Pensions can sound complicated, but they don’t have to be! If you’re considering retirement, it’s essential to understand the types of pensions in the UK and how they work. In the UK, you can build up a retirement income in three main ways: State Pensions, workplace pensions, and private pensions (which include personal pensions and SIPPS – Self-Invested Personal Pensions). Each type has its features, benefits, and things to watch out for.

📅 This is Part 2 of our UK Pension Series. We recommend catching up on the other parts to ensure you’re fully informed and prepared.

Embark on your retirement planning journey with this user-friendly guide, part of our comprehensive series. We’ll start by breaking down each pension type in simple terms, providing current facts for the 2024/25 tax year. By the end, you’ll clearly understand the key differences between State, workplace, and private pensions, their advantages and disadvantages, and how they can work together to secure your future. Let’s start and track your progress as you navigate the guide!

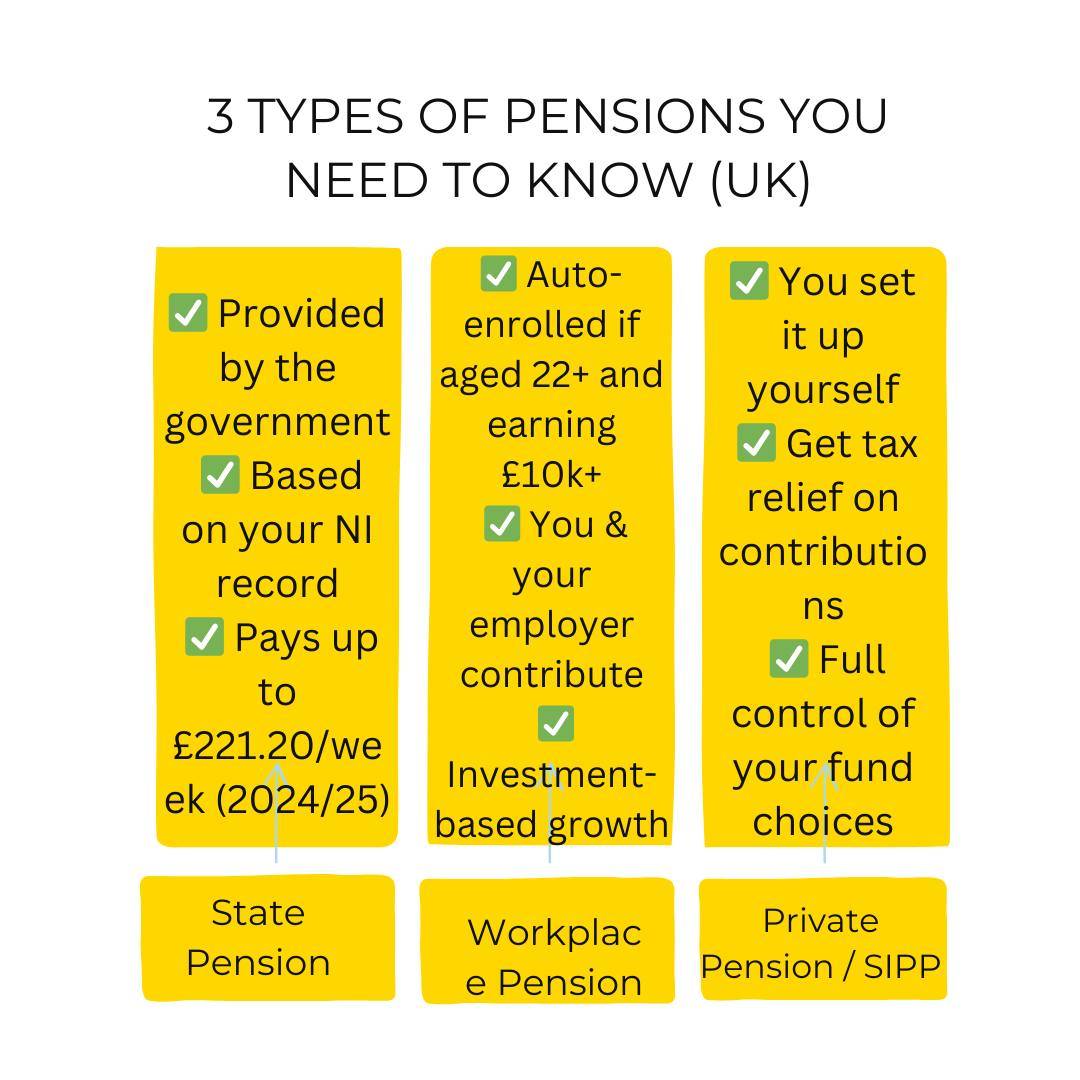

What Are the Main Types of Pensions in the UK?

