Table of Contents

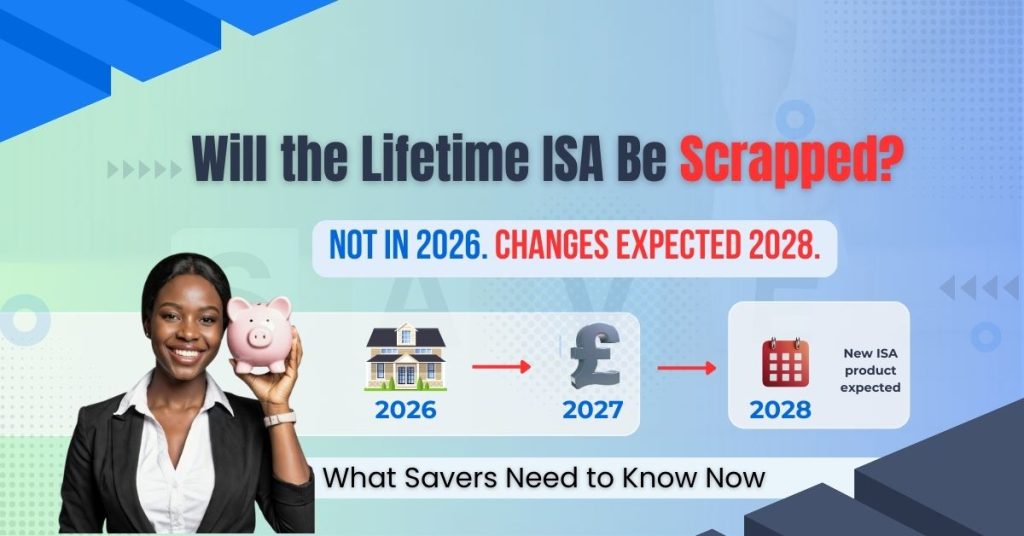

ToggleIs the Lifetime ISA being scrapped? That’s the question hundreds of savers have been asking since the Autumn Budget 2025. The short answer is no, but significant changes are coming. Here’s everything you need to know about what’s changing, what’s staying the same, and what it means for your savings strategy.

This is an important planning topic, but to be clear, the current Lifetime ISA product remains unchanged for now, and any replacement or reform is not expected to take effect until at least April 2028.

Key Takeaways

➤ Current LISAs continue indefinitely – No cut-off date for existing accounts

➤ You can still open a new LISA – Eligibility rules unchanged (ages 18-39)

➤ New product coming around April 2028 – First-time buyers only (retirement feature removed)

➤ The retirement savings feature may be removed from the new product for new savers

➤ Withdrawal penalty being removed in the new product (currently 25%)

➤ Bonus structure changing – From monthly payments to a lump sum at purchase

➤ Many details unknown – Property cap, bonus percentage, contribution limits to be confirmed

Bottom line:If you’re eligible for a LISA, there’s no reason to delay opening one. In fact, opening one now under the current rules may give you better long-term returns, even if it’s just to put £1 into the account to secure it before you turn 40.

Is the Lifetime ISA Being Scrapped? What's Really Happening

Why the Lifetime ISA Isn't Being Scrapped: The Government's New Consultation

In the Autumn Budget 2025, the government announced a consultation on a new, simpler ISA product designed to support first-time home buyers. The aim is to streamline LISA and address its complexities and criticisms, particularly the controversial 25% withdrawal penalty.

According to official Gov.uk publications:

HMRC published Tax-Free Savings Newsletter 19 (November 2025) and Newsletter 20 (January 2026), which confirm that:

- The government will consult on a new product to support first-time buyers

- The current Lifetime ISA will remain available until any new product is launched

- You can continue to open a Lifetime ISA and keep contributing under the current rules until the replacement product is introduced.

- Account holders can continue to contribute to their existing LISAs without any restrictions.

Important: This is still in the consultation phase. The government is gathering feedback from industry and the public before finalising the new product’s design.

