Table of Contents

ToggleWhen most people think of a Lifetime ISA, they think of first-time buyers saving for a deposit. But there’s another powerful use for LISAs that often gets overlooked: retirement planning. If you’re eligible to open a LISA (ages 18-39), it can be a valuable addition to your retirement strategy, offering tax-free growth, tax-free withdrawals, and a 25% government bonus on your contributions.

However, with the government announcing changes to the LISA in the Autumn Budget 2025, the retirement feature may only remain available for those who already have a LISA or open one before the new product launches (expected around April 2028). This makes understanding how to use a LISA for retirement more important than ever.

In this guide, we’ll explore everything you need to know about using your Lifetime ISA for retirement, how it compares to pensions, and whether you should consider opening one now to preserve this valuable benefit.

Quick Summary

Access age: You can withdraw penalty-free from age 60 onwards

Key tax benefit: Tax-free growth AND tax-free withdrawals (unlike pensions)

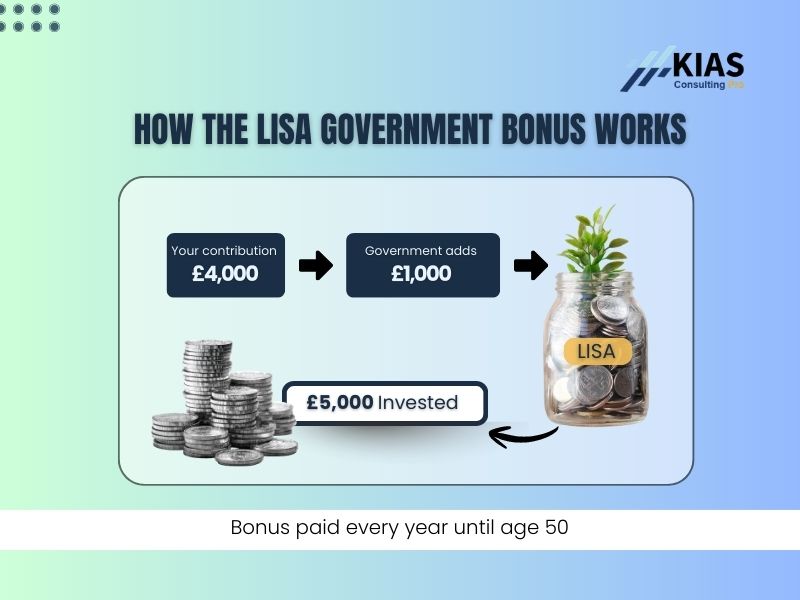

Government bonus: 25% on contributions up to £4,000/year (£1,000 max bonus)

2028 changes: Retirement feature may be removed for NEW savers after ~April 2028

Existing LISAs: Can continue indefinitely for retirement under current rules

Best for: Basic-rate taxpayers, self-employed, those wanting flexible access at 60

Can be combined with: Workplace pensions, personal pensions, other ISAs

Why Consider a LISA for Retirement?

While workplace pensions are often the go-to retirement savings vehicle (and rightly so, especially if your employer contributes), a Lifetime ISA offers unique benefits that make it worth considering as part of your broader retirement strategy.

The Unique Advantages of LISA for Retirement

1. Tax-free withdrawals at 60 Unlike pensions, which are taxed as income when you withdraw (except for the 25% tax-free lump sum), every penny you withdraw from your LISA is completely tax-free. This includes contributions, the government bonus, and all growth.

2. Earlier access than pensions You can access your LISA penalty-free from age 60, whereas most pensions can’t be accessed until at least age 66 (and this is likely to increase to 68 or beyond in the coming decades).

3. 25% government bonus Just like with pensions, you get a boost from the government, 25% on contributions up to £4,000 per year. For basic-rate taxpayers, this is equivalent to the 20% tax relief on pensions.

4. No forced annuity or drawdown rules Your LISA is your money. You can withdraw it all at once, take regular amounts, or leave it invested; there are no complex rules about how you must access it.

5. Protection from means-tested benefits,partly While LISA balances do count toward means-tested benefits (unlike pensions), the tax-free withdrawals mean you won’t be taxed on income in retirement, which can help with benefit calculations.