In the UK, most people’s retirement income comes from a mix of:

- State Pension – A government pension based on National Insurance contributions.

- Workplace Pension – A company pension where you and your employer contribute.

- Private Pension – A personal pension or SIPP you set up yourself.

Each has a role in your overall retirement plan.

State Pension

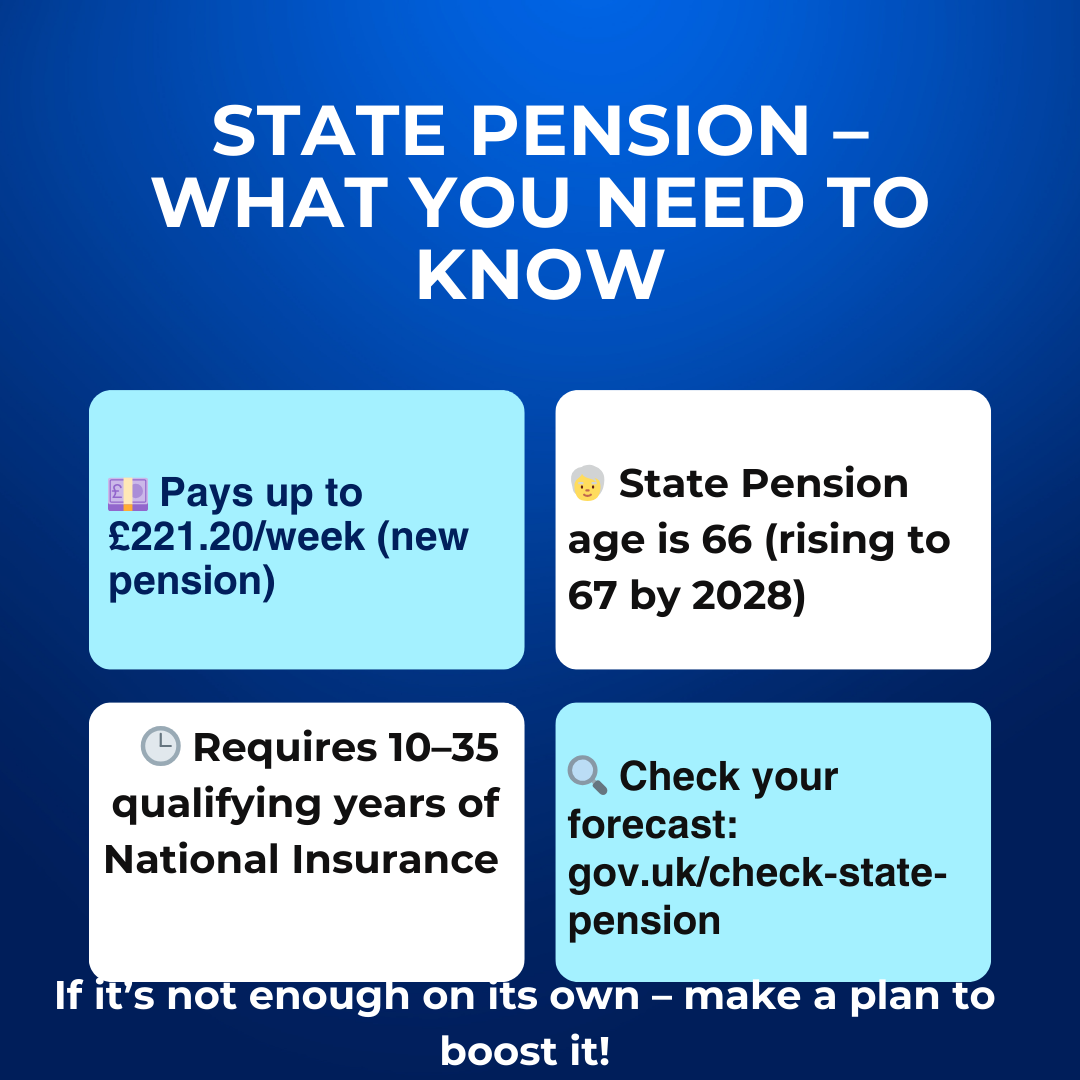

How Much Is the State Pension in 2024/25?