When Will Lifetime ISA Changes Take Effect?

Following industry feedback and internal analysis, the government has decided to postpone mandatory digital reporting under the digitalisation of ISAs until April 2028.

However, the government has not confirmed an official launch date, and this timeline could change depending on:

- The consultation process and feedback received

- Legislative approval timelines

- Technical implementation requirements

- Political and economic conditions

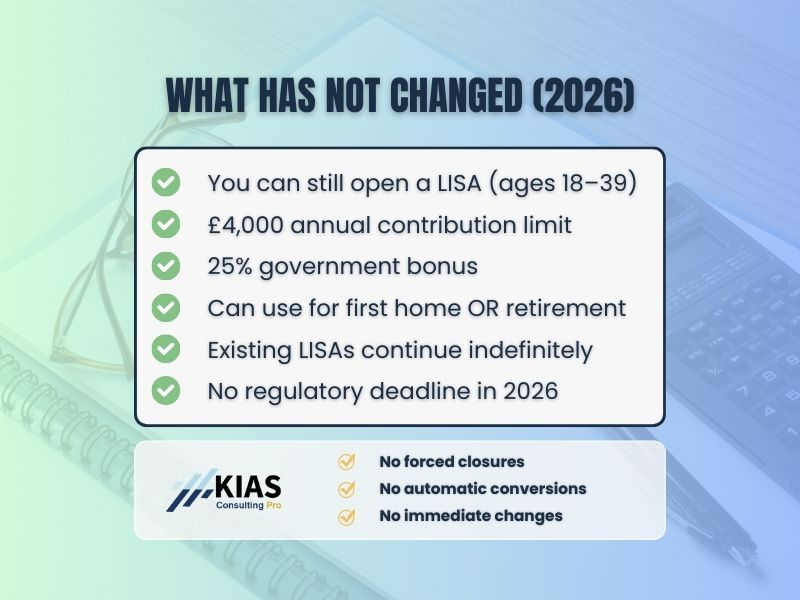

What This Means for 2026-2027

- Current Lifetime ISAs do not stop or close

- There is no immediate deadline to open or fund a LISA this year

- People can still open and contribute to a Lifetime ISA under existing rules

- No urgency from a regulatory cut-off perspective

So, although reform is on the horizon, there is no panic deadline in 2026 or 2027.

Lifetime ISA Changes: What's Different in the Proposed 2028 Product

Emerging policy discussions and government announcements suggest several potential changes to the new ISA design. Remember, these are proposals under consultation and not yet final.

Lifetime ISA Retirement Feature Being Removed (But Not Scrapped)

The replacement ISA may only support first-time home purchase saving, removing the existing LISA’s dual purpose of home buying and retirement saving.

What this means:

- New savers after the launch date (likely 2028) may not be able to use the new product for retirement

- Existing LISA holders can continue using their accounts for retirement under current rules

- People saving for retirement may need to rely on pensions or standard ISAs instead

Instead of receiving the 25% government bonus periodically throughout the year, which allows your bonus to earn interest or investment returns alongside your contributions, the new product may only pay the bonus as a lump sum when you complete your house purchase.

What this means:

You would miss out on years of compounding growth on your bonus. This could potentially reduce your overall savings pot by hundreds of pounds, depending on how long you save before buying.

