🌟Introduction

📈 Investing Notice: This content is for informational purposes only and not investment advice. Investments can go up and down in value. Always do your own research and seek advice from a regulated professional. See full disclaimer. Table of Contents

In this guide, you’ll find investment fees explained in simple UK terms, what they are, where they hide, how they affect your returns, and practical ways to pay less in 2025 and beyond.

Investing is one of the most powerful ways to build long-term wealth, but there’s one quiet threat that can seriously shrink your future pot:

Fees.

They don’t feel dramatic in the moment. 0.25% here, 0.75% there. But over 20–30 years, those small percentages can add up to tens of thousands of pounds lost in costs rather than kept in your portfolio.

If you’re completely new to investing, you may find it helpful to start with my guide on ETFs and index funds. It includes a simple illustration showing how fees quietly compound over time:

➡️ Investing in ETFs & Index Funds for Beginners

By the end, you’ll understand:

- The main types of investment fees in the UK (platform, fund, trading and FX fees)

- How seemingly small fees can take £10,000–£50,000+ off your long-term returns

- Simple steps you can take to cut costs without overcomplicating your strategy.

Important: This article is for general information and education only and is not personal financial advice. Fees and platform terms can change, so always check the latest information on each provider’s website and consider speaking to a regulated adviser if you’re unsure.

What Are Investment Fees? (Explained Simply)

Investment fees are the costs you pay to invest. Some are obvious, others are hidden in small print, and many new investors don’t know they’re being charged at all.

Here are the core types of fees in the UK:

1. Platform Fees

This is what your investment platform (e.g., ISA or SIPP provider) charges you for using their service.

Platforms usually charge in one of two ways:

- A percentage of your portfolio (e.g., 0.15%–0.45%)

- A flat monthly or annual fee

How to know which is better for you:

Smaller portfolios usually benefit from percentage fees; larger portfolios often benefit from flat fees. But there are important exceptions; some platforms, like InvestEngine, charge £0 platform fees, making them ideal for beginners.

I’ll show you exactly which platform suits your portfolio size in the comparison table below.

2. Fund Fees (OCF, AMC, TER)

These are the ongoing costs charged inside a fund, whether it’s an index fund or an actively managed fund.

You may see terms like:

- OCF (Ongoing Charges Figure)

- AMC (Annual Management Charge)

- TER (Total Expense Ratio)

Index funds tend to be low-cost (0.06%-0.25%).

Actively managed funds tend to be higher-cost (0.5%-1%+).

If you need help choosing between them, my guide on How to Invest in Stocks in the UK offers a beginner-friendly overview.

➡️ Read next: How to Invest in Stocks in the UK (Beginner Guide)

3. Trading Fees

These cover the costs of buying and selling investments.

Examples include:

- Buy/sell charges

- FX fees on international shares (often 0.15% - 1.5%)

- Stamp duty on UK shares (0.5%)

- Bid-ask spreads (the hidden cost of trading)

Important: Platforms that offer “free trading” may charge in other ways, particularly through FX fees when you buy US or international stocks. I’ll cover this in detail in the FX fees section below.

4. Pension & Wrapper-Level Fees

Inside your workplace pension, SIPP or Lifetime ISA, fees may include:

- Annual admin fees

- Transfer-out charges

- Higher OCFs for default funds

If you’re building a long-term portfolio, my ETF and index fund guides explain how low-cost funds support diversification:

➡️ Read next: Investing in ETFs & Index Funds for Beginners

How to Check the Total Cost of Your Investments

Many investors don’t know where to find fee information. Here’s a simple checklist you can use today:

1. On your investment platform

Look for:

- "Fees” or "Charges" tab

- “Cost & Charges Statements” (platforms must provide these annually)

- Account settings or help section

2. On the fund factsheet

Search for:

- OCF (Ongoing Charges Figure)

- AMC (Annual Management Charge)

- “Transaction costs” section

You can usually find fund factsheets by searching “[Fund name] factsheet” on Google or on the fund provider’s website.

3. On your annual platform statement

You should receive:

- Summary of total fees paid

- Breakdown: Platform fees vs fund fees

- Admin fees

- Pension wrapper fees (if applicable)

Top tip:

If you can’t easily find your fee information, that’s often a red flag. The best platforms make fees transparent and easy to understand.

