🌟Introduction

📈 Investing Notice: This content is for informational purposes only and not investment advice. Investments can go up and down in value. Always do your own research and seek advice from a regulated professional. See full disclaimer. Table of Contents

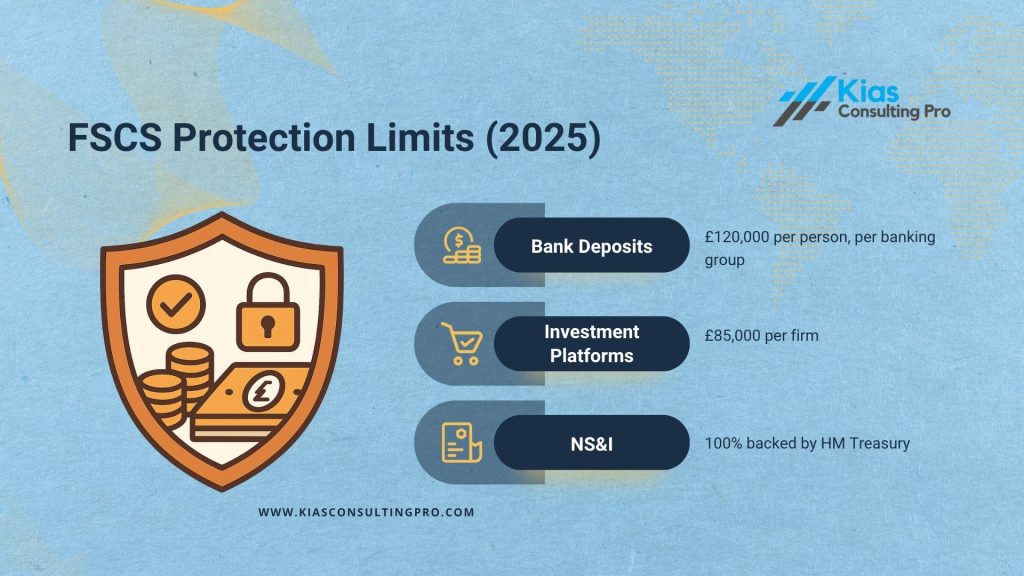

From 1 December 2025, the Financial Services Compensation Scheme (FSCS) is increasing the protection limit on eligible UK bank deposits from £85,000 to £120,000 per person, per banking group.

That’s a big step up in protection for savers, especially if you’re building larger cash reserves for emergencies, house deposits, or business needs.

But FSCS protection goes beyond just bank accounts. Many people don’t realise that investment platforms also benefit from FSCS protection if the firm itself fails, even though your investments can still go up and down in value.

In this guide, we’ll break down in simple terms:

- What FSCS protection is and how it works

- The new £120,000 limit and what it means for you

- Which banks and savings providers are covered

- How investment platforms are protected

- How much to keep with one bank

- A practical checklist to make sure your money is properly covered

What Is FSCS Protection? (Explained Simply)

The Financial Services Compensation Scheme (FSCS) is the UK’s official safety net for customers of authorised financial firms.

If a regulated bank, building society, credit union or investment firm fails and can’t return your money, the FSCS steps in (up to certain limits).

Key features of FSCS protection

- Automatic: if your provider is covered, you’re automatically protected

- Government-backed: the scheme is set up by law.

- Fast payouts for deposits: most eligible bank deposits are paid out within 7 days.

- Free: you don’t pay anything extra for FSCS protection.

Think of it as a backup plan: if the worst happens to your bank or platform, you’re not left with nothing.

The New £120,000 FSCS Deposit Limit in 2025

From 1 December 2025, the FSCS deposit protection limit will rise to £120,000 per person, per authorised banking group.

This means that if your bank, building society, or credit union fails after that date, you will be covered for eligible deposits up to £120,000.

This covers:

- Current accounts

- Easy-access savings accounts

- Fixed-term savings accounts

- Cash ISAs

- Some business accounts (separate business limit)

Previously, the limit was £85,000, so this is a significant increase in protection for UK savers.

Do you need to do anything?

No. If your bank or building society is FSCS-protected, the new limit applies automatically from 1 December 2025. You don’t need to fill in any forms or switch accounts to activate the higher limit.

Which Banks and Savings Providers Are Covered?

Most well-known UK institutions are covered by FSCS protection, as long as they’re authorised by the Financial Conduct Authority (FCA) or Prudential Regulation Authority (PRA).