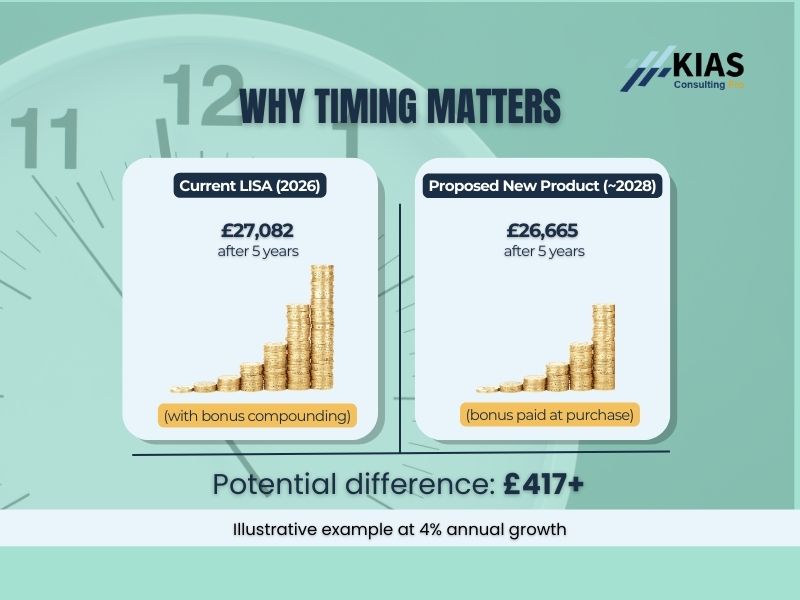

Example comparison:

Let’s say you save £4,000 per year for 5 years, with an average annual interest rate of 4%:

Current LISA (monthly bonus with compound interest):

- Year 1: Save £4,000 + receive £1,000 bonus = £5,000 (this earns interest for 5 years)

- Year 2: Save £4,000 + receive £1,000 bonus = £5,000 (this earns interest for 4 years)

- Year 3-5: Same pattern

- Total after 5 years with compound interest: approximately £27,082

Proposed new product (lump sum bonus at purchase only):

- Years 1-5: Save £4,000/year = £20,000 total contributed

- Your £20,000 grows with 4% interest to approximately £21,665

- The government adds a £5,000 bonus at the point of house purchase

- Total: approximately £26,665

Difference: You could have around £417 less with the new structure due to losing compound growth on the annual bonuses over five years.

The longer you save before buying, the bigger this difference becomes.

Withdrawal Charges May Be Removed

The current 25% withdrawal penalty for non-qualifying withdrawals could be eliminated in the new product, removing one of the most common criticisms of the current LISA.

Why the penalty can be removed:

Under the proposed new product, the government will only pay the 25% bonus when you complete your house purchase. This means all the money in your account before that point is entirely yours, you haven’t received any government money yet. Therefore,there’ss no need topenalisee you for withdrawing your own money if your circumstances change.

Under the current system, you receive the 25% bonus immediately each year, which is why the government needs to reclaim it (plus an additional amount to offset the lost bonus) if you withdraw for non-qualifying purposes.

What this means:

- Greater flexibility if your circumstances change (e.g., you decide not to buy, or you exceed the property cap)

- No risk of getting back less than you contributed if you need to access funds early

- Makes the product less risky for people with uncertain timelines

Current LISA penalty example:

- You save £4,000 and receive a £1,000 bonus = £5,000 total in your account

- If you withdraw early for non-qualifying reasons: £5,000 minus 25% penalty (£1,250) = £3,750 returned to you

- You get back less than you originally put in

Proposed new product:

- No penalty meansyou’dd get back what you contributed, just without receiving the bonus

This is arguably the biggest improvement in the new product design, particularly for savers who value flexibility.

Retirement Saving Could Be Dropped

HMRC guidance indicates that the new product may not support the retirement-saving use case, meaning the Lifetime ISA’s role as a retirement option could change or be removed entirely for new savers.

What this means:

- Ifyou’re currently using a LISA for retirement (accessible from age 60), you can continue under existing rules indefinitely

- New savers after the new product launches (around 2028) may not have this option

- They would also need to use alternative retirement savings vehicles, such as pensions or regular Stocks & Shares ISAs.

