Understanding Lifetime ISA contribution limits is essential if you want to maximise the full benefits of this powerful UK savings account. A Lifetime ISA allows you to contribute up to £4,000 per tax year, and the government adds a 25% bonus of up to £1,000 annually. Knowing how Lifetime ISA contribution limits work can help you plan your savings more effectively for your first home or retirement.

Table of Contents

Toggle

In this guide, we’ll break down everything you need to know about LISA contribution limits, how the 25% government bonus is calculated and paid, and practical strategies to get the most from your account.

Quick Summary

Annual LISA contribution limit: £4,000 per tax year (confirmed until April 2031)

Maximum government bonus: £1,000 per year (25% of £4,000)

Overall ISA allowance: £20,000 per tax year (LISA contributions count toward this)

Contribution age limits: Can contribute from age 18 until the day before you turn 50

One LISA rule: You can only pay into one Lifetime ISA per tax year

Bonus payment: Usually added within 4-9 weeks of each contribution

Tax year: Runs from 6 April to 5 April the following year

Why Lifetime ISA Contribution Limits Matter

Understanding Lifetime ISA contribution limits helps you maximise your government bonus and avoid costly mistakes. Contributing each tax year strategically ensures you receive the full 25% government bonus and build your savings faster. Whether you’re aiming for your first home or retirement, knowing exactly how much you can contribute, and when, makes all the difference to achieving your financial goals.

The £4,000 Annual Contribution Limit

How Much Can You Save Each Year?

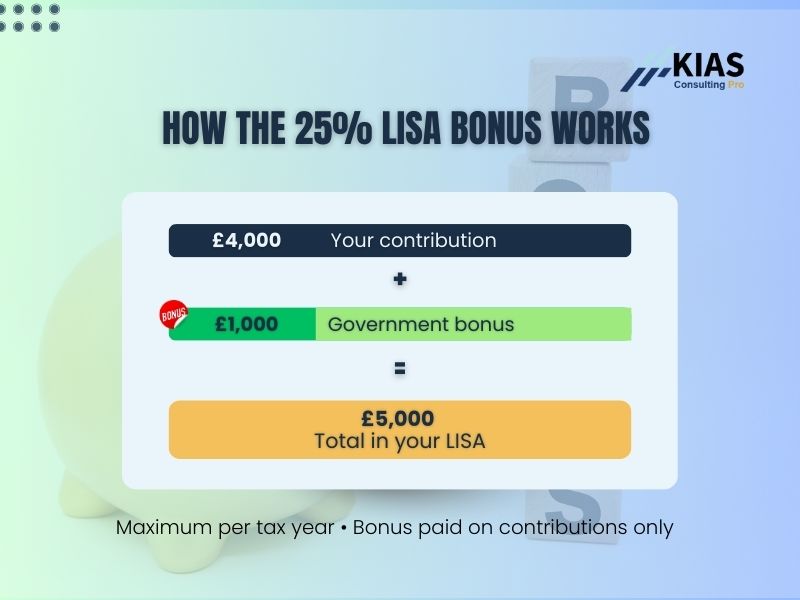

The maximum you can contribute to your Lifetime ISA in any tax year is £4,000. This is your personal contribution allowance, which means if you contribute the maximum, you’ll receive a £1,000 government bonus (25% of £4,000), giving you a total of £5,000 in your account.

Important: This £4,000 Lifetime ISA contribution limit applies regardless of whether you have a Cash LISA, Stocks & Shares LISA, or both. You cannot contribute £4,000 to each type; it’s £4,000 total across all your Lifetime ISAs.

2026 Budget Update: LISA Contribution Limits Frozen Until 2031

The government confirmed the Lifetime ISA contribution limit will remain £4,000 per year until at least April 2031, subject to future policy changes. This provides certainty for long-term planning.