High street banks (FSCS-protected)

Examples include:

- Barclays

- HSBC UK (including First Direct and M&S Bank)

- Lloyds Bank, Halifax, Bank of Scotland

- NatWest and Royal Bank of Scotland

- Santander UK

- TSB

- Virgin Money

Digital and challenger banks

Many newer banks and app-based providers are also protected, such as:

- Monzo

- Starling Bank

- Chase UK

- Kroo

- Metro Bank

- Zopa Bank

Building societies

Building societies are also covered, for example:

- Nationwide Building Society

- Coventry Building Society

- Yorkshire Building Society

- Leeds Building Society

- Skipton Building Society

Savings platforms and government-backed options

Some platforms act as “marketplaces” that allow access to savings accounts from multiple banks. Protection usually applies to the underlying bank, not the platform itself. Examples include:

- Raisin UK

- Hargreaves Lansdown Active Savings

- Flagstone

- Chip (protection applies via partner banks such as ClearBank, Allica Bank, etc.)

- Moneybox (FSCS protection applies to savings via its partner banks, and investment accounts are protected up to £85,000 if the firm fails)

And remember, NS&I (National Savings & Investments) is slightly different; it is 100% backed by HM Treasury, not just up to £120,000. That includes products like Premium Bonds and Direct Saver.

Banking Groups and Shared FSCS Limits

A crucial detail: the £120,000 limit applies per banking group, not per brand name.

Some brands share one banking licence. If you have money with more than one brand in the same group, they share a single £120,000 FSCS limit.

Examples of shared licences

- Lloyds Banking Group

- Lloyds Bank

- Halifax

Bank of Scotland

→ All share one combined £120,000 limit per person

- HSBC Group

- HSBC UK

- First Direct

M&S Bank

→ One £120,000 limit per person

- NatWest Group

- NatWest

- Royal Bank of Scotland

- NatWest

Ulster Bank (GB)

→ One £120,000 limit per person

Always check who actually holds the banking licence before deciding how to spread your savings.

How Much Should You Keep in One Bank?

The simple rule of thumb is:

Don’t hold more than £120,000 in eligible deposits with one banking group.

If you have under £120,000 in total savings

You can comfortably keep everything with one FSCS-protected institution and still be fully covered.

If you have £120,000 – £240,000

Consider splitting your savings between two separate banking groups.

For example:

- £120,000 with Barclays

- £120,000 with Nationwide

Both would be fully protected, as they’re different groups.

If you have more than £240,000

You may want to spread your money across three or more different groups and consider:

- Mixing banks and building societies

- using NS&I for extra government-backed security

- combining cash savings with appropriately risk-managed investments (if suitable)

Temporary High Balance Protection (Up to £1 Million)

The FSCS can protect up to £1 million for 6 months in certain life events, for example:

- Money from selling your main home

- Inheritance

- Divorce or civil partnership dissolution settlements

- Redundancy payments

- Insurance or compensation payouts

This is called temporary high-balance protection and is designed for situations where you may hold large sums of cash for a short period.

The protection starts from the date the money is deposited or the date you become entitled to it (whichever is later) and lasts for up to 6 months.

FSCS Protection for Investment Platforms

FSCS protection isn’t just for bank savings. It also applies to investment firms and platforms, but the rules and limits are different.

The investment protection limit: £85,000 per firm

FSCS investment protection covers up to:

£85,000 per person, per authorised investment firm

This applies where:

- The investment firm becomes insolvent and cannot return your investments, or

- There has been fraud, mismanagement or similar failure by the firm.

Examples of firms where this type of protection is relevant include:

- Hargreaves Lansdown

- Vanguard Investor

- AJ Bell

- Interactive Investor

- Fidelity Personal Investing

- Charles Stanley Direct

What FSCS does not cover for investments

FSCS does not protect you against:

- normal investment risk

- stock market falls

- poor performance of funds or shares

If the market goes down, that is part of investing, not something FSCS will compensate for.

How your investments are usually held

Most regulated UK platforms hold client assets in segregated client accounts or nominee arrangements, separate from the company’s own money. That means:

- Your investments are not treated as part of the firm’s own assets if it collapses

- Administrators aim to return your holdings to you

If there is a shortfall or assets cannot be returned, FSCS may step in up to the £85,000 limit.

What about cash held inside an investment account?

Uninvested cash inside:

- a Stocks & Shares ISA

- a SIPP (Self-Invested Personal Pension)

- a General Investment Account (GIA)

…is usually covered under investment firm protection (up to £85,000) rather than the £120,000 bank deposit limit, because it sits within an investment wrapper.

Always check with your provider to understand exactly how your cash is held and protected.

Joint Accounts, Business Accounts and Multiple Accounts

Joint Accounts

For a joint account, each person gets their own limit.

Example:

- A couple with £240,000 in a joint account:

- £120,000 is protected in the name of person A

- £120,000 is protected in the name of person B

So the full amount is covered under the new rules.