Why Investment Fees Matter More Than Most People Think

Fees may look small, but over time, they compound against you.

Once you see your investment fees explained with real numbers, the long-term impact becomes impossible to ignore.

Let’s break it down.

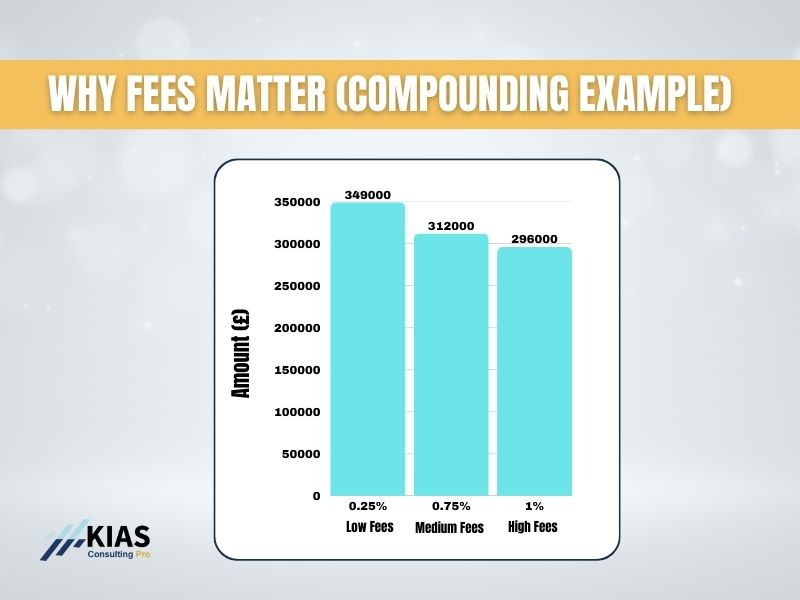

Example: The Cost of Fees Over 30 Years

If you invest £300 per month for 30 years at a 7% average return:

Scenario A: Low Fees (0.25%)

Final pot: Approximately £349,000

Scenario B: Medium Fees (0.75%)

Final pot: Approximately £312,000

Scenario C: High Fees (1%)

Final pot: Approximately £296,000

📉 Difference between 0.25% and 1% fees?

Over £50,000.

You didn’t invest any more money. You simply paid less in fees.

This is why understanding and managing fees matters.

Want to see exactly how fees affect YOUR portfolio?

Use my compound interest calculator to model different fee scenarios:

💡 Compound Interest Calculator

Ending balance: —

Total contributions: —

Total interest: —

Real (inflation-adjusted) balance: —

📊 Yearly summary

| Year | Start Balance | Contributions | Interest | End Balance |

|---|

Quick tip:

When using the calculator: important to consider if you have a small portfolio.

- Subtract your total fee % from your expected return

- Example: 7% return - 0.75% fees = input 6.25% as your growth rate

- Compare multiple scenarios to see the real cost of different fee levels

This helps you visualise exactly how much fees are costing you over time, and how much you could save by switching to a lower-cost option.

Breakdown: Types of Investment Fees Explained Clearly

This breakdown is part of helping you get your investment fees explained in a practical, easy-to-apply way.

1. Platform Fees

Platform fees usually range from:

- 0% to 0.45% per year, OR

- £4 to £12 a month (for certain providers like Vanguard)

What affects how much you pay?