What this means for you:

- You can reliably plan your savings knowing the LISA contribution allowance won’t change for at least 5 years

- The £4,000 limit won’t be adjusted for inflation during this period

- The maximum annual government bonus remains at £1,000 until 2031

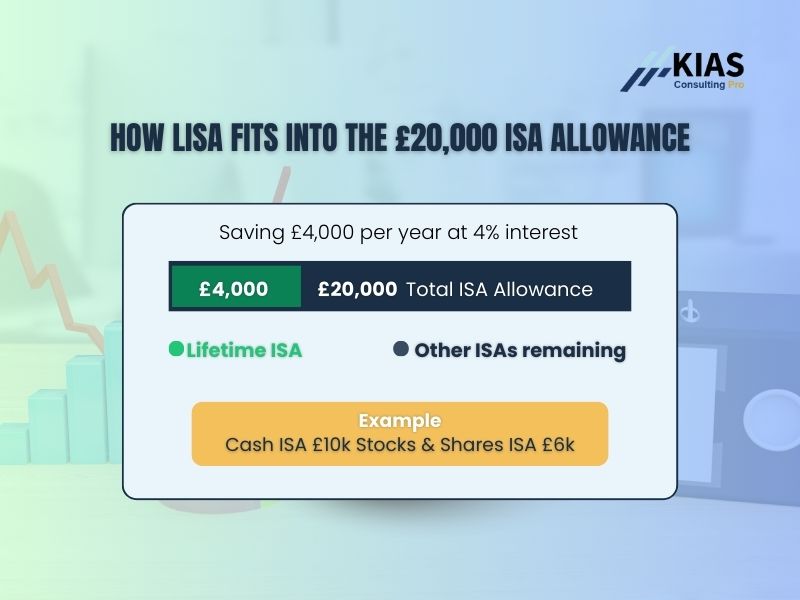

How the £4,000 LISA Limit Fits Within Your Overall ISA Allowance

The £20,000 Total ISA Allowance

Every UK taxpayer has an overall ISA allowance of £20,000 per tax year. This is the total amount of new money you can save or invest across all types of ISAs combined, including:

- Cash ISAs

- Stocks & Shares ISAs

- Lifetime ISAs

- Innovative Finance ISAs

Your Lifetime ISA contribution counts toward this £20,000 total.

Working Out What’s Left

If you contribute the maximum £4,000 to your LISA, you’ll have £16,000 remaining that you can contribute to other ISAs in the same tax year.

Example:

- You contribute £4,000 to your Lifetime ISA

- You have £16,000 left for other ISAs

- You could put £10,000 in a Cash ISA and £6,000 in a Stocks & Shares ISA

- Total across all ISAs: £20,000

For more on making the most of your ISA allowance, see our guide: The Tax-Free Secret: Why an ISA Should Be in Your Financial Plan.

Understanding the 25% Lifetime ISA Bonus

How the LISA Bonus Works

If you contribute the maximum £4,000 to your LISA, you’ll have £16,000 remaining that you can contribute to other ISAs in the same tax year.

Example:

- You contribute £4,000 to your Lifetime ISA

- You have £16,000 left for other ISAs

- You could put £10,000 in a Cash ISA and £6,000 in a Stocks & Shares ISA

- Total across all ISAs: £20,000

Understanding Lifetime ISA contribution limits helps you plan your contributions strategically and maximise your government bonus each tax year.

For more on making the most of your ISA allowance, see our guide: The Tax-Free Secret: Why an ISA Should Be in Your Financial Plan.

What Happens If You Contribute Too Much?

Excess Contributions Explained

If you contribute more than £4,000 to your LISA in a single tax year, the extra amount is called an “excess contribution.”

What happens to excess contributions:

- No bonus on the excess: Excess contributions do not receive a government bonus

- Usually returned without penalty: Your provider will usually return the excess amount without applying the 25% withdrawal penalty, provided it is corrected properly through the provider

- Must be corrected: Contact your provider immediately to arrange the return of excess contributions

How to Avoid Excess Contributions

- Track your contributions carefully throughout the tax year

- Remember the tax year runs from 6 April to 5 April (not calendar year)

- If you're close to the limit, check your balance before making additional contributions

- Most providers will reject contributions that would exceed your allowance, but don't rely on this

How to Avoid Excess Contributions

If you accidentally contribute too much:

1. Contact your provider immediately

to correct the error.

2. They can help you withdraw the excess amount without penalty

3. The sooner you act, the easier it is to resolve

Understanding withdrawal penalties helps you avoid losing your bonus. Read: Understanding LISA Withdrawal Rules and Penalties for complete details on when penalties apply.