The 2028 Changes You Need to Know

What's Changing for Retirement Savers

The government announced in the November 2025 Budget that they’re consulting on a new ISA product to replace the Lifetime ISA. This new product will be for first-time buyers only, meaning the retirement feature will likely be removed.

What we know:

- The new product is expected around April 2028

- It will focus solely on first-time home buyers

- The retirement savings option will likely disappear for new savers

What this means for different people:

If You Already Have a LISA

Good news: You can keep your LISA and continue contributing for retirement indefinitely under the current rules. The government has confirmed this in Newsletter 20 (January 2026).

What you can do:

- Continue saving up to £4,000 per year until age 50

- Keep receiving the 25% government bonus

- Access your money tax-free from age 60

- Your LISA won’t be closed or forced to convert

If You Don’t Have a LISA Yet (Ages 18-39)

Strategic consideration: If you’re thinking about retirement and are eligible to open a LISA now, it may be worth opening one before the new product launches to preserve this retirement option.

Why opening now makes sense:

1. Immediate 25% government bonus on contributions (up to £1,000 per year) .

2. Tax-free investment/savings growth – all interest and investment returns grow tax-free

3. Tax-free withdrawals from age 60 – unlike pensions, which are taxed on withdrawal

4. Dual flexibility – you can still use it for a first home if your plans change before age 60

5. Locks in the retirement benefit that may not be available to new savers after 2028

You don’t have to contribute much right now. Even opening a LISA with just £1 secures your eligibility and starts your 12-month holding period. You can always increase contributions later when your financial situation allows.

For basics on opening a LISA, see Part 1: What is a Lifetime ISA?

LISA vs Pension: Which is Better for Retirement?

This is the big question. Should you save into a LISA or a pension for retirement? The answer isn’t straightforward; it depends on your circumstances, tax rate, and whether your employer offers pension contributions.

Direct Comparison: LISA vs Pension

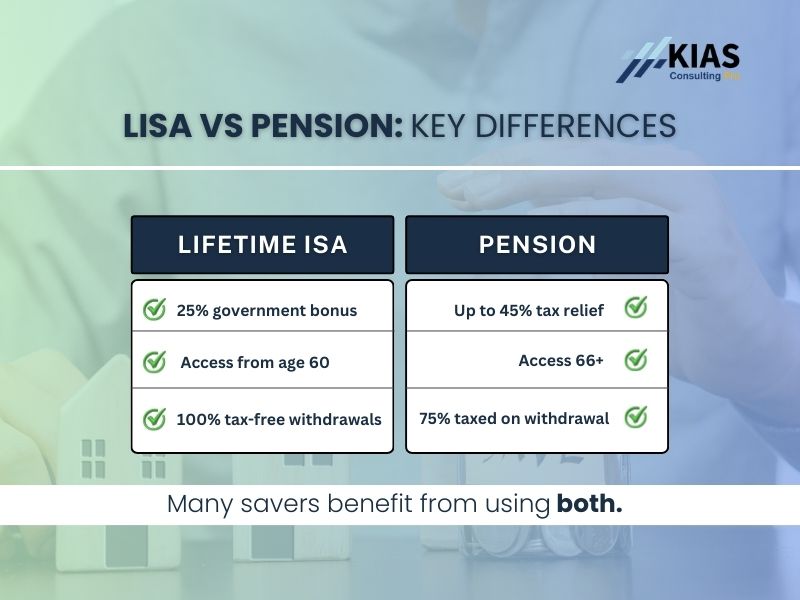

Feature | Lifetime ISA | Workplace/Personal Pension |

Government boost | 25% bonus (up to £1,000/year) | 20%-45% tax relief, depending on the rate |

Annual contribution limit | £4,000 | £60,000 (or 100% of earnings) |

Access age | 60 | Typically 66+ (rising to 68+) |

Tax on withdrawals | Completely tax-free | 25% tax-free, rest taxed as income |

Tax on growth | Tax-free | Tax-free |

Employer contributions | No | Yes (workplace pensions) |

Flexibility | High (access all or some anytime after 60) | Moderate (rules around drawdown) |

Counts for benefits | Yes | No (protected) |

Inheritance tax | Part of your estate | Usually outside your estate |

When a LISA is Better Than a Pension

This is the big question. Should you save into a LISA or a pension for retirement? The answer isn’t straightforward; it depends on your circumstances, tax rate, and whether your employer offers pension contributions.