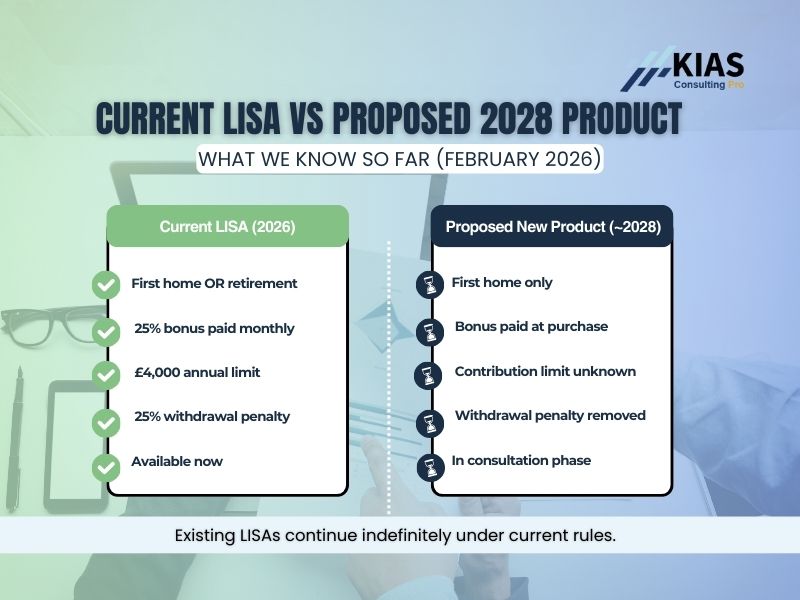

Current LISA vs Proposed New Product

Here’s a side-by-side comparison of what we know:

Feature | Current LISA (2026) | Proposed New Product (~2028) |

Purpose | First home OR retirement | First home ONLY |

Bonus payment timing | Monthly/periodic (compounds over time) | Lump sum at purchase |

Withdrawal penalty | 25% on non-qualifying withdrawals | Removed |

Annual contribution limit | £4,000 | Unknown (likely £4,000) |

Government bonus | 25% (up to £1,000/year) | Unknown (likely 25%) |

Property price cap | £450,000 | Unknown (may be updated) |

Age eligibility to open | 18-39 | Unknown |

Can use for retirement? | Yes (age 60+) | Likely NO for new accounts |

Status | Available now | Consultation phase |

Availability | Indefinite for existing accounts | Expected around April 2028 |

Why Your Lifetime ISA Isn't Being Scrapped: What Continues in 2026

- Individuals aged 18-39 can still open a Lifetime ISA under the current rules.

- Save up to £4,000 per tax year and receive a 25% government bonus (up to £1,000 annually)

- You can use the account towards a first home purchase (up to £450,000) or access it from age 60 for retirement.

- The existing Lifetime ISA remains available indefinitely until the government launches the new product.

- No changes to contribution limits until at least April 2031

- All current withdrawal rules, including the 25% penalty, remain in place.

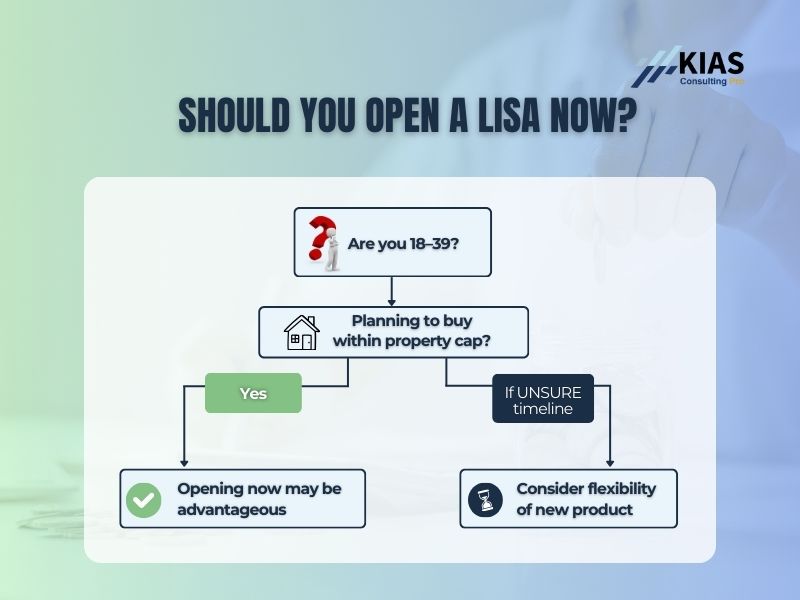

Is the Lifetime ISA Being Scrapped for You? What Different Savers Should Know

If You’re a First-Time Buyer

Good news:

