to take? Thanks for reading.