Direct Comparison: LISA vs Pension

Feature | Lifetime ISA | Workplace/Personal Pension |

Government boost | 25% bonus (up to £1,000/year) | 20%-45% tax relief, depending on the rate |

Annual contribution limit | £4,000 | £60,000 (or 100% of earnings) |

Access age | 60 | Typically 66+ (rising to 68+) |

Tax on withdrawals | Completely tax-free | 25% tax-free, rest taxed as income |

Tax on growth | Tax-free | Tax-free |

Employer contributions | No | Yes (workplace pensions) |

Flexibility | High (access all or some anytime after 60) | Moderate (rules around drawdown) |

Counts for benefits | Yes | No (protected) |

Inheritance tax | Part of your estate | Usually outside your estate |

1. You’re a basic-rate taxpayer (earning under £50,270)

For basic-rate taxpayers, the LISA’s 25% bonus is equivalent to the 20% tax relief on pensions. But the LISA wins because:

- Withdrawals are completely tax-free (pensions are taxed)

- Earlier access at 60 vs 66+

- More flexibility in how you use the money

Example:

- LISA: Contribute £4,000, get £1,000 bonus = £5,000. Withdraw £5,000 at 60 (tax-free)

Pension: Contribute £4,000, get £1,000 tax relief = £5,000. Withdraw £5,000 at 66, pay tax = £4,000 (if you’re a basic-rate taxpayer in retirement)

2.You’re self-employed with no employer contributions

Without an employer-matching contribution, a LISA offers benefits similar to a personal pension for basic-rate taxpayers, but with greater flexibility.

3. You want an earlier retirement (age 60-65)

If you plan to retire before state pension age, a LISA gives you tax-free income from age 60 onwards to bridge the gap.

4. You value simplicity and flexibility

LISAs have simpler rules, your money is truly yours at 60, with no complex drawdown regulations.

When a Pension is Better Than a LISA

1. You’re a higher-rate taxpayer (earning £50,271-£125,140)

Higher-rate taxpayers get 40% tax relief on pensions, which is significantly better than the LISA’s 25% bonus.

Example:

- Pension: Contribute £6,000, but it only costs you £3,600 (after 40% tax relief)

LISA: Contribute £4,000, get £1,000 bonus = £5,000

2. Your employer contributes to your workplace pension

This is free money you can’t get elsewhere. Always contribute enough to your workplace pension to get the full employer match before considering a LISA.

Example: If your employer matches 5% and you earn £30,000:

- You contribute £1,500

- Employer contributes £1,500

- Total: £3,000 in your pension (double your contribution!)

3. You want to save more than £4,000 per year

The LISA’s £4,000 annual limit means it can’t be your sole retirement vehicle if you want to save substantial amounts.

4. You’re an additional-rate taxpayer (earning over £125,140)

With 45% tax relief, pensions are significantly more valuable than LISAs for very high earners.

The Power Strategy: LISA + Pension Combined

For many people, the best approach is to use both a LISA and a pension as part of a diversified retirement strategy.

The Recommended Priority Order

1. Immediate 25% government bonus on contributions (up to £1,000 per year)

.

2. Tax-free investment/savings growth – all interest and investment returns grow tax-free

3. Tax-free withdrawals from age 60 – unlike pensions, which are taxed on withdrawal

4. Dual flexibility – you can still use it for a first home if your plans change before age 60

5. Locks in the retirement benefit that may not be available to new savers after 2028

Real-Life Example: Sarah’s Combined Strategy

Sarah, age 32, earns £35,000 per year:

Her strategy:

- Workplace pension: Contributes 5% (£1,750), employer matches 5% (£1,750) = £3,500 total

- Lifetime ISA: Contributes £4,000, receives £1,000 bonus = £5,000 total

- Emergency fund: Keeps 3-6 months’ expenses in an easy-access savings account

Total retirement savings per year: £8,500 (plus growth)

By age 60, Sarah will have:

- Workplace pension: Approximately £213,000 (assuming 5% annual growth)

- Lifetime ISA: Approximately £304,000 (assuming 5% annual growth)

- Total retirement pot: £517,000 (before state pension)

This combined approach gives Sarah both employer contributions and the LISA’s tax-free benefits.

