Planning for retirement can initially feel overwhelming, especially if you’re new to pensions. However, gaining a solid understanding of how UK pensions work is not just a decisive step towards taking control of your long-term financial independence, but also a powerful tool that empowers you to make informed decisions about your future.

In this straightforward and easy-to-follow guide, we’ll demystify what a pension is, how it grows over time, and why starting now – regardless of age – can pave the way for a comfortable retirement. You’ll find that understanding pensions is simpler than you might think.

📅 This is Part 1 of a 7-part series created to help beginners understand UK pensions with clarity and confidence.

What Is a Pension?

A pension is a long-term savings plan designed to provide income when you retire. What makes pensions especially powerful is the way your money grows over time — boosted by tax benefits and, if you’re employed, employer contributions, too.

At its core, a pension is a pot of money that you, your employer (if applicable), and the government (through tax relief) contribute regularly. That pot is then invested, allowing it to grow through compound interest and market returns. Compound interest is the interest on a loan or deposit, calculated based on the initial principal and the accumulated interest from previous periods. This means that your money can grow exponentially over time.

How Do Pensions Work?

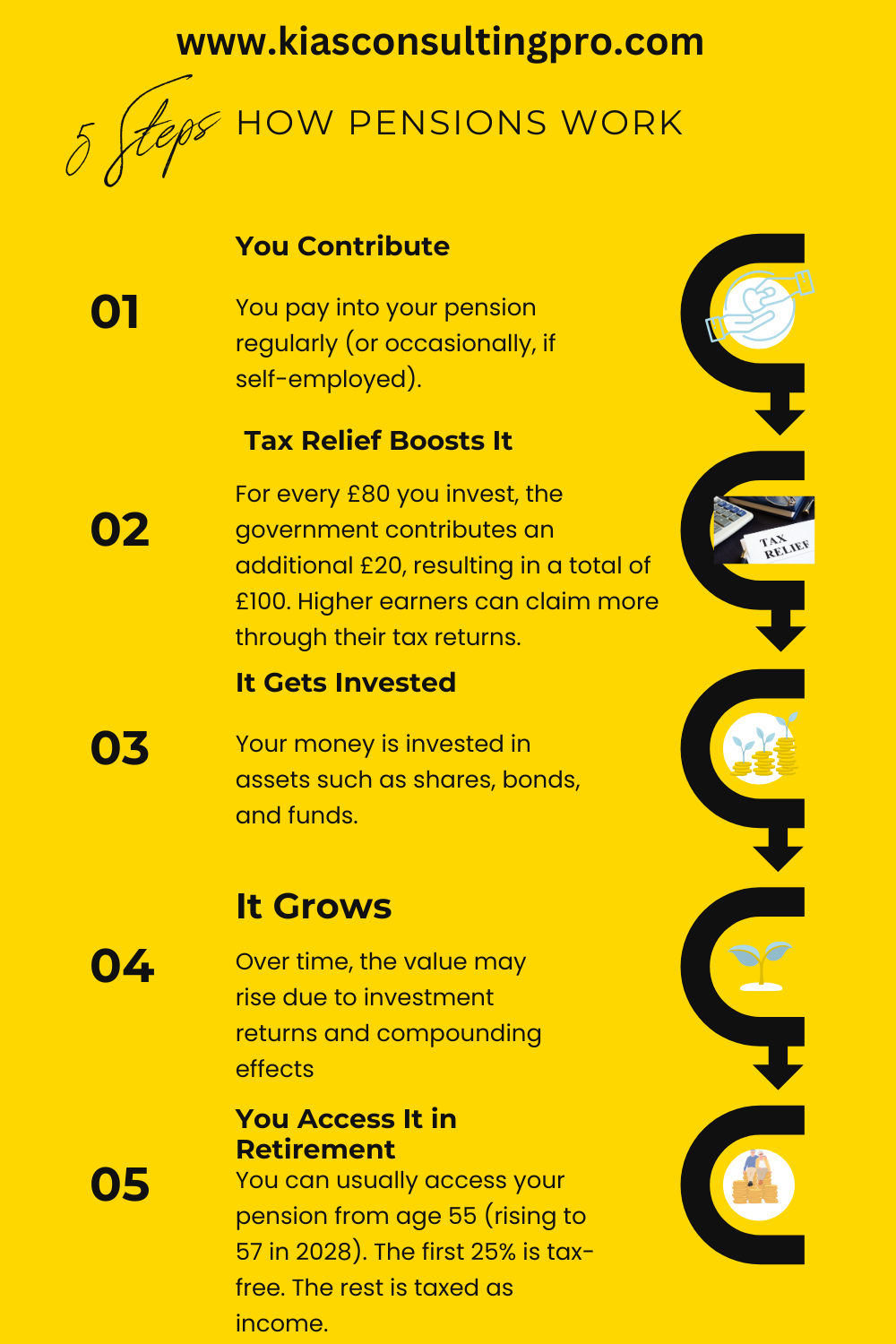

Let’s break it down step by step:

1. You Contribute

You pay into your pension regularly (or occasionally, if self-employed).

2. Tax Relief Boosts It

For every £80 you invest, the government contributes an additional £20, resulting in a total of £100. Higher earners can claim more through their tax returns.

3. It Gets Invested

Your money is invested in assets such as shares, bonds, and funds.