- New State Pension: £221.20/week for those retiring after April 2016 (35 NI years required).

- Basic State Pension: £169.50/week for those who retired before April 2016.

These amounts are typically increased yearly under the ‘triple lock’ policy, which ensures that the State Pension increases by the highest of inflation, average earnings growth, or a minimum of 2.5%.

State Pension Age and Eligibility

- The current State Pension age is 66 (rising to 67 by 2028).

- You need at least 10 qualifying NI years to receive anything and 35 years for the full new State Pension.

Check your State Pension forecast here: Check State Pension

Pros and Cons

Pros:

- Guaranteed for life

- Inflation-linked

Cons:

- Not enough on its own

- Only accessible from age 66 (and rising)

💡 Want to boost your future State Pension?

Learn how to top up your National Insurance contributions to increase your retirement income.

Workplace Pensions

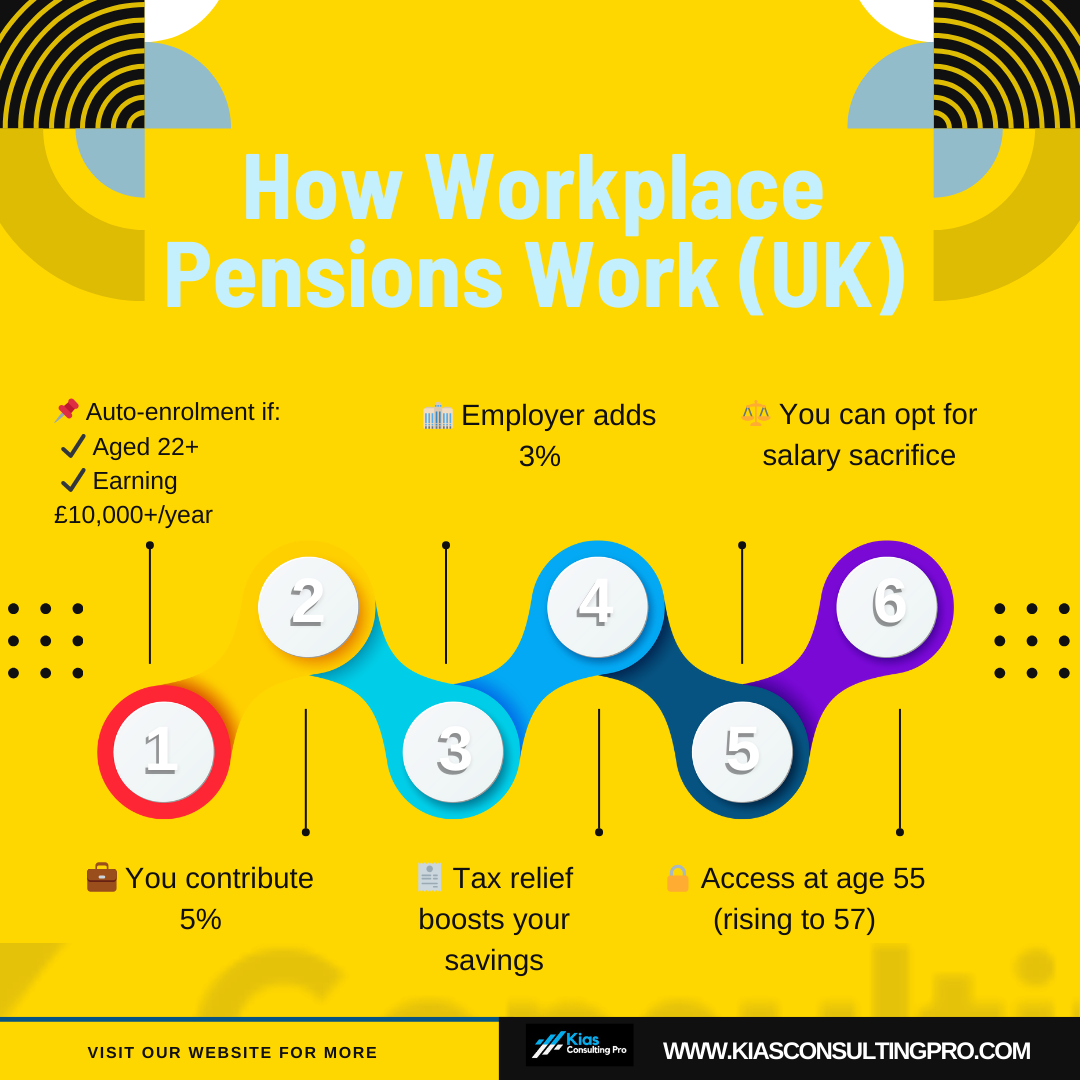

Auto-Enrolment and Contributions

If you’re aged 22+ and earn £10,000+/year:

- You’re automatically enrolled in a workplace pension.

- Minimum contribution: 5% from you (includes tax relief), 3% from employer = 8% total.

You can learn more: Workplace Pensions.

Defined Contribution vs Defined Benefit

- DC pensions invest your contributions; your pot grows based on returns.

- DB pensions promise a fixed income based on your salary and years worked (now rare).

Pros and Cons

Pros:

- Employer contributes

- Tax relief

Cons:

- Investments can go up/down.