- Your portfolio size

- Whether you hold funds or individual shares

- Whether you invest through an ISA, SIPP or GIA

- How often you trade

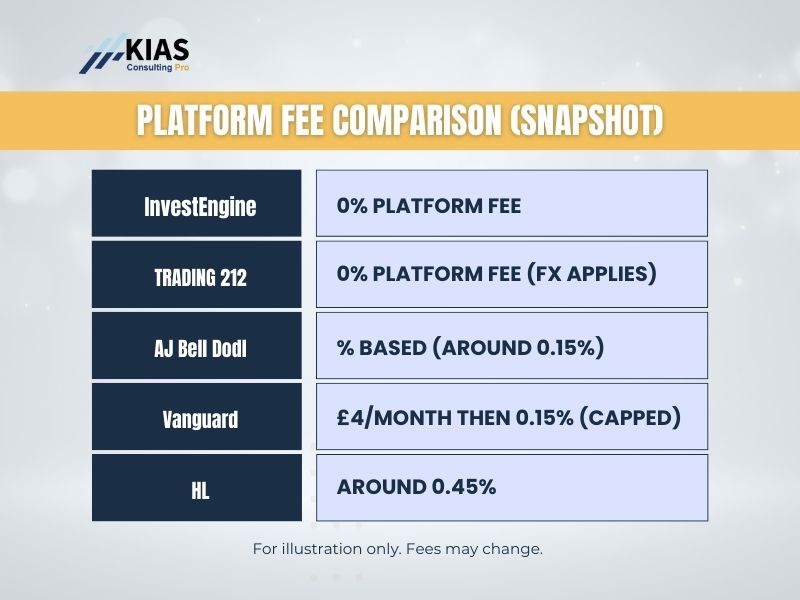

UK Platform Fee Comparison (2025)

To give you a feel for how platform fees differ, here’s a simplified snapshot of some well-known UK providers.

Note:

Fee information is based on publicly available data as at November 2025 and may change. This is not an exhaustive list. Always check each provider’s own website for the latest charges and terms.

Platform | Platform Fee (ISA/GIA) | Typical Minimum / Cap | Typical Use Case | Notes |

InvestEngine (DIY) | 0% platform fee on DIY portfolios | £0 | Cost-conscious investors building ETF-only portfolios | No platform fee on DIY ETF portfolios. You still pay the ETF’s OCF and any FX costs. |

Trading 212 | 0% platform fee | £0 | Investors who want both ETFs and individual shares | No platform fee; FX fee applies on non-GBP trades. See provider for details. |

AJ Bell Dodl | Percentage-based fee (e.g. around 0.15%) | Often with a low minimum (e.g. £1/month) | Investors who prefer a mix of funds and shares in a simple app | Charges vary by account type and investment. Check the current Dodl fee schedule. |

Vanguard | Percentage-based fee with a low minimum (e.g. £4/month, then around 0.15%, capped) | Minimum and cap apply | Investors who like Vanguard funds and a straightforward platform | Limited to Vanguard’s own funds/ETFs. Platform fee structure and caps may change. |

Hargreaves Lansdown | Percentage-based fee (e.g. around 0.45% on funds) | No cap on some account types | Investors who value research tools and a wide investment range | Fees and caps differ by account and investment type. Check HL’s current charges. |

Platform Fee Tipping Points: How Costs Change as Your Portfolio Grows

As your portfolio grows, different fee structures can become more or less cost-effective. The figures below are illustrative only, they’re not recommendations.

➤ Around £0 – £8,000:

Percentage-based or minimum-fee platforms can feel relatively expensive in pounds-and-pence terms. Some investors in this range look at providers with no platform fee (but they’ll still pay fund charges and any FX costs).

➤ Around £8,000 – £32,000:

At this level, low percentage-based platforms and capped/minimum-fee platforms may work out similarly. It’s worth comparing both the percentage fee and any minimum charges.

➤ Around £32,000 – £80,000:

Percentage-based fees become more noticeable in £ terms. For some investors, platforms with lower percentages or caps can reduce total costs.

➤ Around £80,000 – £250,000+:

For larger portfolios, even small percentage differences add up. Some platforms apply caps on fees above certain levels, which can limit costs, but it’s still important to weigh this against fund choice, service and features.

Example: Total Annual Platform Fees

Let’s see what you’d actually pay as platform fee:

Portfolio Size | InvestEngine | Trading 212 | AJ Bell | Vanguard | HL |

£5,000 | £0 | £0 | £12 | £48 | £22.50 |

£10,000 | £0 | £0 | £15 | £48 | £45 |

£25,000 | £0 | £0 | £37.50 | £48 | £112.50 |

£50,000 | £0 | £0 | £75 | £75 | £225 |

£100,000 | £0 | £0 | £150 | £150 | £450 |

£250,000 | £0 | £0 | £375 | £375 (capped) | £1,125 |

Key insight: Zero-fee platforms stay at £0 regardless of portfolio size, but they may have limitations (ETF-only for InvestEngine, FX fees for Trading 212).