How Much Could You Have by Age 60?

Let’s look at realistic projections for LISA retirement savings.

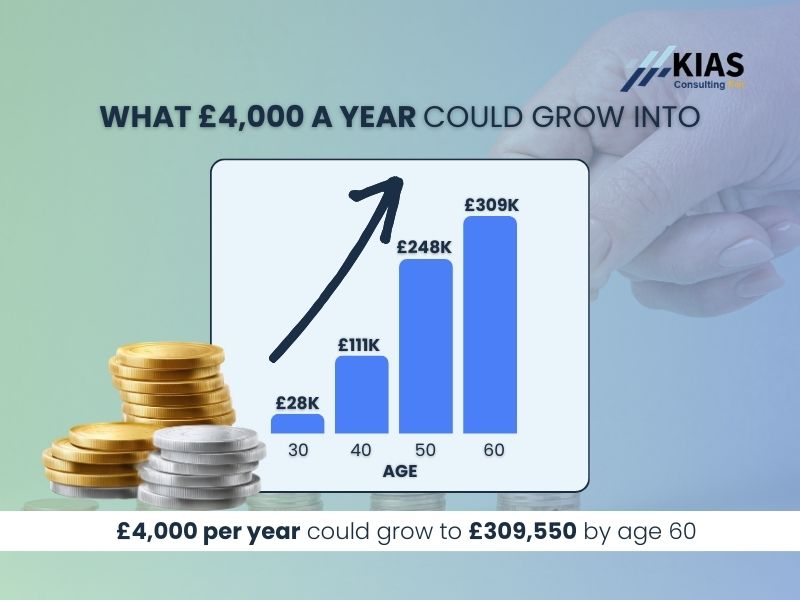

Scenario 1: Full Contributions from Age 25 to 50

Assumptions:

- Contribute £4,000 per year from age 25 to 49

- Receive £1,000 government bonus per year

- Invest in a Stocks & Shares LISA with 5% average annual growth

- 25 years of contributions (stop at age 50)

- Leave invested from age 50 to 60 (10 more years of growth)

Results:

Age | Total Contributed | Total Bonuses | Investment Growth | LISA Value |

30 (5 years) | £20,000 | £5,000 | £3,335 | £28,336 |

40 (15 years) | £60,000 | £15,000 | £36,370 | £111,371 |

50 (25 years) | £100,000 | £25,000 | £123,130 | £248,131 |

60 (35 years total) | £100,000 | £25,000 | £184,550 | £309,550 |

At age 60, you’d have approximately £309,550 completely tax-free.

That’s enough to:

- Withdraw £15,000 per year for over 20 years

- Supplement your state pension significantly

- Retire earlier or work part-time from age 60

Scenario 2: Starting Later (Age 35) with Smaller Contributions

Assumptions:

- Contribute £2,000 per year from age 35 to 49

- Receive a £500 government bonus per year

- 5% average annual growth

- 15 years of contributions

Results at age 60:

- Total contributed: £30,000

- Total bonuses: £7,500

- Investment growth: £38,421

- LISA value: £75,921

Even starting later with smaller contributions, you still build a significant tax-free retirement pot.

The Impact of Growth Rates

Here’s how different growth rates affect a £4,000/year contribution from age 25-49:

Growth Rate | Value at Age 60 |

3% (Conservative) | £243,114 |

5% (Moderate) | £309,550 |

7% (Growth-focused) | £403,318 |

Past performance doesn’t guarantee future results. Investments can go down as well as up.

