How Much Should I Contribute to My Pension?

A Beginner’s Guide to Building a Secure Retirement

💬 Want to know how much to contribute to your pension in the UK and how to make every pound count?

This beginner’s guide breaks it down step-by-step so you can feel confident about your retirement savings.

Why Your Pension Contributions Matter

Planning for retirement isn’t just about having a pension; it’s about ensuring you’re putting enough into it. Even small, consistent contributions can grow into a meaningful income later in life, providing a secure and comfortable retirement. This guide will explain how much you should contribute, how to maximise employer support, and how pensions compare to ISAs and savings accounts.

📅 This is Part 3 of our UK Pension Series. We recommend catching up on Part 1 and Part 2 to ensure you’re fully informed and prepared.

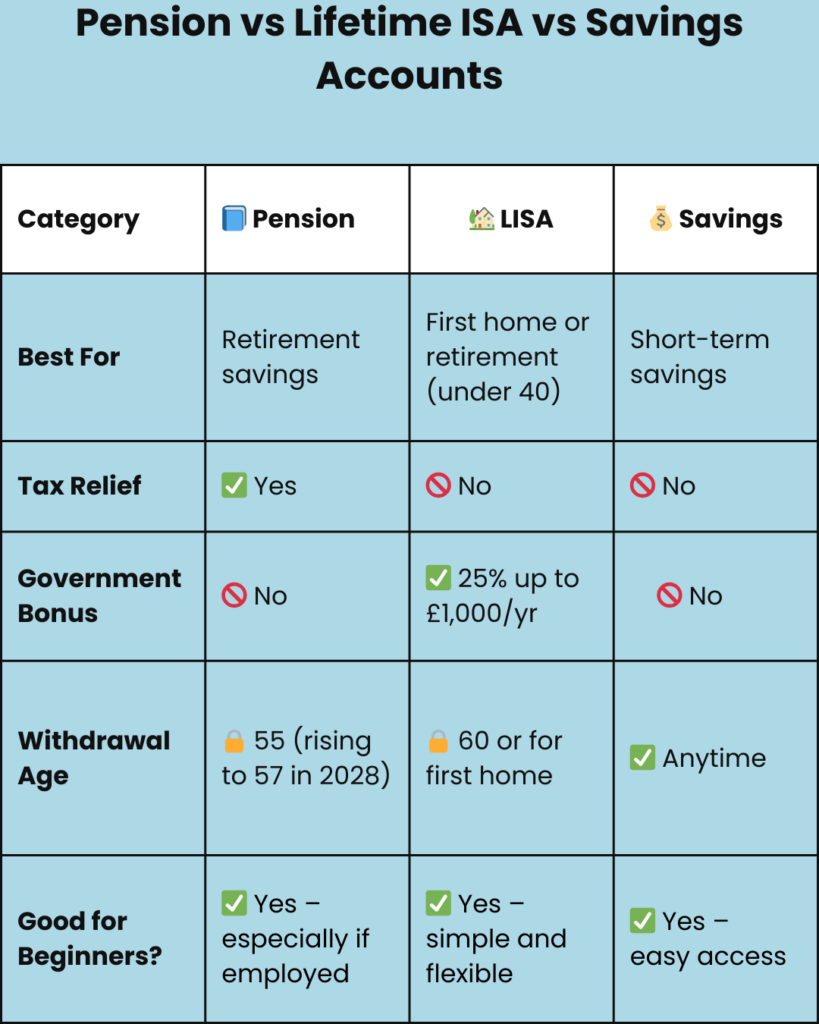

Pension vs Lifetime ISA vs Savings Accounts

When Each One Makes Sense

Pension: Best for long-term retirement savings, significantly when your employer contributes, and you receive tax relief.

Lifetime ISA (LISA): Great if you’re under 40 and saving for a first home or retirement. Offers a 25% government bonus.

Savings Account: Useful for short-term goals and emergency funds. It offers easy access and complete control over your funds, but remember, there’s no tax relief.

Tax Benefits Comparison

Account Type | Tax Relief | Government Bonus | Access Restrictions |

|---|---|---|---|

| Pension | Yes | No | Age 55+ (57 from 2028) |

| LISA | No | 25% (up to £1,000/yr) | Age 60 or for first home |

| Savings | No | No | None |

Pension Contribution Tips for the UK – How Much Is Enough?

Wondering how much to contribute to your pension in the UK? A simple rule of thumb is to save a percentage of your income equal to half your age.

Start with Contribution Calculators

These user-friendly tools can help you estimate how much you’ll need and ensure you’re on the right track:

Consider Your Age and Income

A helpful rule of thumb:

Aim to save a percentage of your salary equal to half your age. So, at age 30, target 15% of your income (including employer contributions).

Even if you can’t reach that percentage yet, remember that every little bit counts. Start with what you can afford and increase it when your income grows.