- The new product should work better for you with no withdrawal penalty

- More forgiving if your circumstances change (e.g., relationship breakdown, job loss, property price changes)

- Likely still includes a 25% government bonus (to be confirmed)

🎯 Action Steps

1. Consider opening a LISA now under current rules to start earning the 25% bonus with monthly compounding and benefit from tax-free growth, rather than waiting until 2028 for the lump sum structure, which offers less overall return.

2. Start saving early to maximise both the bonus and compound interest benefits.

3. Monitor updates to the £450,000 property cap, as many experts expect the government to increase it to reflect current house prices.

4. Watch for:

- Confirmation of the property price cap (currently £450,000)

- Final bonus percentage for the new product

- Annual contribution limits

If You’re Saving for Retirement (Age 60+)

Keep your existing LISA:

- You can continue contributing indefinitely under current rules

- The retirement feature will remain available for your existing account

- No forced closure or conversion to the new product

New savers after 2028:

- May need to look at alternative retirement products such as personal pensions or regular Stocks & Shares ISAs

- The new product likely won’t support retirement savings as a qualifying withdrawal option

Uncertainty:

We don’t yet know whether retirement-focused LISAs will remain available to new savers, or whether the option will be discontinued entirely for anyone opening an account after the new product launches.

Consider: If you’re planning to save for retirement and are eligible to open a LISA now (ages 18-39), it may be worth opening one before the new product launches to preserve the retirement option. By opening now, you’ll benefit from:

- Immediate 25% government bonus on contributions (up to £1,000 per year)

- Tax-free investment/savings growth - all interest and investment returns grow completely tax-free

- Tax-free withdrawals from age 60 - unlike pensions, which are subject to income tax on withdrawal

- Dual flexibility - you can still use it for a first home if your plans change before age 60

This gives you a powerful retirement savings vehicle that may not be available to new savers after the replacement product launches.

If You’re Unsure About Your Timeline

Current LISA:

- 25% penalty on early withdrawals for non-qualifying purposes

- High risk if you’re not certain about your home-buying timeline or whether you’ll stay within the property price cap

New product (expected 2028):

- No penalty, significantly more flexibility

- Better option if you value adaptability over maximum compounding returns

Consider:

- Your risk tolerance and how certain you are about buying a home within the qualifying criteria

- Whether you’re likely to stay within the £450,000 property cap in your target area

Your timeline, if you’re planning to buy soon (within 1-3 years), the current LISA could give you better overall returns due to monthly bonus compounding.

Q: Should I wait until 2028 to open a LISA?

No. If you’re eligible (ages 18-39), opening a LISA now means you start earning the 25% bonus immediately, benefit from compounding as your bonus earns interest or investment returns over time, and lock in the dual-purpose feature that allows you to use it for either home buying or retirement. Under the proposed new product, the bonus would be paid only at purchase, significantly reducing your overall returns, and the retirement option would not be available.

Q: What happens to my existing LISA after 2028?

You can keep it and continue contributing under the current rules indefinitely. Your existing LISA will not be closed, converted, or affected by the new product launch.

Q: Will the 25% bonus stay the same in the new product?

Unknown. The consultation hasn’t confirmed the bonus percentage for the new product, though it’s likely to remain at 25% given the government’s stated goal of supporting first-time buyers. We’re awaiting further details from the consultation process.

Q: Can I use my existing LISA for retirement after 2028?

Yes, absolutely. If you already have a LISA, you can continue using it for retirement purposes and access it penalty-free from age 60. The retirement feature is being removed from the new product for new savers, not from existing accounts.

Q: Is the £450,000 property price cap being updated?