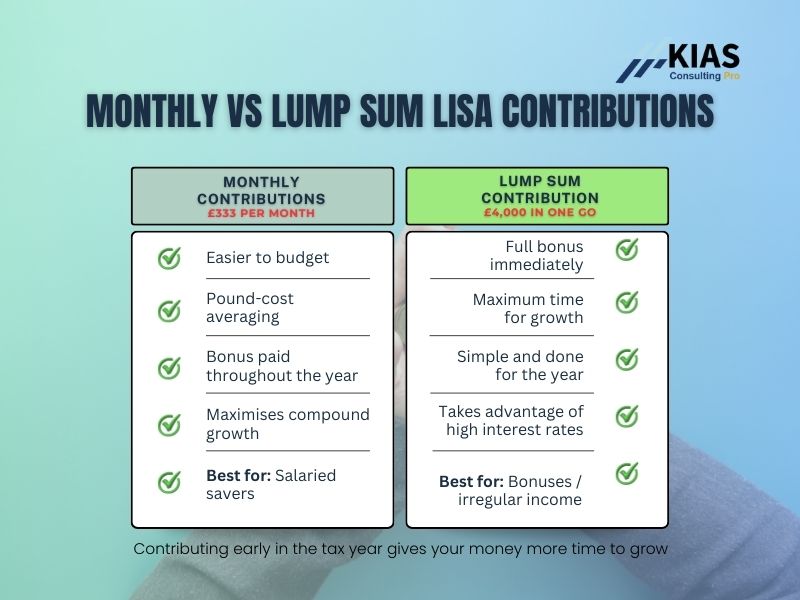

Contribution Strategies: Monthly vs Lump Sum

Should You Contribute Monthly or as a Lump Sum?

There are two main approaches to contributing to your LISA: regular monthly contributions or lump sum deposits. Each has its advantages.

Monthly Contributions

How it works: You set up a standing order or direct debit to contribute a set amount each month (e.g., £333.33 per month to reach £4,000 annually).

Advantages:

- Easier to budget – Smaller, regular amounts are more manageable than a large lump sum

- Pound-cost averaging – For Stocks & Shares LISAs, you invest at different price points, reducing the impact of market volatility

- Bonus paid more frequently – You receive bonus top-ups throughout the year as you contribute

- Maximises compound growth – Earlier contributions (and their bonuses) have more time to earn interest or investment returns

Disadvantages:

- Requires discipline to maintain regular contributions

- May miss out on time in the market if you have the full amount available upfront

Best for: Most savers, especially those on a regular salary or those investing in a Stocks & Shares LISA

Lump Sum Contributions

How it works: You deposit the full £4,000 (or whatever amount you can afford) at once, typically at the start of the tax year.

Advantages:

- Immediate bonus – Your full £1,000 government bonus is claimed in one go

- Maximum compound growth – The full amount (including bonus) has the entire year to earn returns

- Simple and straightforward – One transaction and you’re done for the year

- Takes advantage of high interest rates – If rates are particularly good at a certain point

Disadvantages:

- Requires having £4,000 available at once

- For investments, you’re exposed to market timing risk (all your money goes in at one price point)

Best for: Those with savings available at the start of the tax year or those with irregular income (self-employed, bonuses, etc.)

The Best Time to Contribute

If you’re making a lump sum contribution, early in the tax year (April/May) is typically best because:

- Your money has the maximum time to grow

- The government bonus has more time to earn interest or investment returns

- You lock in your allowance early before circumstances change

However, contributing at any point in the tax year is better than not contributing at all!

Regardless of your approach, Lifetime ISA contribution limits remain fixed at £4,000 per tax year, so consistency and timing are key.

If you’re deciding between account types for your contributions, read: Cash vs Stocks & Shares LISA: How to Choose the Best Lifetime ISA for Your Goals.

Maximising Your LISA Bonus: Practical Tips

1. Contribute Early and Often

The sooner you contribute, the sooner you receive the 25% Lifetime ISA bonus, and the more time that bonus has to grow. Even small, regular contributions add up over time thanks to compound interest.

Example: If you contribute £333 per month starting in April, your final contribution and bonus in March will have less time to grow than your first contribution in April. Starting early maximises this effect.

2. Use the Full £4,000 Allowance Every Year

If you can afford it, always aim to contribute the full £4,000 each year to maximise your £1,000 government bonus. If you don’t use your annual LISA contribution allowance, it doesn’t roll over; you lose it.

Over 10 years at full contributions:

- Your contributions: £40,000

- Government bonuses: £10,000

- Total before growth: £50,000

That’s £10,000 in free money you’d miss if you didn’t maximise contributions!