For more on choosing between Cash and Stocks & Shares LISAs, see Part 3: Cash vs Stocks & Shares LISA

Tax Benefits: Why LISA Withdrawals are So Powerful

The Tax-Free Advantage

When you withdraw from your LISA at age 60+, everything is completely tax-free:

- Your original contributions

- The government bonuses

- All interest earned

- All investment growth

- All dividends received

This is different from pensions, where:

- Only 25% is tax-free

- The remaining 75% is taxed as income

- Higher withdrawals can push you into higher tax brackets

Real Example: £200,000 Withdrawal Comparison

Let’s say you have £200,000 saved and want to withdraw it all at age 60:

Lifetime ISA:

- Withdraw £200,000

- Tax paid: £0

- You receive: £200,000

Pension:

- Withdraw £200,000

- Tax-free portion (25%): £50,000

- Taxable portion (75%): £150,000

- Tax on £150,000 at basic rate (20%): £30,000

- You receive: £170,000

Difference: £30,000 more with a LISA

Assumes you’re a basic-rate taxpayer. Higher-rate taxpayers would pay even more tax on pension withdrawals.

Tax Planning Flexibility

Because LISA withdrawals are tax-free, they don’t:

- Affect your personal allowance

- Push you into higher tax brackets

- Trigger the higher-rate threshold

This gives you greater flexibility in retirement planning.

Who Should Use a LISA for Retirement?

LISA for Retirement is Ideal If You:

1. Are a basic-rate taxpayer The 25% bonus is equivalent to pension tax relief for basic-rate taxpayers, but with tax-free withdrawals.

2. Are self-employed Without employer pension contributions, a LISA offers similar benefits to a personal pension but with more flexibility.

3. Want to retire early (age 60-65) Access your tax-free LISA from age 60 to fund early retirement or reduce working hours before state pension age.

4. Value flexibility and simplicity LISAs have straightforward rules, your money is yours at 60 with no complex regulations.

4. Are under 40 and haven’t opened a LISA yet Lock in the retirement benefit before it potentially disappears for new savers after 2028.

5. Want a diversified retirement strategy Combine LISA with pensions and other ISAs for tax diversification in retirement.

When to Prioritise Pensions Over LISA

1. Your employer offers pension contributions Always get the full employer match first; it’s free money.

2. You’re a higher-rate taxpayer 40% or 45% tax relief makes pensions more valuable than the LISA’s 25% bonus.

3. You want to save more than £4,000/year for retirement Pensions have much higher contribution limits (£60,000 vs £4,000).

4. You won’t need the money until after 66 If you can wait for standard pension access age, pensions offer higher contribution limits.

Practical Strategies for LISA Retirement Planning

Strategy 1: The “Early Years Accelerator”

Best for: People in their 20s and early 30s

How it works:

- Maximize LISA contributions (£4,000/year) in your 20s and 30s

- Give your money maximum time to compound

- Consider Stocks & Shares LISA for higher growth potential

- Switch to a Cash LISA closer to age 60 to reduce risk

Benefit: Maximum compounding time means your money works harder.

Strategy 1: The “Early Years Accelerator”

Best for: Employees with workplace pensions

How it works:

- Contribute enough to the workplace pension to get a full employer match

- Put remaining savings into LISA (up to £4,000)

- Additional savings go back into pension or other ISAs

Benefit: You get both employer contributions and LISA tax-free benefits.

Strategy 3: The “Tax Diversification” Strategy

Best for: People wanting multiple retirement income sources

How it works:

- Build both a pension and a LISA

- In retirement, manage withdrawals from both strategically

- Use tax-free LISA withdrawals to avoid pushing yourself into higher tax brackets with pension income

Benefit: Greater control over your tax position in retirement.

Strategy 4: The “Last-Minute Lock-In”

Best for: People ages 38-39 who haven’t opened a LISA

How it works:

- Open a LISA before age 40 (even with just £1)

- Preserve the retirement option before the 2028 changes

- Increase contributions when finances allow

Benefit: Secures access to retirement LISA before it potentially disappears.

Common Questions About LISA for Retirement

Q: Can I access my LISA before age 60?

Yes, but you’ll face a 25% withdrawal penalty unless you’re: Buying your first home (under £450,000) Terminally ill with less than 12 months to live The penalty applies to your entire balance, including bonuses and growth

Q: What happens to my LISA if I die before 60?

