Planning for retirement? Don’t let misinformation stop you from building the future you deserve. This guide will uncover 10 common retirement myths UK readers often believe: myths that could delay your savings, drain your pension, or prevent you from making smart financial moves.

💭 “It’s a good feeling to reach retirement and have the choice — not the obligation — to work. Planning gives us the freedom to choose whether or not we continue working. Let’s face it: as we age, health and strength may no longer be on our side. Retirement should be the time to enjoy the fruits of your labour, not a period of financial stress.”

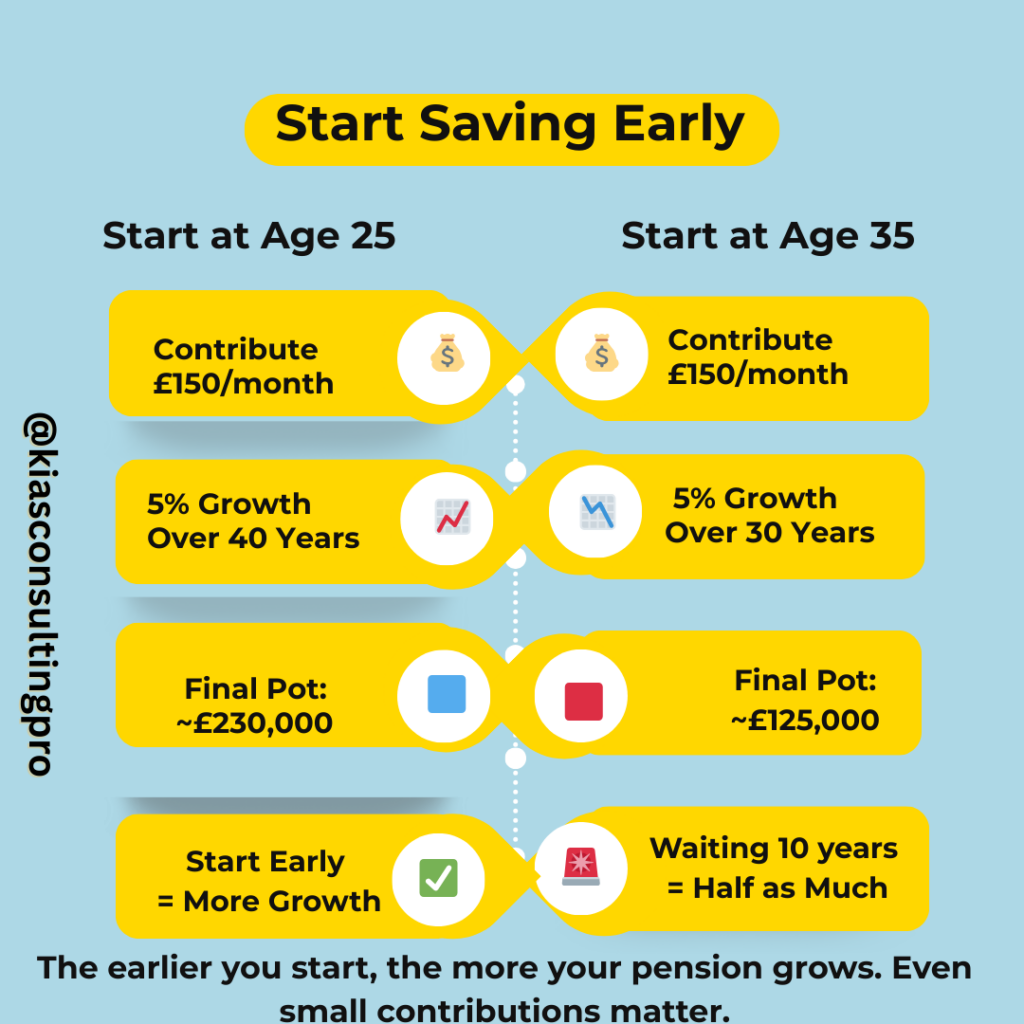

Myth 1: “I’m too young to think about retirement.”

Reality: The power of your money grows exponentially the earlier you start. With the magic of compound interest and employer pension contributions, starting in your 20s or 30s could double or triple your retirement pot compared to starting in your 40s. This means you have the power to shape your financial future from an early age.

💡 Tip: Even small contributions now can grow into a significant sum later.

This is one of the most overlooked retirement myths in the UK — age doesn’t disqualify you from planning.