2. Fund Fees (OCF/AMC)

These are the ongoing costs charged by the fund manager.

Common fee levels

- Index funds: 0.06%-0.25%

- Active funds: 0.5%-1%+

- Specialist funds (tech/ethical): 0.4%-1%+

What you get for the fee

- Index fund: Tracks the market automatically (passive management)

- Active fund: Manager tries to beat the market (active stock picking)

- Multi-asset fund: Offers "all-in-one" investing across different assets

- ESG fund: Ethical filters and screening based on environmental/social criteria

Important to know:

Even on zero-fee platforms like InvestEngine and Trading 212, you still pay the fund’s OCF. This is unavoidable, it is automatically deducted from the fund before returns are calculated.

For more on building a diversified portfolio with low-cost funds:

➡️ Read next: Building & Managing a Stock Portfolio in the UK – Part 1

➡️ Read next: Diversifying Your Investments (Part 2)

3. Trading, FX & Hidden Fees

Many investors forget these costs, but they can be more expensive than your platform fee.

Trading Fees

- Buy/sell fees (charged per trade)

- Some platforms charge £5–£12 per trade

- Others offer free trading (but check for other fees)

Stamp Duty

- 0.5% on most UK shares

- Not charged on funds or ETFs

- Automatic; deducted when you buy

FX Fees: The Silent Portfolio Killer for US Stock Investors

If you invest a lot in US stocks or global ETFs, FX fees can become a significant part of your total costs. For example, a 1% FX fee on £10,000 of US share purchases in a year is £100 in currency conversion charges alone.

Some platforms charge a lower FX percentage than others. A lower FX fee (for example, 0.15% rather than 1%+) can reduce these costs, especially for investors who trade international shares regularly. The exact FX percentage and how it’s applied are set by each platform and can change, so it’s important to check the provider’s latest fee information.

Example:

- You invest £1,000/month into US stocks

- Your platform charges a 0.5% FX fee

- Annual FX cost: £60

- Over 10 years: £600+ (plus lost growth on that £600)

For a £25,000 portfolio investing 50% in US stocks, a 1% FX fee costs you £125/year just on currency conversion. Further reading on Trading 212 and InvestEngine reviews.

UK Platform FX Fees (2025)

Trading 212 | 0.15% | One of the lowest FX fees among major UK platforms. Applies on non-GBP trades. |

InvestEngine | 0.45% | FX fee applies only when buying non-GBP ETFs. Many popular ETFs on the platform are GBP-listed, so FX may not apply. No platform fee on DIY portfolios. |

Vanguard | 0% on funds | No FX fee on Vanguard funds/ETFs, but product range is limited to Vanguard-only options. |

AJ Bell Dodl | 0.95% | FX fee applies on non-GBP trades. Cost may add up for frequent US stock purchases.g |

Hargreaves Lansdown | 1%+ | FX fee varies by trade size and account type. Higher than many low-cost platforms. |

If you’re investing heavily in US stocks or international ETFs, Trading 212’s 0.15% FX fee can save you hundreds of pounds per year compared to other platforms.

I’ve written comprehensive guides on how Trading 212 works and how to use it effectively:

➡️ Trading 212 UK Review 2025

➡️ Complete Guide: Investing on Trading 212

How to Minimise FX Fees

- Use platforms with low FX charges for US stocks (Trading 212 is currently the cheapest at 0.15%)

- Consider UK-listed global funds: no FX conversion needed (e.g., Vanguard FTSE All-World)

- Buy in larger, less frequent trades: you pay FX fees each time you convert currency

- Use GBP-traded ETFs when available, e.g., VUSA (GBP) vs VOO (USD), both track the S&P 500 on budget is progress

Bid–Ask Spread

This is the “hidden” cost between the buying price and selling price.

Higher on:

- ETFs with low trading volume

- Individual shares (especially smaller companies)

- Specialist funds

Lower on:

- Popular ETFs like Vanguard FTSE All-World

- Large-cap stocks

- Highly liquid investments

You don’t see this cost on your statement, but it affects the price you pay when buying and the price you receive when selling.

Spotlight: Zero-Fee Platforms for Beginners

If you’re just starting or have under £30,000 to invest, zero-fee platforms offer exceptional value.