Multiple accounts with the same bank

If you have several accounts with the same banking group, the £120,000 limit applies to the total across all of them, such as:

- £50,000 in a current account

- £50,000 in a savings account

- £30,000 in a Cash ISA

Total = £130,000 → £120,000 protected, £10,000 above the limit.

Business accounts

Eligible business accounts also have FSCS protection, usually with their own limits separate from your personal savings. If you’re a company director or sole trader, it’s worth checking how your business deposits are protected.

Your FSCS Peace of Mind Checklist

Use this simple checklist to make sure your money is properly protected:

Your FSCS Protection Checklist (2025)

- List all your accounts – current, savings, ISAs and business.

- Group them by banking group, not just brand name.

- Check if any group exceeds £120,000 in deposits.

- Move excess cash to a different FSCS-protected institution if needed.

- Review your investment platforms – stay within the £85,000 limit per firm where possible.

- Understand how uninvested cash is held in your ISA / SIPP / GIA.

- Consider NS&I for extra government-backed security.

- Make a plan for large short-term balances (house sale, inheritance, etc.) using temporary high-balance protection.

- Review your protection at least once a year or whenever there’s a big change in your finances.

A few hours spent checking this can save a lot of worry later.

What Happens If Your Bank or Platform Fails?

Failures are rare, but it’s helpful to know the process.

If a bank or building society fails

- The FSCS is notified

- Your eligible balances are identified from the bank’s records.

- Compensation is paid automatically (usually within 7 days for deposits)

- You may receive the money by bank transfer or cheque.

If an investment platform fails

- Administrators are appointed to review and return client assets.

- Your investments are usually transferred to another provider or returned to you.

- If there is a shortfall that cannot be recovered, FSCS may compensate you up to £85,000 per firm.

You don’t need to “apply” in most standard cases; the process is handled for you.

How to Use FSCS Protection to Keep Your Money Safe in 2025

The increase in FSCS deposit protection to £ 120,000 is excellent news for UK savers. Combined with £85,000 protection for investment firms, it means both your cash and your investments benefit from strong safeguards when you use properly regulated providers.

To make the most of this:

- Avoid holding more than £120,000 in a single banking group

- Check that your banks, building societies and platforms are FSCS-covered

- Be aware of the £85,000 limit for investment firms.

- Use temporary high balance protection when large sums arrive.

- Review your setup regularly as your wealth grows.

A little organisation now can give you real peace of mind, so you can focus on growing your money, not worrying about whether it’s safe.

Important Disclaimer

This article is for informational and educational purposes only. It does not constitute financial advice or a personal recommendation. FSCS rules and limits can change, and how they apply may depend on your individual circumstances. Always check the latest information on the official FSCS website and consider speaking to a qualified financial adviser if you need advice tailored to your situation.

Master Your Money in 2025: A Complete Guide to Budgeting and the Best Tools That Actually Work

Find the best budgeting tools and planners to master your money in 2025. Learn how to create a budget that works for you using digital planners, binders, and smart budgeting systems.

The Truth About InvestEngine – My UK Review After 1 Year (2025)

I transferred my Vanguard SIPP to InvestEngine – and it wasn’t smooth sailing. Here’s my honest 2025 review of the platform after a full year of use, including why I’m giving them a second chance.

The Ultimate List of 7 Best Investing Books for Beginners (2025 Edition)

Discover the best investing books for beginners in 2025, seven timeless reads that simplify wealth-building, explain core investing principles, and help you start your journey toward financial independence with confidence.

How to Raise a Complaint to the UK Financial Ombudsman (With Real-Life Example)

I raised a complaint with the UK Financial Ombudsman when my SIPP transfer went wrong, and won. Here’s what happened, how the process works, and how to raise your own complaint with confidence.

The Smart Investor’s Secret: How ISAs Can Grow Your Wealth Tax-Free

ISAs remain one of the UK’s best-kept tax-free saving secrets. Discover how ISAs can grow your wealth tax-free and why starting early gives your money more time to compound. Whether you prefer saving or investing, learn how to make the most of your ISA in 2025 and beyond.

How to Switch Bank Accounts Safely (CASS Explained)

Want to switch bank accounts in the UK without stress? Learn how CASS works step-by-step, the protections built in, and smart tips to avoid mistakes.

Great overview! I’m curious: how often do people forget about the shared banking group limits? That seems likely to catch many savers off guard.

You’re absolutely right, the shared banking group limits do catch a lot of savers off guard!

Many people assume that each account they hold with a bank is separately protected, but under FSCS rules, protection is applied per banking group, not per individual account or brand.