4. It Grows

Over time, the value may rise due to investment returns and compounding effects.

5. You Access It in Retirement

You can usually access your pension from age 55 (rising to 57 in 2028). The first 25% is tax-free. The rest is taxed as income.

Why Pensions Matter

Pensions are one of the most tax-efficient and reliable ways to build wealth for later life.

✅ Tax Relief: You get an instant boost on your contributions.

✅ Employer Contributions: If you’re employed, your workplace pension often includes employer top-ups.

✅ Investment Growth: Your pot grows tax-free over decades. This growth is primarily due to the compounding effect of your contributions and the returns from your investments. Over time, your pension pot can grow significantly, providing you with a substantial retirement fund.

✅ Security: Your funds are protected under UK regulation and generally not accessible until retirement, providing a safety net that discourages impulsive spending. This assurance should give you the confidence to start contributing to your pension without worry.

💪 Think of a pension as “paying your future self.” It’s not lost money — it’s freedom waiting for you.

A Note on Investing Fear vs. Reality

Many people are wary of investing and believe it’s too risky, so they avoid it altogether — often keeping their money in low-yield savings accounts. But what’s frequently overlooked is that you’re already investing if you have a workplace pension.

By default, your pension funds are invested in stocks, bonds, and other financial assets. This means you’re already participating in the market — just passively. Once you realise this, investing for yourself (via a SIPP or ISA) becomes less intimidating.

📌 Want to feel more confident with investing? Check out these helpful guides:

And if you’re thinking longer-term:

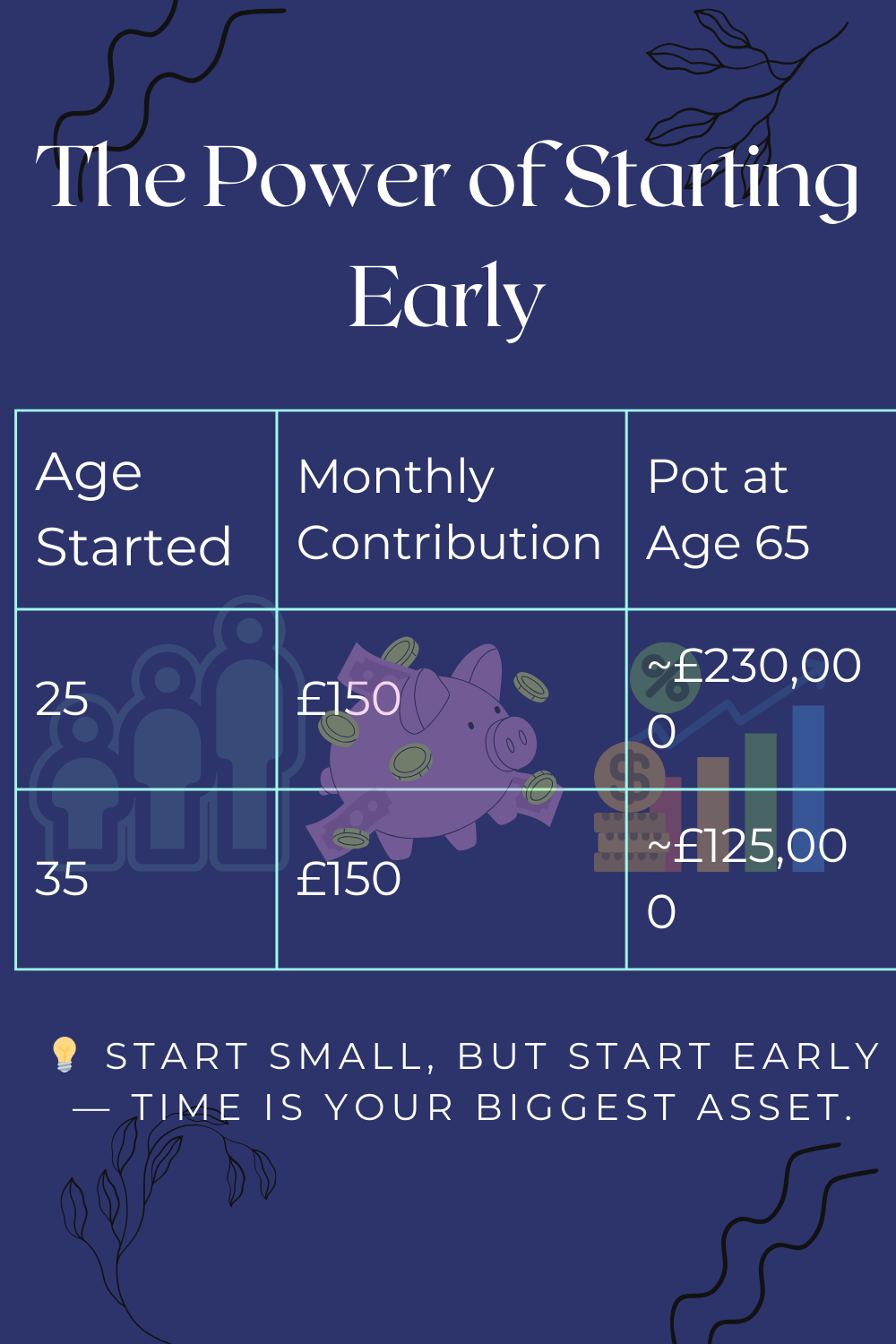

Example: The Power of Starting Early

If you contribute £150/month from age 25 to 65 with 5% growth, you could have ~£230,000

Start at age 35 with the same terms? You might only have ~£125,000

The earlier you begin, the more time your money has to grow.

Time is your most powerful asset. Start small — start now.

Common Pension Myths – Busted

“Pensions are only for older people.”

Wrong. The earlier you start, the more your money grows. Starting in your 20s or 30s gives you decades of compounding.

“Investing my pension is too risky.”

Most pension schemes are diversified and managed by professionals. You can even choose low-risk fund options.

“I won’t get a pension if I’m self-employed.”

Self-employed people can open a personal pension or SIPP and still receive tax relief on contributions.

“I’ll just rely on the State Pension.”

The full State Pension is currently £203.85 per week (2024–25 rates). It helps but is not enough for most people’s retirement lifestyle goals.

Here are 4 myths — BUSTED — to help you take control of your future 💡