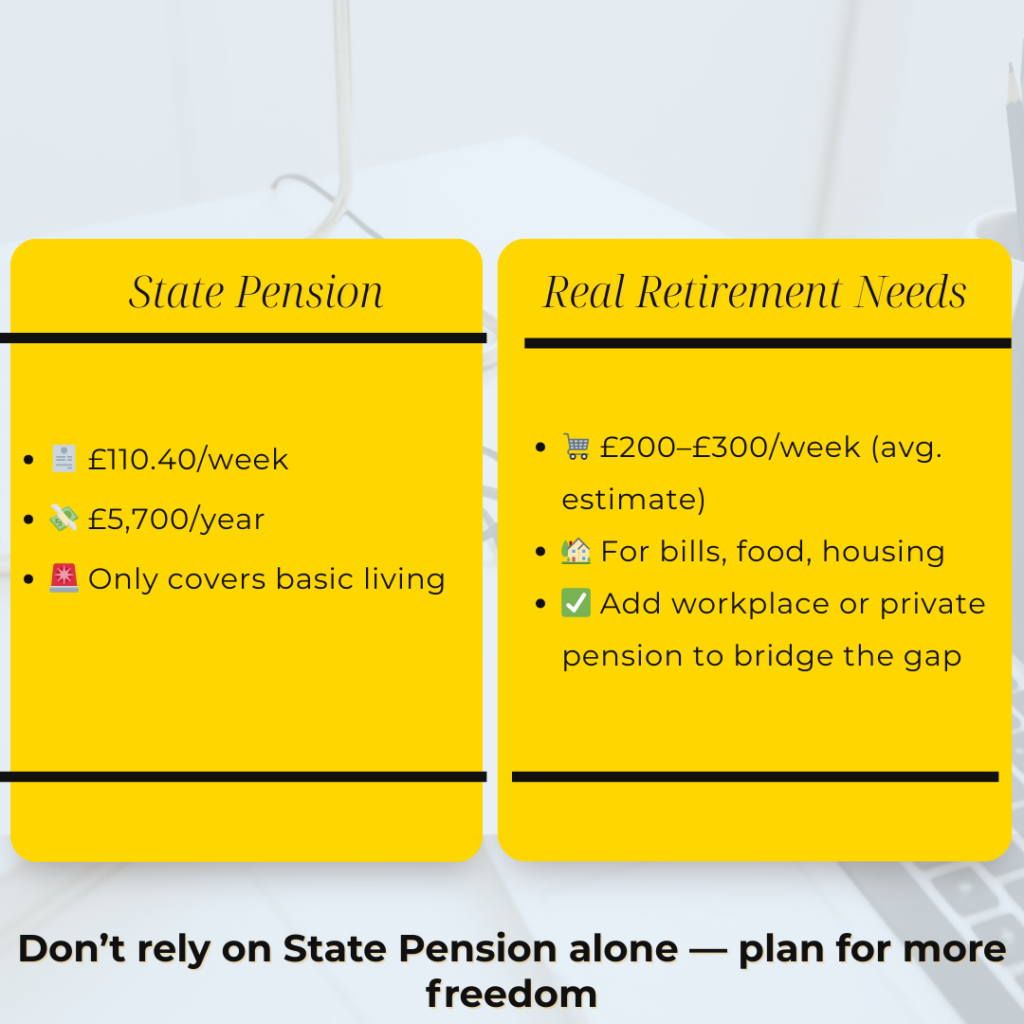

Myth 2: “I can rely solely on the State Pension.”

Reality: As of 2024/25, the full new State Pension is around £110.40 per week—about £5,700 per year. It’s designed as a basic safety net, not a full retirement income.

👉 Check your State Pension forecast here

Myth 3: “My employer pension is enough.”

Reality: Auto-enrolment minimums (8% total, including employer and employee) may not be enough for your desired lifestyle. You may need to increase your contributions or open a private pension for top-ups.

Myth 4: “Pensions are too risky — I’d rather keep my money in savings.”

Reality: Pensions are invested, but that’s a good thing! Your pension is likely already diversified. Inflation can eat away at savings over time, while pensions are designed to grow tax-free.

👉 Discover practical ways to earn more and invest in your future: How to Earn an Extra £1000 a Month

Myth 6: “I can always catch up later.”

Reality: Delaying means losing years of growth and potential employer contributions. While catch-up contributions are possible, starting earlier is far more effective.

👉 Related: How Much Should You Contribute to Your Pension?

Myth 7: “I’ll just rely on my home to fund retirement.”

Reality: Downsizing or equity release might help, but depending solely on property is risky. Market downturns or needing to stay put can limit this strategy.

Myth 8: “I have a private pension somewhere… that should be fine.”

Reality: Lost or scattered pensions can lead to a lack of visibility and control over your retirement funds. By actively tracking, consolidating (when appropriate), and monitoring your pension pots, you can take charge of your retirement planning and ensure you’re making the most of your savings.

👉 Use the Pension Tracing Service

Myth 9: “I’ll use my savings and ISA instead.”

Reality: ISAs and savings accounts are great tools, but pensions come with significant tax perks and employer contributions you won’t get elsewhere. The annual ISA allowance is £20,000 (2024/25), but pensions can offer even more flexibility and long-term growth — especially with tax relief and compound interest. Use them together to maximise your retirement planning.

👉 Also read: How to Top Up National Insurance

Myth 10: “I don’t need to worry about this until near retirement.”

Reality: While pension planning in your 40s, 50s, or even 60s is still valuable, it’s never too early to start. The earlier you begin, the more freedom and flexibility you give your future self, providing reassurance and confidence in your financial decisions.