Retiring early in the UK is a dream for many, but is it realistic? In this post, we’ll explore what early retirement means in the UK, the key things to consider, and how your pension can help make it a reality. Whether early retirement means stopping work entirely at 55, switching to part-time at 60, or reaching financial independence long before State Pension age, this guide is designed to give you precise, practical guidance to start planning.

What Does Early Retirement Mean in the UK?

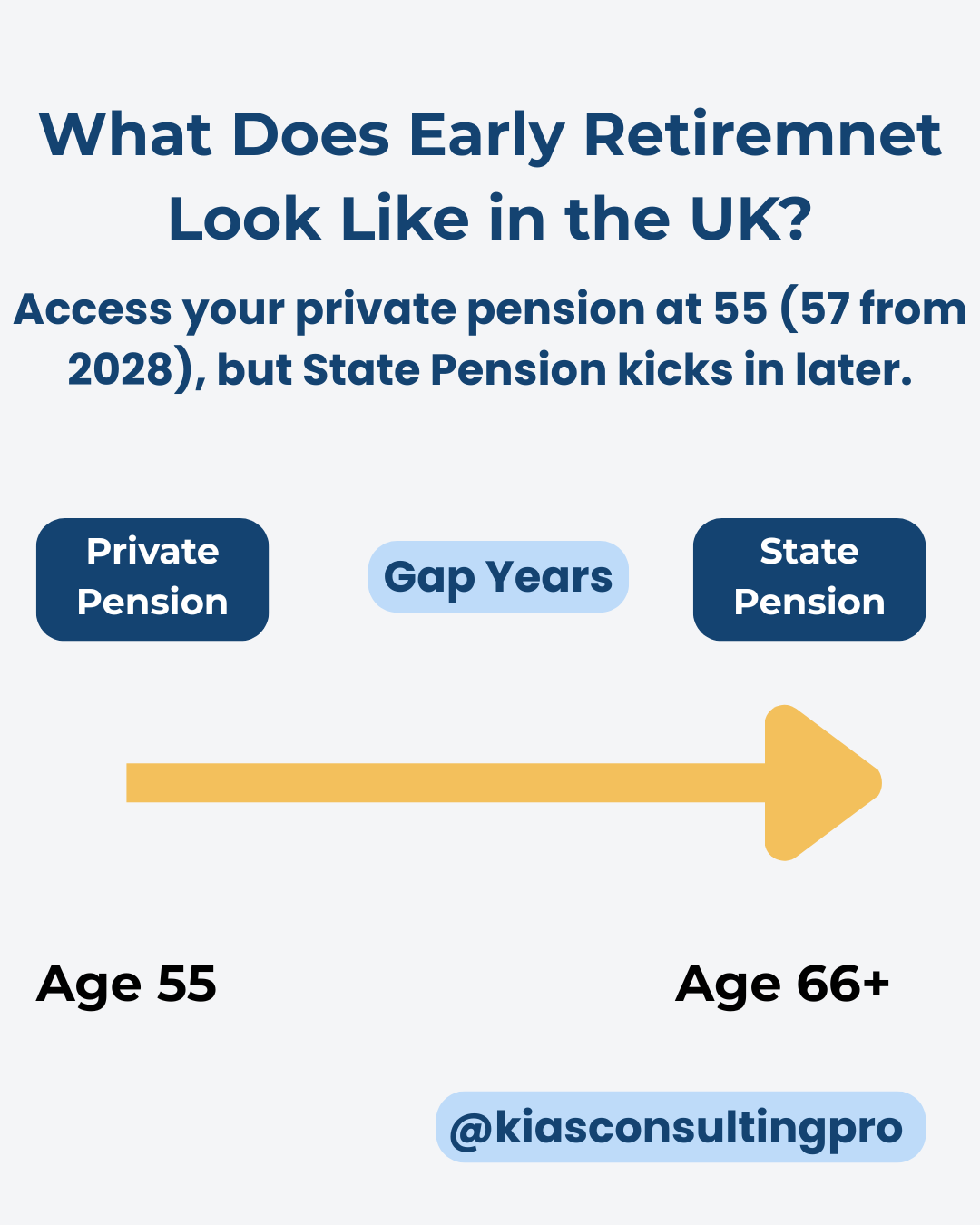

Early retirement in the UK means retiring before the State Pension age (currently 66 and rising). That might be age 55, 57, 60, or when you can financially step away from full-time work.