Yes, absolutely. If you already have a LISA, you can continue using it for retirement purposes and access it penalty-free from age 60. The retirement feature is being removed from the new product for new savers, not from existing accounts.

Q: If I open a LISA now, will I be forced to switch to the new product in 2028?

No. The government has confirmed that existing LISA holders can continue under current rules indefinitely. You will not be required to switch to the new product.

Q: Can I have both a current LISA and the new product when it launches?

This hasn’t been confirmed yet and will depend on the final regulations. Typically, you can have only one active LISA at a time, but we’ll need to wait for official guidance once the consultation concludes and the legislation is drafted

Q: What if I’ve already maxed out my LISA contributions but want to save more?

You can use your remaining ISA allowance (£20,000 total minus your £4,000 LISA contribution = £16,000 remaining) to save into a Cash ISA or Stocks & Shares ISA. All ISA types offer tax-free growth on savings and investments.

Is There Urgency to Open a LISA Now?

No regulatory deadline exists in 2026 to open or fund a Lifetime ISA. The key consideration for savers is planning, understanding the potential reforms and how they might affect long-term saving strategies.

However, there are strategic reasons you might want to act sooner rather than later:

Why Opening a LISA Now Makes Sense

1. Compounding bonus growth – Monthly bonuses earn interest or investment returns for years before you buy, significantly increasing your total pot.

2. Dual-purpose flexibility – Lock in both retirement and home-buying options, giving you maximum future flexibility

3. Certainty of current rules – No guessing what the final new product will look like or whether it will be as generous

4. Time value – The earlier you start, the more you benefit from compound growth on both contributions and bonuses

5. Higher overall returns – As shown in our example, you could have several hundred pounds more by benefiting from bonus compounding

Why You Might Wait

1. Uncertain timeline – If you genuinely don’t know when you’ll buy a home, the current 25% penalty risk is significant

2. Property cap concerns – If you’re highly likely to exceed the £450,000 cap in your target area

3. Strong preference for flexibility – The new product’s penalty removal is more important to you than maximising returns

Bottom line: For most eligible savers who are serious about buying a home within the property cap in the next 5-10 years, opening a LISA now is financially advantageous. But this is a planning decision based on your circumstances, rather than a looming regulatory cutoff.

Lifetime ISAs continue to be a valuable tool for:

- First-time buyers seeking a government bonus on savings plus compound growth over time

- People saving for retirement who appreciate a tax-efficient structure with tax-free withdrawals

- Those who want the flexibility of both home buying and retirement options under one product (for now)

The government’s consultation and proposal for a new, simpler ISA reflects a genuine desire to refine the product and address legitimate criticisms, particularly the harsh withdrawal penalty that has trapped some savers. But the current Lifetime ISA remains open and fully operational and is likely to remain available until around 2028.

You can continue to open and contribute to a Lifetime ISA today while staying informed about how the reforms progress through the consultation process.

What Should You Do Now?

If You’re Eligible for a LISA (Ages 18-39)

- Consider opening one now to lock in the current rules and start earning bonuses that compound over time

- Subscribe to our newsletter to stay updated on the consultation process and any new developments as they’re announced

- Read our complete LISA series for comprehensive guidance on how to maximise your savings:

Part 1: What is a Lifetime ISA? An Introduction for First-Time Buyers

Part 1: What is a Lifetime ISA? An Introduction for First-Time Buyers- Part 2: Lifetime ISA for First-Time Buyers: How to Secure Your First Home in the UK

- Part 3: Cash vs Stocks & Shares LISA: How to Choose the Best Lifetime ISA for Your Goals

- Part 4: Understanding LISA Withdrawal Rules and Penalties

Part 5: LISA Contribution Limits and Government Bonus Explained

Part 5: LISA Contribution Limits and Government Bonus Explained- Part 6: Planning for Retirement with Your Lifetime ISA

Not Sure If a LISA Is Right for You?

Have questions about the LISA changes or need help with your savings strategy? Drop a comment below or contact us directly for personalised guidance tailored to your specific circumstances and goals.

Get the Budget Planner