Your LISA forms part of your estate and passes to your beneficiaries. There’s no penalty, and the money is inherited tax-free (though it may be subject to inheritance tax if your estate exceeds the nil-rate band).

Q: Can I withdraw my LISA gradually from age 60?

Yes! Unlike pensions with specific drawdown rules, you can withdraw as much or as little as you want from age 60 onwards. All withdrawals are tax-free.

Q: Should I stop contributing at age 50?

You must stop, LISAs don't accept contributions after age 50. However, your existing balance continues to grow tax-free, and you can access it penalty-free from age 60.

Q: Can I have both a LISA and a pension?

YAbsolutely! Many people combine both for a diversified retirement strategy. This is often the optimal approach.

Q: What if I've already bought my first home with my LISA?

You can keep your LISA and continue contributing for retirement under current rules. The retirement benefit remains available to you.

Q: Will my LISA affect my state pension?

No. LISA savings don't affect your entitlement to state pension, which is based on your National Insurance record.

Q: What if I’ve already maxed out my LISA contributions but want to save more?

You can use your remaining ISA allowance (£20,000 total minus your £4,000 LISA contribution = £16,000 remaining) to save into a Cash ISA or Stocks & Shares ISA. All ISA types offer tax-free growth on savings and investments.

How LISA Fits Into Your Complete Retirement Strategy

Using a Lifetime ISA for retirement shouldn't happen in isolation; it works best as part of a comprehensive financial plan.

The Complete Retirement Picture

1. State Pension (Foundation)

- Check your National Insurance record

- Top up voluntary contributions if needed

- Understand your projected state pension amount

- 📊 Read our State Pension Forecast Guide

2. Workplace Pension (Employer Match)

- Contribute at least enough to get the full employer match

- Consider increasing contributions as your salary grows

3. Lifetime ISA (Tax-Free Supplement)

- Contribute up to £4,000/year for the 25% bonus

- Access tax-free from age 60

4. Other ISAs (Additional Tax-Free Savings)

- Use remaining ISA allowance (£16,000 after LISA)

- Build additional tax-free retirement funds

5. Emergency Fund (Short-Term Security)

- Keep 3-6 months' expenses accessible

- Separate from retirement savings

Your Action Plan

Ages 18-30

- Open a LISA to start the clock (even with £1)

- Contribute what you can afford alongside the emergency fund

- Consider Stocks & Shares LISA for long-term growth

Ages 30-40

- Maximise employer pension match

- Increase LISA contributions toward £4,000/year

- Review and adjust investment strategy

Ages 40-50

- Continue LISA contributions until age 50

- Increase overall retirement savings

- Consider when to shift from growth to stability

Ages 50-60

- LISA continues growing (no new contributions allowed)

- Focus on pensions and other ISAs

- Plan retirement income strategy

Age 60+

- Access LISA tax-free as needed

- Coordinate withdrawals with pension and state pension

- Enjoy your retirement!

A Lifetime ISA can be a powerful tool for retirement planning, especially for basic-rate taxpayers, the self-employed, and anyone wanting tax-free income from age 60. While it shouldn’t replace a workplace pension (particularly if your employer contributes), it can significantly enhance your retirement provision.

Given the upcoming 2028 changes, if you’re eligible to open a LISA (ages 18-39) and interested in retirement planning, it’s worth considering opening one now to preserve this valuable benefit. Even if you only contribute £1 initially, you’ll lock in the option to use it for retirement, an option that may not be available to new savers after 2028.

The beauty of the LISA is its flexibility: you can use it for your first home before age 60, or for retirement from age 60 onwards. This dual purpose, combined with tax-free growth and withdrawals, makes it a unique and valuable part of a complete retirement strategy.

Next in this series: We’ve now completed all six parts of the Lifetime ISA series. Review the complete series at Lifetime ISA Series: Your Complete Guide to Saving and Buying Your First Home

Have questions about Lifetime ISA contribution limits or want to share your LISA savings strategy? Drop a comment below or contact us directly for personalised guidance tailored to your specific circumstances and goals.

Subscribe below to receive regular updates on LISA rules, savings strategies, and the latest government announcements affecting your finances.

Get the Budget Planner