3. Consider Tax Year Planning

If you have irregular income or receive bonuses, plan:

- Set aside money throughout the year in a separate savings account

- Make your LISA contribution when you have the funds available

- Don’t wait until March, the earlier the better

4. Coordinate with Other ISAs

If you’re also contributing to a Cash ISA or Stocks & Shares ISA, prioritise your LISA first to ensure you get the 25% government bonus. The LISA bonus makes it the most valuable ISA for most savers.

Recommended priority:

- LISA – Get the 25% bonus (up to £4,000)

- Workplace pension – Get employer contributions (free money!)

Other ISAs – Use remaining ISA allowance (up to £16,000 more)

Working with Other ISAs: The One LISA Rule

You Can Only Pay Into One LISA Per Tax Year

Even though you can have multiple Lifetime ISAs open (perhaps a Cash LISA and a Stocks & Shares LISA), you can only contribute to one of them in any given tax year.

Example scenario:

- In the 2025/26 tax year, you contribute £4,000 to a Cash LISA with Provider A

- In the same tax year, you cannot contribute to a Stocks & Shares LISA with Provider B

- You’d need to wait until the next tax year (starting 6 April 2026) to contribute to the other LISA

Switching Between LISA Types

If you want to move from a Cash LISA to a Stocks & Shares LISA (or vice versa), you can transfer your existing LISA to a new provider. This doesn’t count as a new contribution, so it doesn’t use up your annual allowance.

Key points about transfers:

- Transfers must be done directly between providers (don’t withdraw and redeposit yourself)

- Your government bonuses transfer with you

- Your 12-month LISA holding period continues (no reset)

- You can still make new contributions to the new LISA after transferring

Important: Not All Providers Accept LISA Transfers

Before you plan to transfer, check whether your intended new provider accepts LISA transfers. Not all providers do, which can be frustrating if you’ve already decided to switch.

Note:

Some providers do not accept LISA transfers even though they offer other ISA products. For example, Hargreaves Lansdown does not accept Lifetime ISA transfers from other providers, so always check before assuming you can transfer to a specific platform.

For Stocks & Shares LISAs:

- AJ Bell Dodl – Accepts transfers and charges just 0.15% annually (minimum £1 per month), making them one of the most competitive options for Stocks & Shares LISAs

- AJ Bell Youinvest – The full platform version also accepts transfers

- Nutmeg – Accepts LISA transfers for their managed investment service

For Cash LISAs:

- Moneybox – Accepts transfers and currently offers competitive interest rates

- Tembo Money – Accepts transfers for their Cash LISA product

- Plum – Accepts LISA transfers

Always check with your chosen provider before initiating a transfer. Contact them directly to confirm:

- They accept LISA transfers

- What documentation they need

- How long the transfer process takes (typically 4-8 weeks)

- Whether there are any transfer fees

Pro tip:

If you’re moving from a Cash LISA to a Stocks & Shares LISA, AJ Bell Dodl’s 0.15% fee (£1 minimum per month) makes them particularly attractive. On a £20,000 LISA balance, that’s just £30 per year, compared to other platforms charging 0.25%-0.45%.

Age Limits for LISA Contributions

When Can You Start Contributing?

You must be aged 18 to 39 to open a Lifetime ISA. Once you’ve opened your account, you can continue contributing until the day before your 50th birthday.

Important timeline:

- Age 18-39: Can open a new LISA

- Age 18-49: Can contribute to an existing LISA

- Age 50+: No new contributions allowed (but your existing LISA continues to grow)

Example: If you open a LISA at age 39, you can contribute for 11 years (until age 49), potentially adding £44,000 and receiving £11,000 in government bonuses.

Why the Age 50 Cut-Off?

The LISA was designed to encourage long-term savings for first-time home buyers and retirement. The age 50 cut-off ensures that savers have at least 10 years until they can access their LISA penalty-free at age 60 for retirement.

Real-Life Example: Maximising Your LISA Over 5 Years

Let’s look at a practical example of someone maximizing their Lifetime ISA contributions:

Meet Sarah, age 32:

- Wants to buy her first home in 5 years

- Has £4,000 to invest each year

- Chooses a Cash LISA earning 4% interest

Year-by-year breakdown:

Year | Sarah’s Contribution | Gov Bonus | Interest Earned* | Year-End Balance |

1 | £4,000 | £1,000 | £100 | £5,100 |

2 | £4,000 | £1,000 | £304 | £10,404 |

3 | £4,000 | £1,000 | £516 | £15,920 |

4 | £4,000 | £1,000 | £737 | £21,657 |

5 | £4,000 | £1,000 | £966 | £27,623 |

Total over 5 years:

- Sarah’s contributions: £20,000

- Government bonuses: £5,000

- Interest earned: £2,623

- Final balance: £27,623

*Interest calculated at 4% annually on the growing balance

The power of the government bonus is clear: Sarah ends up with £7,623 more than she contributed, a 38% return on her investment before accounting for interest.