InvestEngine: Best for ETF Investors

What you pay:

- Platform fee: £0

- Fund fees only (OCFs typically 0.13%-0.25%)

- No trading fees on ETFs

What to watch:

- Limited to ETFs (no individual stocks)

- Managed portfolio option available (0.25% fee)

- FX fee: 0.45% on currency conversions

Who it’s for:

- Beginners who want simple, low-cost index investing

- Long-term investors using ISAs or SIPPs

- Anyone building a passive ETF portfolio

I’ve written a comprehensive review covering everything from setup to hidden costs:

➡️ InvestEngine UK Review 2025: Is It Worth It?

Consumer protection note: Like all UK platforms, InvestEngine is FCA-regulated. If you ever have issues with any platform, my guide explains your rights:

Trading 212: Best for Flexibility

What you pay:

- Platform fee: £0

- FX fee: 0.15% (lowest in the UK)

- No trading fees on stocks or ETFs

What you get:

- Access to individual stocks AND ETFs

- Fractional shares

- AutoInvest feature (automatic portfolio building)

- ISA and General Investment Account options

Who it’s for:

- Investors who want individual stock exposure

- Anyone buying US stocks regularly (lowest FX fees)

- People who want more flexibility than ETF-only platforms

Quick definition:

Investment fees are the platform, fund, trading and currency conversion costs you pay to invest. They are usually expressed as a percentage per year (for ongoing fees) or as fixed charges when you buy/sell.

Frequently Asked Questions About Investment Fees

1. What is a reasonable investment fee in the UK?

For index funds and ETFs, total costs under 0.4% per year (platform plus fund fees combined) are generally considered low. Active funds often cost more, but higher costs do not guarantee better performance.

2. How can I check what fees I am currently paying?

You can usually find your fees in three places:

- Your platform’s fees or “charges” page

- Your annual “cost and charges” statement

- Each fund’s factsheet (look for the Ongoing Charges Figure, or OCF)

If this information is hard to find, that is often a warning sign that costs are not being presented clearly.

3. Are zero-fee platforms really free?

Not completely. Platforms that advertise no platform fee may still charge:

- Fund fees (OCF/TER), which all funds have

- Foreign exchange (FX) fees on non-GBP investments

- Other charges depending on the products offered

However, for many investors they can still reduce overall costs compared with some traditional platforms.

4. Should I move an old pension to reduce fees?

It depends on the type of pension and any benefits attached to it. Before moving a pension, always check for:

- Exit or transfer fees

- Protected benefits, such as guaranteed annuity rates

- Defined benefit or final salary schemes (these are usually not suitable to transfer)

- Employer contributions, if it is still an active workplace scheme

If an old pension has no special protections and charges high fees, reducing costs may save money over time, but this is not personal advice.

5. Do fees matter more than fund performance?

Over the long term, fees have a very reliable impact because they are charged every year, whereas performance can be unpredictable. Lower fees allow more of your returns to stay invested and compound for your future.

6. What is the difference between AMC and OCF?

The AMC (Annual Management Charge) is the manager’s fee only. The OCF (Ongoing Charges Figure) includes the AMC plus most of the fund’s regular running costs, such as administration, legal and audit fees. The OCF is usually the best figure to use when comparing funds.

7. When should I consider switching platforms?

Many investors review their platform once a year, especially if:

- Their portfolio has grown significantly since they opened the account

- They are paying high percentage-based fees on a large portfolio

- They invest heavily in international shares and face high FX fees

- The platform no longer fits the way they prefer to invest

It rarely makes sense to switch just for the sake of it, but staying on an expensive platform out of habit can be costly over decades.