You can access private pensions (like personal pensions, SIPPs, or workplace pensions) from age 55 (rising to 57 in 2028), but you cannot access your State Pension until you reach the official age set by the government. If you want to retire early early in the UK, you’ll need to rely on your private pension and other savings to cover the gap.

✅ Learn how pensions work in the UK

Can You Afford to Retire Early in the UK?

This is the key question. To retire early, you’ll need to:

Estimate your annual living costs in retirement.

Work out how much income you’ll need before your State Pension kicks in.

You could check how much you have saved in pensions, ISAs, or other investments.

A helpful rule of thumb is the 4% rule—this suggests you can safely withdraw 4% of your pension pot each year without running out of money. So to generate £20,000 per year, you’d need around £500,000 saved. This means if you have £ 500,000 in your pension, you can withdraw 4% of this amount, which is £ 20,000, annually without depleting your pension fund.

📌 Use the MoneyHelper Pension Calculator to check your numbers

Real-Life Example: Emma’s Early Retirement Plan

Emma is 55 and wants to retire from full-time work. She has:

£240,000 in her pension, which she has been contributing to for the past 30 years

£60,000 in her Stocks & Shares ISA

A paid-off home

Emma plans to live on £20,000 yearly until her State Pension starts at 67. That’s 12 years = £240,000 needed. She uses her ISA for flexible income and gradually draws from her pension. With careful planning and a modest lifestyle, Emma retires early without financial stress.

Pros and Cons of Retiring Early in the UK

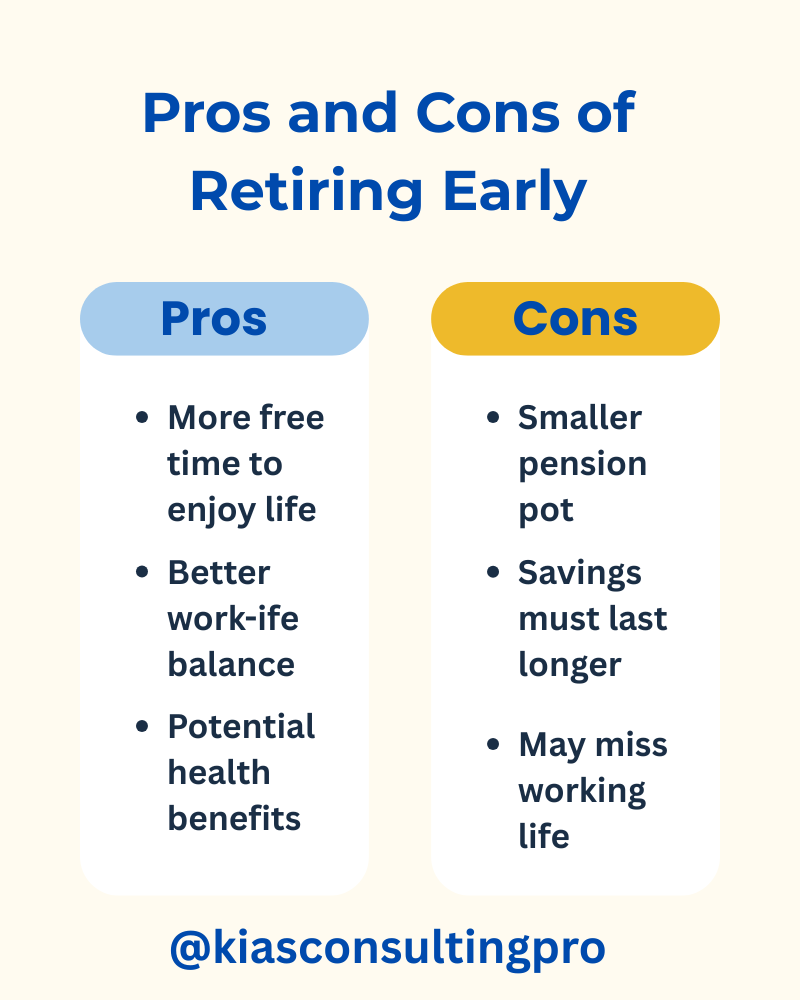

Pros:

More time for hobbies, family, and personal projects

Better health in retirement (you retire while still active)

Opportunity to travel or change careers

Cons:

A longer retirement means needing more savings.