- Less control over fund choices

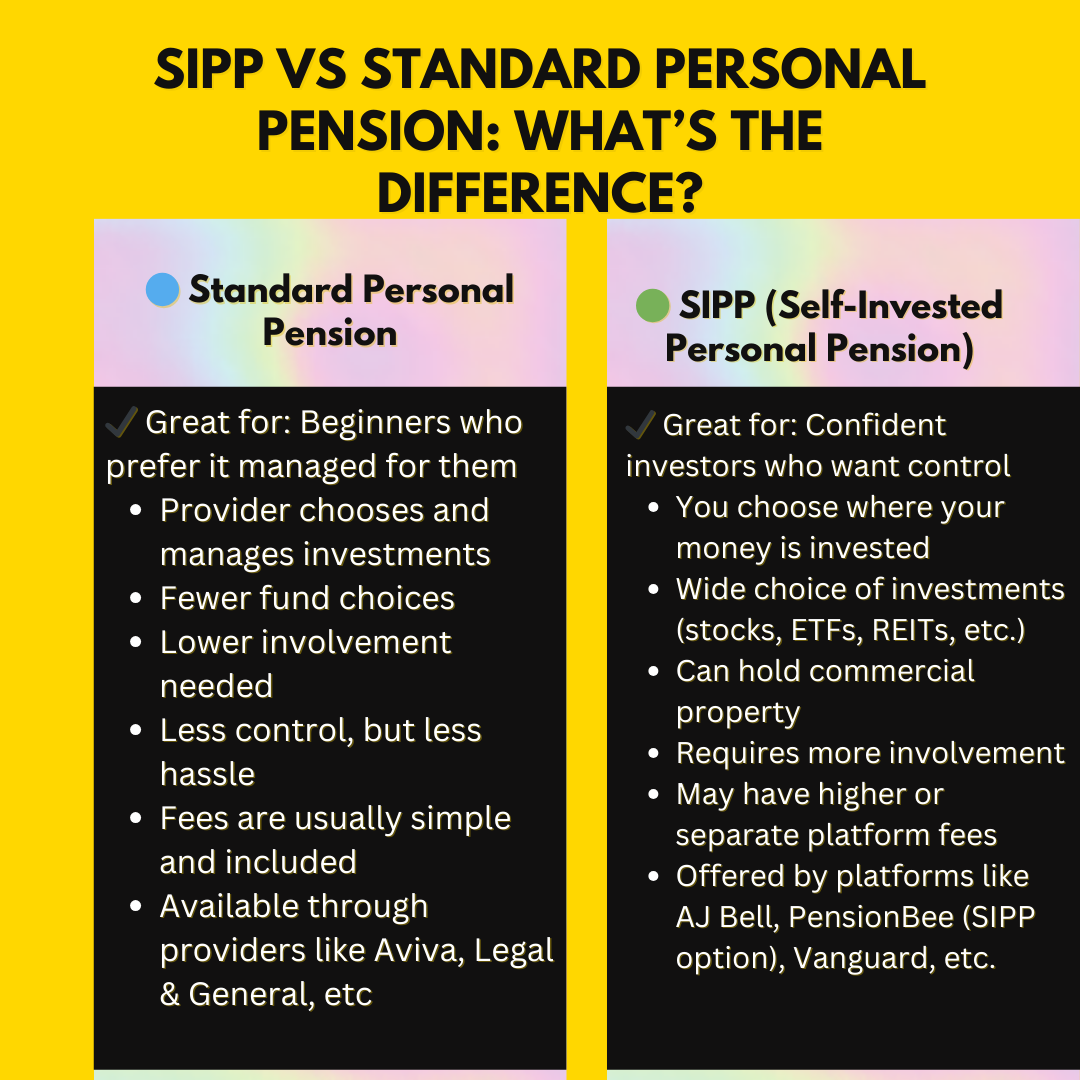

Private Pensions (Personal Pensions & SIPPS)

What is a Personal Pension?

A private pension is a pot you build yourself with a provider.

- SIPP: Offers more investment choices (great for confident investors).

- It can be ideal for the self-employed or to supplement other pensions.

Tax Relief on Contributions

- For every £80 you contribute, the government adds £20 (basic rate) as tax relief. If you’re a basic rate taxpayer, your £ 100 contribution costs you only £ 80.

- Higher-rate taxpayers can claim more through Self-Assessment.

📈 New to investing?

Check out our step-by-step beginner’s guide to investing in stocks in the UK for simple tips to help your pension grow faster.

Contribution Limits

- Annual allowance: £60,000 (or 100% of your earnings, whichever is lower).

- Non-earners can contribute up to £2,880/year (boosted to £3,600 with relief).

Pros and Cons

Pros:

- Full control

- Tax relief boosts savings.

Cons:

- No employer contributions

- Must manage investments

Comparison Table

| Pension Type: State Pension, Workplace | ce Pension, Private | e Pension (SIPP) | |

|---|---|---|---|

| Provider | Government | Employer + Provider | Self-selected provider |

| Contributors | National Insurance | You + Employer + Gov. Relief | You + Gov. Relief |

| Access Age | 66+ (rising to 67/68) | 55 (rising to 57 in 2028) | 55 (rising to 57 in 2028) |

| Investment? | No | Yes (unless DB pension) | Yes |

| Inflation-Proof? | Yes (triple lock) | Partially (depends on the fund) | You choose inflation-proofing |