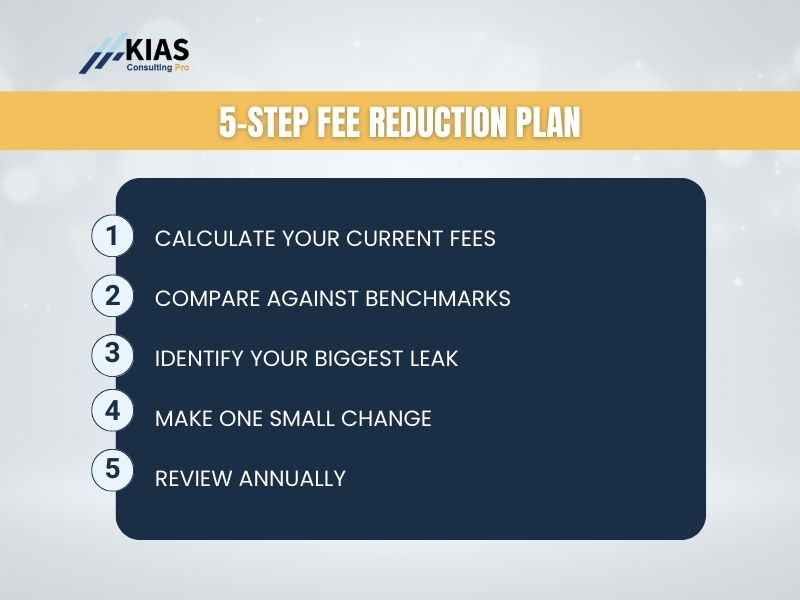

Your Action Plan: Reducing Investment Fees in 2025

If you only do one thing after reading this, let it be this: find out what you’re actually paying. Once you know your total fee level, the next right step becomes much clearer.

Here’s a simple, low-stress action plan:

Step 1: Work out your total annual fees

Check:

- Your platform’s fee page or cost & charges statement

- The OCF on your main funds or ETFs

- Any regular trading or FX costs (if you buy individual shares or overseas investments)

Add them up into a rough total % (for example: 0.25% platform + 0.18% fund + 0.10% FX approximately, 0.53% total).

Step 2: Use some simple benchmarks

As a rough guide (not advice):

- Under 0.4% total → very low, cost-efficient

- 0.4%–0.75% → reasonable, worth keeping an eye on

- Above 1% → worth reviewing, especially on larger portfolios

This isn’t about chasing perfection, just spotting where you might be leaking more in fees than you realised.

Step 3: Identify the biggest leak

Ask yourself:

- Is most of the cost coming from my platform, funds, or FX?

- Am I paying active-fund prices for “market-average” performance?

- Has my portfolio grown, but I’m still on high percentage fees?

You don’t need to fix everything at once. Just pick the biggest pain point first.

Step 4: Make one small change

Choose one of the following to action this month:

- Switch one high-fee fund to a comparable lower-cost option

- Reduce unnecessary trading and stick to a buy-and-hold approach.

- Review whether your platform’s pricing still makes sense for your portfolio size.

- Look into whether an old high-fee pension could be consolidated (if appropriate)

Small, consistent changes can save you thousands over time.

Step 5: Review once a year

Set a calendar reminder to review fees annually. Platforms change, fund charges move, and your portfolio grows. A 20-30 minute review each year is enough to keep you on track.

Summary: Key Takeaways

- Fees are one of the few parts of investing you can control. You can’t control the market, but you can control what you pay to access it.

- Small percentages make a big difference over 20–30 years. Moving from 1%+ in total fees to around 0.4% can mean keeping tens of thousands more in your own pocket.

- Your actual cost is a combination of platform fees, fund OCFs, trading costs, FX fees and pension/admin charges, not just one number.

- Zero- or low-fee platforms and low-cost funds can be very cost-effective, but every option comes with trade-offs. Always weigh fees alongside features, fund choice and your own needs.

- You don’t need to overhaul everything overnight. One thoughtful change at a time, reviewed annually, is enough to meaningfully improve your long-term outcomes.

Every pound you don’t pay out in unnecessary fees is a pound that stays invested and has the chance to compound for your future.

Before You Go: Get Ongoing UK Investing Education

If you found this helpful and want more clear, jargon-free UK investing content:

- 📧 Join my email list for weekly financial education, practical guides on ISAs, pensions, investing platforms and building long-term wealth (without giving personal advice).

- ▶️ Subscribe on YouTube – @WealthWiseCompass for bite-sized videos where I break down the same ideas visually: fees, compound interest, ISA strategies, pension basics and more.

Staying informed is one of the most powerful ways to protect yourself from unnecessary costs and make confident, long-term decisions with your money.

- 📧 Join my email list for weekly financial education, practical guides on ISAs, pensions, investing platforms and building long-term wealth (without giving personal advice).

Related Guides You Might Find Helpful:

Get the Budget Planner