Maximise Employer Contributions

If you’re employed:

You’re automatically enrolled if you earn over £10,000/year and are over 22.

Your employer must contribute at least 3%; many match more if you increase your share.

✅ Tip: Never leave employer contributions on the table. It’s free money for your future!

Use Salary Sacrifice

This allows you to:

Reduce your taxable income.

You can increase your pension contributions.

Save on National Insurance

You can ask your HR department about setting this up through your payroll

When Can You Access Your Pension?

Minimum Withdrawal Age

Currently, age 55, rising to 57 by 2028

Early Access Penalties

Withdrawing earlier typically triggers a 55% tax penalty unless due to serious ill health.

Bonus Tips

Use extra savings or bonuses to top up your pension.

If self-employed, consider a SIPP (Self-Invested Personal Pension)

Check your State Pension forecast here.

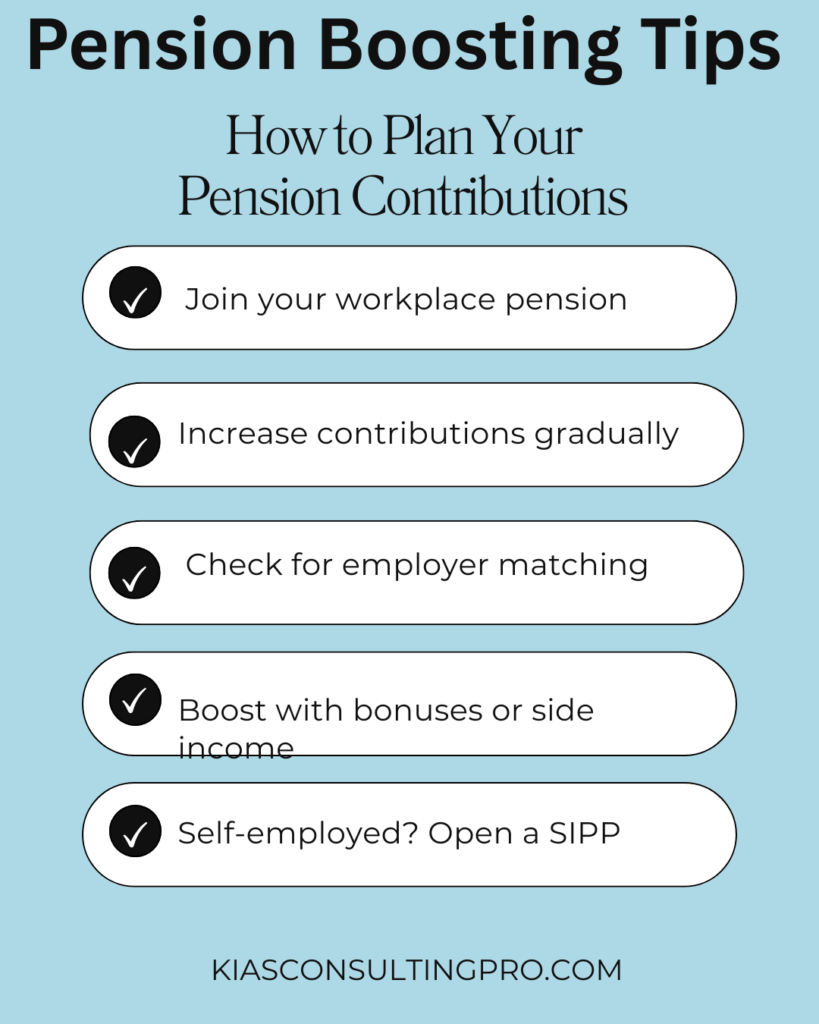

Summary Checklist: How to Plan Your Pension Contributions

Use this quick checklist to ensure you make the most of your pension options. It helps you stay on top of how much to contribute to your pension in the UK, no matter your age or income:

🔲 Use a pension calculator

Check how much you’ll need in retirement and whether you’re on track.

🔲 Join your workplace pension

If you’re eligible, please make sure. You’re enrolled and not missing out on employer contributions.

🔲 Increase contributions gradually

Aim to contribute a % of your salary equal half your age (e.g., 15% at age 30).

🔲 Check for employer matching

You could find out if your employer offers matching above the minimum 3% and match it if you can.

🔲 Use salary sacrifice

You could ask your HR team if you can pay through salary sacrifice to reduce tax and NI.

🔲 Boost with bonuses or side income

Consider topping up your pension using windfalls, bonuses, or extra income.

🔲 Review annually

You could check your pension pot growth and your contributions and adjust if needed every year

🔲 Self-employed? Open a SIPP

Don’t delay — personal pensions offer valuable tax relief even without an employer.

🔲 Check your State Pension forecast

Visit GOV.UK to understand your expected payout and fill NI gaps if needed.