| Guaranteed? | Yes | Only if the DB pension | No (value can fluctuate) |

Conclusion and Next Steps

Each pension type plays a role:

- The State Pension provides a basic income.

- A workplace pension adds significant long-term savings (especially with employer contributions).

- A private pension or SIPP offers flexibility and additional growth.

👉 Action Steps:

- Check your State Pension forecast.

- Maximise employer pension contributions.

- Consider opening a SIPP for extra savings.

- Download our free ebook “5 Steps to Achieve Financial Independence”

- Bookmark our pensions series

💰 Need more income to boost your pension contributions?

Read How to Earn an Extra £1,000 a Month in the UK for practical ideas to grow your income while planning for retirement.

Helpful Tools:

Would you like any help planning your pension? We’ve got you covered with our free resources and personalised coaching sessions. You’re not alone in this journey.

If you find this helpful, please share it with someone starting their pension journey.

📚 Part of the Pension Series:

- ✅ Part 1: How UK Pensions Work

- ✅ Part 2: Types of Pensions in the UK (You Are Here)

- 🚧 Part 3: How Much Should I Contribute to My Pension?

- 🚧 Part 4: State Pension Forecast: How to Check Yours

- 🚧 Part 5: What Happens to Your Pension When You Change Jobs

- 🚧 Part 6: Can You Retire Early? (And How Your Pension Helps)

- 🚧 Part 7: Accessing Your Pension – Withdrawals & Tax Tips

💬 Let us know in the comments: Which pension type do you find most confusing? Or which one are you already using?