How This Fits Into Your Lifetime ISA Strategy

Because Lifetime ISA contribution limits are capped at £4,000 per year, it is important to plan how you use the remaining ISA allowance effectively.

Maximising your Lifetime ISA contributions should be part of a broader financial strategy. Combined with smart investment choices and proper withdrawal planning, LISAs can significantly accelerate your journey toward home ownership or retirement.

Understanding your LISA contribution limits is just one piece of the puzzle. To build a complete strategy:

- Choose the right LISA type for your timeline – See Part 3: Cash vs Stocks & Shares LISA

- Understand when you can access your money – Read Part 2: Lifetime ISA for First-Time Buyers

- Know the withdrawal rules to avoid penalties – Check Part 4: Understanding LISA Withdrawal Rules and Penalties

- Plan for retirement if that’s your goal – Coming in Part 6: Planning for Retirement with Your LISA

By coordinating your LISA contributions with your overall financial plan, you maximise not just your government bonus but your entire financial future.

Q: Can I contribute more than £4,000 if I didn’t use last year’s allowance?

No. The £4,000 annual Lifetime ISA contribution allowance doesn’t carry over from previous years. Each tax year stands alone, and unused allowances are lost.

Q: Do transfers between LISA providers count toward my £4,000 limit?

No. Transfers don’t count as new contributions. You can transfer your entire LISA balance and still contribute up to £4,000 of new money in the same tax year.

Q: What if I contribute and then withdraw in the same tax year?

If you make a withdrawal (with the 25% penalty), this doesn’t free up your contribution allowance. Once you’ve contributed £4,000 in a tax year, that’s your limit regardless of withdrawals.

Q: Can I split my £4,000 contribution across multiple LISAs?

No. You can only contribute to one Lifetime ISA per tax year. You must choose which LISA to contribute to for that year.

Q: Do I get a bonus on money transferred from a Help to Buy ISA?

No. The LISA government bonus is only paid on new contributions. Transfers from a Help to Buy ISA to a LISA move your existing balance (including the Help to Buy bonus you’ve already earned), but don’t generate a new 25% LISA bonus.

What Should You Do Now?

If You Don't Have a LISA Yet

1. Decide if a LISA is right for you - Are you saving for a first home or retirement?

2. Choose Cash or Stocks & Shares - Based on your timeline and risk tolerance

3. Open your LISA before age 40 - Even if you only contribute £1 initially

4. Set up regular contributions - Automate your savings to reach £4,000 annually

Need help deciding? See Part 1: What is a Lifetime ISA? for a comprehensive introduction.

If You Already Have a LISA

1. Check your contribution total for this tax year - Make sure you're not close to the £4,000 limit

2. Plan your contributions - Will you do monthly or a lump sum?

3. Consider increasing contributions - Can you afford to contribute more to maximise the bonus?

4. Review your LISA type - Is a Cash or Stocks & Shares LISA still right for your goals?

The £4,000 annual Lifetime ISA contribution limit and 25% government bonus make the LISA one of the most powerful savings tools available in the UK. By understanding how these limits work and adopting smart contribution strategies, you can maximise your free money from the government and build substantial savings for your future.

Whether you’re saving for your first home or planning for retirement, making full use of your LISA contribution allowance should be a priority in your financial plan.

Coming next in this series:  Part 6 will explore hoe to use your Lifetime ISA for retirement planning, including comparisons with pensions and strategies for long-term wealth building.

Part 6 will explore hoe to use your Lifetime ISA for retirement planning, including comparisons with pensions and strategies for long-term wealth building.

Have questions about Lifetime ISA contribution limits or want to share your LISA savings strategy? Drop a comment below or contact us directly for personalised guidance tailored to your specific circumstances and goals.

Subscribe below to receive regular updates on LISA rules, savings strategies, and the latest government announcements affecting your finances.

Get the Budget Planner