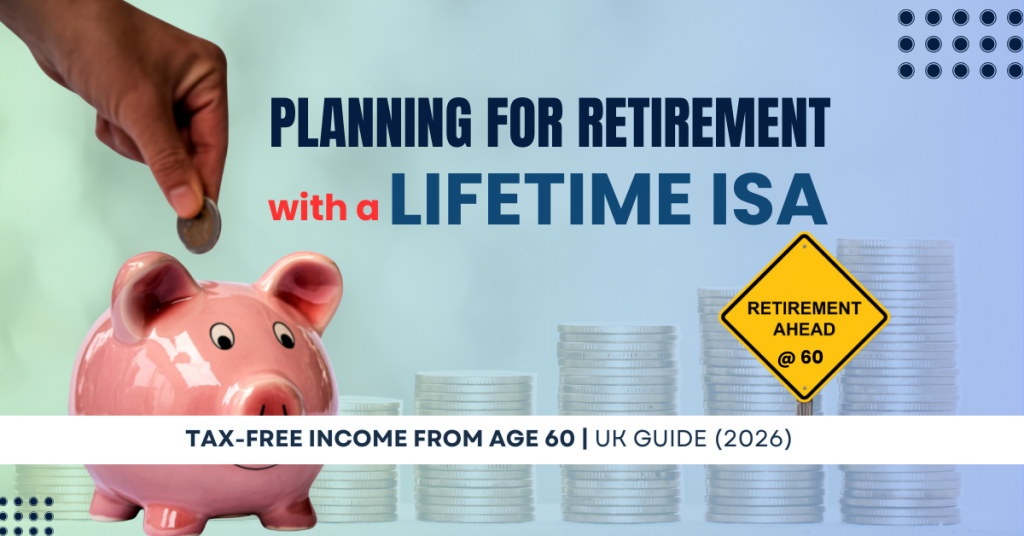

Planning for Retirement with Your Lifetime ISA: Complete UK Guide (2026)

Planning for retirement with a Lifetime ISA offers unique advantages that many savers overlook. With tax-free growth, tax-free withdrawals from age 60, and a 25% government bonus, LISAs can be a powerful addition to your retirement strategy—especially for basic-rate taxpayers and the self-employed.

This comprehensive guide explains everything you need to know about using your LISA for retirement, including detailed comparisons with pensions, realistic projections of what you could have by age 60, and strategic advice on combining LISAs with workplace pensions.

Importantly, with the government planning to remove the retirement feature for new savers around April 2028, understanding your options now is crucial. If you’re eligible (ages 18-39) and interested in retirement planning, opening a LISA before the changes could preserve this valuable benefit.

Learn how to make the most of your LISA for a more secure financial future.

Lifetime ISA Contribution Limits and Bonus Explained (2026 Guide)

Understanding Lifetime ISA contribution limits is crucial for maximising your savings in 2026. The annual limit of £4,000 determines how much government bonus you’ll receive—making it one of the most important aspects of your LISA strategy.

In this comprehensive guide, we explain everything you need to know about LISA contribution limits, including how the £4,000 annual cap works, how it fits within your overall £20,000 ISA allowance, and what happens if you contribute too much.

We’ll also explore practical strategies like monthly versus lump sum contributions, when to contribute for maximum growth, and how to coordinate your LISA with other ISAs. Plus, learn about the 2026 Budget update confirming limits remain frozen until 2031.

Whether you’re saving for your first home or planning for retirement, this guide will help you make the most of your Lifetime ISA contribution allowance and maximise your government bonus.

Will the Lifetime ISA Be Scrapped? Everything We Know About the 2028 Changes

Is the Lifetime ISA being scrapped? Learn what the proposed 2028 changes mean, what stays the same, and how to protect your bonus, retirement options, and home-buying plans.

Hargreaves Lansdown Fee Changes March 2026: What You Really Need to Know

A 515-character summary explaining the key changes (0.45% → 0.35% platform fees, new £1.95 fund charge) and positioning the article as a guide to help readers calculate their impact and decide whether to stay or switch.

Capital Gains Tax on Property in the UK (2025/26)

Capital gains tax on property in the UK can apply when selling a buy-to-let, second home, or inherited property. This 2025/26 guide explains the rules, Private Residence Relief, allowable costs, and the 60-day reporting deadline.

How to Reduce Capital Gains Tax Legally in the UK (2025/26): 10 Strategies That Can Help

Learn how to reduce Capital Gains Tax legally in the UK for 2025/26. 10 practical CGT strategies, clear examples, and a free CGT calculator.