No access to the State Pension or some benefits until later

Your pension has less time to grow

How to Retire Early in the UK– Step-by-Step

Here’s a simple checklist:

Set your retirement age target (e.g. 55, 60, etc.)

Estimate annual expenses you’ll need

Add up your savings (pension, ISA, savings, other assets)

Use a retirement calculator to see if your pot is enough.

You could check if you have any pension gaps or missed contributions.

Make a top-up plan (e.g. increase pension/ISA savings now)

Plan for phased retirement (e.g. part-time work or freelancing)

✅ Check your State Pension forecast

Book a 1:1 session for personalised guidance.

Vanguard Review 2025: What You Need to Know About Fees & Funds

Vanguard review 2025 for UK investors: fees explained (£4/month under £32k; 0.15% cap above), beginner-friendly funds (LifeStrategy, Target Retirement, global index/ETFs), and when to consider alternatives. Includes quick links to ISA, Junior ISA, ETF and pension-transfer guides.

UK Credit Reference Agencies Explained: How to Check and Improve Your Credit Score

Learn how UK credit reference agencies work, why Experian, Equifax, and TransUnion matter, and how to monitor and improve your credit score effectively.

How to Choose the Best Junior Stocks & Shares ISA (JISA) in the UK 2025: Top Providers Reviewed

Looking for the best Junior Stocks & Shares ISA in the UK? Compare top providers for 2025, discover pros and cons, and find the ideal JISA for your child’s future.

How to Open a Hargreaves Lansdown JISA: The Ultimate Step-by-Step Guide

Looking to open a Hargreaves Lansdown Junior ISA? Follow this beginner-friendly, step-by-step guide and learn the pros, cons, and answers to frequently asked questions.

Unlock Financial Independence: The Ultimate Guide to the Best Vanguard ETFs and Index Funds

Imagine a life free from money worries. Learn how to confidently invest in Vanguard ETFs and index funds with this comprehensive UK beginner’s guide. Explore top funds, platform fees, common mistakes to avoid, and access a FREE 5-day video course to kickstart your investment journey toward financial independence.

Trading 212 Cash ISA: How to Maximise Your Tax-Free Savings (Complete Guide)

This comprehensive guide explores the benefits of Trading 212 Cash ISA, including tax advantages, competitive interest rates, and easy account setup. Compare it with other top Cash ISAs and learn how to maximise your savings in 2025.

How to Leverage Your Assets and Boost Your Income to Get Out of Debt Faster 2025

Struggling with debt? Learn how to use your assets and side hustles to accelerate your debt repayment journey in 2025. Practical, actionable tips to help you regain control of your finances.

Lifetime ISA Withdrawal Penalties Explained: How to Avoid Costly Mistakes

Understand the critical withdrawal rules for your Lifetime ISA (LISA) and avoid costly penalties. Learn when you can withdraw funds penalty-free, the impact of the 25% early withdrawal charge, and how to navigate joint purchases effectively in this detailed UK guide.

Are You Losing Money in a Default Pension Fund? Book Your Free Review Today

Have you changed jobs and left your pension behind? Many workplace pensions are stuck in default funds that underperform. In this blog, discover why a free 1:1 pension review could help you grow your retirement savings and take control of your future. Perfect for anyone unsure where their pension stands.

Trading 212 Review UK: A Simple Guide to the Best Commission-Free App for New Investors

Wondering if Trading 212 is the right app to start your investment journey? This beginner-friendly review breaks down the key features, fees, and tips you need to know.

Cash vs Stocks & Shares LISA (2025): How to Choose the Best Lifetime ISA

Explore the key differences between Cash and Stocks & Shares Lifetime ISAs to find the best fit for your financial goals in 2025. Learn about risk, growth potential, and how each option supports your journey to homeownership or retirement.

Lifetime ISA for First-Time Buyers: How to Secure Your First home in the UK

Are you planning to buy your first home? A Lifetime ISA (LISA) can boost your deposit by 25%. This guide simplifies how it works, its eligibility, and its essential rules.